Back to January 2025 Industry Update

January 2025 Industry Update: Truckload Demand

Freight demand weakened further in December as peak retail shipping season came to an end.

Key Points

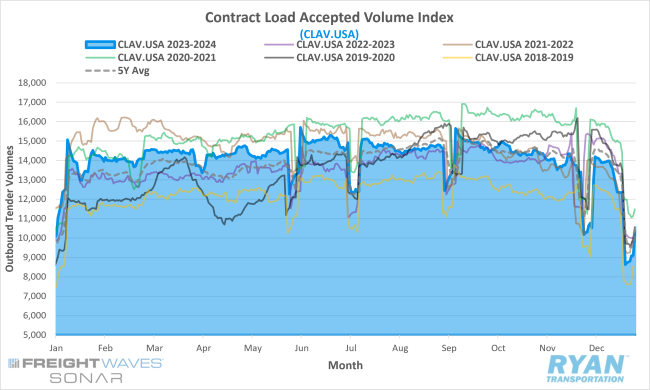

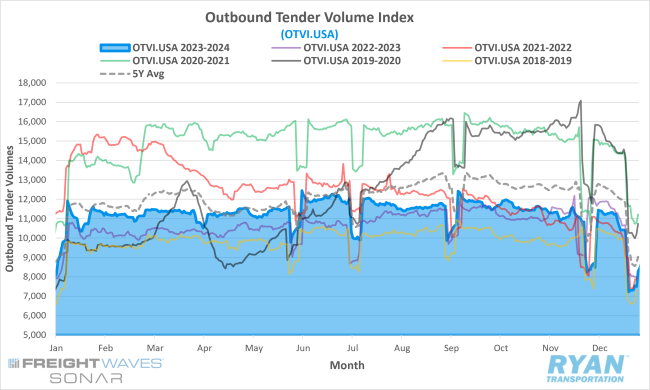

- Comparing mid-month levels to remove disruptions from the holidays, the FreightWaves SONAR Outbound Tender Volume Index (OTVI.USA), a measure of contracted tender volumes across all modes, registered a 2.7% increase MoM in December, rising from 11,016.90 in November to 11,314.13 in December.

- Looking at the 21-day monthly moving average of daily tender volumes to reduce static in the data from the holiday lulls, average daily tender volumes in December were down 6.4% MoM compared to November, dropping from 11,117.44 in November to 10,402.09 in December.

- Compared to December 2023, the monthly average of daily tender volumes was down 8.8% YoY and 13.7% below the 5-year average.

- Spot market activity surged in December following a decline in November, registering 17.3% higher MoM and 23.3% higher compared to December 2023.

- The Cass Freight Index Report, which analyzes the number of freight shipments across North America and the total dollar value spent on those shipments, registered MoM declines for both shipments and expenditures of 7.3% and 2.6%, respectively, with both remaining lower compared to 2023 by 6.5% and 3.4%, respectively.

Summary

Freight demand continued to underperform typical seasonal patterns in December, following a lackluster November. After entering the month in a post-Thanksgiving lull, outbound tender volumes exhibited signs of recovery by the end of the first week and throughout much of the second week. During this period, OTVI values averaged approximately 3% higher than pre-Thanksgiving levels. By the end of the second week, volumes peaked at a 7.5% WoW increase. However, this upward momentum dissipated as tender volumes declined sharply in the second half of the month. This downward trend persisted through December, resulting in an overall decline of 1.1% compared to the beginning of the month.

On an annual basis, December marked the first month in 2024 where the OTVI index fell below its corresponding levels from the previous year. Through the first 11 months of 2024, average daily tender volumes were 6.8% higher than the same period in 2023. While YoY comparisons for December were slightly affected by the post-Thanksgiving slowdown extending into early December, adjusting for this still reflects a 5.3% YoY decline in the monthly average of daily tender volumes compared to December 2023. Furthermore, December’s drop in outbound tender volumes widened the gap between current levels and the five-year average to 13.7% below—the largest differential since March 2023, when volumes were 15.5% below the five-year average.

Although contract volumes faced ongoing challenges in December, the spot market experienced notable growth due to multiple holiday disruptions. According to DAT, spot load postings more than doubled in the days following Thanksgiving and into the first week of December compared to the preceding week. However, after this surge, spot load postings moderated over the subsequent two weeks, decreasing by 14% before rising again by 11% in the week leading up to Christmas. During the final week of the year, as holiday-related closures curtailed operations, total spot load postings fell by nearly 47% WoW.