Back to April 2025 Industry Update

April 2025 Industry Update: Economy

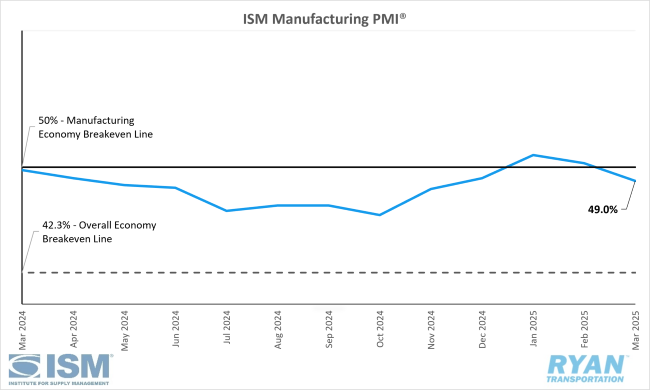

U.S. manufacturing activity returned to contraction in March driven by further weakening in demand despite continued increases in prices.

United States ISM Manufacturing PMI

Key Points

- The ISM® Manufacturing PMI® registered 49.0% in March, a 1.3% decrease from February’s reading of 50.3% and moved back into contraction territory.

- The New Orders Index contracted further in March, dropping 3.4% from February’s reading of 48.6% to 45.2%.

- The Production Index registered 48.3% in March, 2.4% lower than February’s figure of 50.7% and moved back into contraction.

- The Employment Index moved deeper into contraction territory, registering 44.7% in March, a 2.9% decrease from February’s reading of 47.6%.

- The Prices Index jumped 7.0% in March to 69.4%, up from February’s reading of 62.4%.

Summary

Domestic manufacturing activity in the United States reverted to contractionary territory in March, following two consecutive months of expansion, according to the latest ISM® Manufacturing PMI® report. The data indicates a weakening in both demand and output, while input levels continued to rise—an unfavorable combination for overall economic growth.

From a broader economic perspective, March marked the 59th consecutive month of overall economic expansion, following a single month of contraction in April 2020. (Historically, a Manufacturing PMI® reading above 42.3% over time is indicative of general economic growth.)

The ongoing decline in demand was most evident in the New Orders Index, which fell further into contraction for the second straight month, reaching its lowest level since May 2023 at 43.4%. Survey respondents noted a continued deterioration in demand sentiment, with a positive-to-negative sentiment ratio of 1-to-2—down significantly from February’s 1.3-to-1. Additional softening in the demand environment was also reflected in the Backlog of Orders Index, which contracted at an accelerated rate and remained firmly in contraction territory. New export orders also declined.

Despite these challenges, the Customers’ Inventories Index remained in the "too low" range, suggesting potential for future production growth—a modest silver lining in an otherwise subdued demand landscape.

On the output side, the Production and Employment indices together contributed a 5.3% negative impact to the overall Manufacturing PMI® reading in March. The report attributes the decline in production activity to companies adjusting business plans downward in response to continued economic uncertainty. This pullback in factory output, coupled with limited capital investment, has driven further reductions in employment. Respondent companies reported headcount reductions through layoffs, attrition and hiring freezes, with commentary reflecting an approximate 1-to-1.3 ratio of hiring to workforce reductions. Attrition and hiring freezes, in particular, were the preferred methods of workforce management for the second consecutive month, viewed as less disruptive and costly than layoffs.

Regarding input factors, all four primary indices—Supplier Deliveries, Inventories, Prices and Imports—registered in expansionary territory in March. However, the expansion of inputs amidst weakening demand does not bode well for future economic growth. The most notable increase came from the Prices Index, which rose another 7.0% MoM in March, following a 7.7% rise in February. Over the past six months, the Prices Index has surged by 21.1%, reaching 78.5%, its highest level since June 2022.

Among the six largest manufacturing sectors—Chemical Products; Transportation Equipment; Computer & Electronic Products; Food, Beverage & Tobacco Products; Machinery; and Petroleum & Coal Products—three reported growth in March: Petroleum & Coal Products, Computer & Electronic Products and Transportation Equipment. This is a decline from four sectors reporting growth in February.

Why it Matters:

Following a brief return to expansionary territory in the previous two months, momentum in U.S. manufacturing activity stalled in March, leading to a more pessimistic outlook for the sector. According to the latest ISM® Manufacturing PMI® report, nearly every subindex declined sequentially, with the exceptions of the Prices Index, Inventories Index and Customers’ Inventories Index—all of which signal potential headwinds for future economic growth. While signs of progress were more visible in earlier reports, positive indicators in the March data are notably scarce. Nonetheless, the current level of contraction does not yet rise to the level of serious concern, according to Timothy Fiore, Chair of the ISM® Manufacturing Business Survey Committee.

As in February, tariffs remained a prominent theme in both the quantitative data and qualitative business sentiment captured in the March report. Fiore noted that 68% of respondents referenced tariffs in their headline comments, with particular emphasis on the confusion stemming from the uneven rollout of duties on imports from Canada and Mexico. This uncertainty was most acutely felt across the input-related indices of the PMI®, especially the continued surge in the Prices Index. Fiore attributed the 21.1% increase in input prices over the past six months to recent changes in U.S. trade policy.

The report pointed to dramatic price increases in key commodities such as steel and aluminum, driven by newly implemented tariffs, as clear evidence of this inflationary pressure. Additional commodities—including corrugate, copper and resin—have also seen price upticks as businesses shift away from foreign sourcing, driving increased demand for domestic materials.

According to survey respondents, tariff-related uncertainty is approaching a critical threshold for economic stability. The March data shows stagnation in both demand and output, while input costs continue to climb. This environment has fostered indecision among companies and supply chain executives, with many reluctant to act amid unclear policy direction and the potential cost of reversing decisions if circumstances change. As Willard “Bill” Witte, Senior Economist at FTR Associates, succinctly put it, “Indecision leads to inaction, and inaction is a growth killer.”

President Trump is expected to announce plans for reciprocal tariffs in early April, which may help provide clarity in the near term. However, the impact of these measures on the manufacturing sector remains uncertain. Fiore suggested that while the implementation of tariffs may be resolved relatively quickly for many components measured in the PMI®, long-term downside risks persist. He cautioned that although the intention is to reduce the trade deficit, the policy is unlikely to bolster U.S. manufacturing competitiveness or preserve current cost structures. Many U.S. firms source goods from abroad due to cost advantages and altering this dynamic may increase the cost of living. Fiore further warned that higher consumer costs could drive wage demands, potentially fueling a wage-price spiral.

Macro Economy

- Core consumer prices and the Fed’s preferred inflation gauge came in slightly hotter than expected, rising 2.8% YoY in February and 0.1% higher than both the consensus and January’s revised figure of +2.7%, up from the initially reported +2.6%, according to the most recent Personal Income and Outlays Report from the Bureau of Economic Activity (BEA).

- The core Personal Consumptions Expenditures (PCE) index, which excludes volatile food and energy prices, rose 0.4% MoM, just above the +0.3% consensus and 0.3% MoM increase in January.

- Meanwhile, headline PCE in February was up 0.3% MoM, matching both the consensus and January’s reading, and rose 2.5% YoY versus the +2.5% consensus and the prior reading.

- The Federal Reserve kept the target funds rate unchanged at 4.25%-4.50% in their March 19th meeting, noting the U.S. economy continued to expand “at a solid pace” while the economic outlook has become more uncertain, according to the Federal Open Market Committee (FOMC) statement.

- The Fed stuck with initial projections of two 25 bps interest rate cuts this year while the median 2025 policy rate is expected to be 3.9%.

- According to the CME FedWatch Tool, futures traders are anticipating interest rates to remain unchanged at the next Fed meeting in May with a 79.4% probability compared to a 20.6% probability for a 25-bps reduction to 4.00%-4.25%.

- Inflation cooled more than expected in March, according to the latest Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) Report, as headline CPI rose 2.4% on a seasonally adjusted annual basis, down from the 2.8% increase in February and the +2.4% consensus.

- Excluding food and energy prices, core CPI rose 2.8% compared to last year, 0.3% below the 3.1% increase recorded in February and the +3.0% consensus, on a seasonally adjusted basis.

- On a monthly basis, headline CPI declined 0.1% compared to the 0.2% increase in February and was weaker than the +0.1% consensus.

- Core CPI increased 0.1% in March, less than the +0.3% consensus and the 0.2% increase in February.