Back to April 2025 Industry Update

April 2025 Industry Update: Flatbed

Tariff uncertainty and concerns in industrial commodities led to tighter flatbed conditions and higher rates.

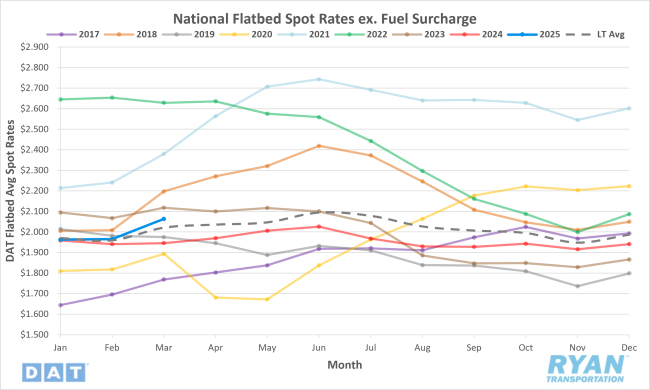

Spot Rates

Key Points

- The national average flatbed spot rate excluding a fuel surcharge rose 5.0% MoM (just under $0.10) in March to just over $2.06.

- Average flatbed spot linehaul rates in March were up 6.0% YoY compared to March 2024 and were 1.0% higher than the LT average.

- The initially reported flatbed contract rate excluding any surcharges increased 0.3% MoM in March and registered 0.3% higher compared to March 2024 levels.

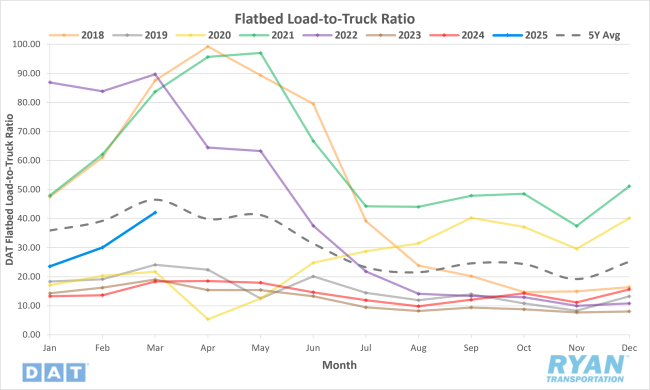

Load-to-Truck Ratio

Key Points

- The flatbed LTR registered 39.9% higher MoM in March at 42.1.

- Compared to March 2024, the flatbed LTR was 129.1% higher YoY but remains 9.5% below the 5-year average.

- Flatbed load post volumes surged in March, rising 46.8% MoM, while equipment posts registered a more moderate increase of 5.0% MoM.

Market Conditions

Flatbed Summary

In the flatbed and RGN truckload market, construction equipment has seen a noticeable rise in highway transport visibility, indicating growth in its market share. This equipment, primarily imported through ports like Savannah (57%) and Tacoma (20%), contribute to overall machinery shipping trends in the U.S. Despite this visibility, total machinery imports were down 23% last year, according to S&P Platts. Baltimore remained the top port for machinery imports, handling nearly a quarter of all shipments, followed by other key ports such as Tacoma, Galveston and Brunswick. This decline in imports has considerable impacts on flatbed freight volume, especially in sectors reliant on overseas equipment.

The U.S. housing market showed mixed signals in February 2025, which is critical for forecasting flatbed freight needs tied to construction. While housing starts increased by 11.2% MoM, the number was still 2.9% lower than a year earlier. Building permits—a key leading indicator—fell 1.2% from January and are down 6.8% YoY, especially in the multi-family segment. Single-family construction showed more stability with an uptick in completions, suggesting near-term demand for building materials. However, the overall trend points to uncertainty, potentially softening future flatbed volumes tied to new housing development.

Post-disaster recovery from 2024 hurricanes and California wildfires have begun to drive increased flatbed demand for building materials. Insurance processing delays and damage assessments slowed initial recovery, but shipment activity has recently picked up. Pre-spring inventory buildup across the landscaping and construction sectors is also underway, expected to follow typical seasonal patterns. Meanwhile, concerns over potential tariffs have caused a spike in imported metals orders, pressuring capacity around major ports and cross-border shipping lanes. Although domestic metal producers are hopeful, demand appears concentrated in regional hotspots, requiring agile freight solutions.

Industry analysts have suggested that while overall construction activity is seasonally slow, pre-tariff industrial shipping has lent some short-term support to the flatbed market. Demand remains weaker compared to other trailer types, but infrastructure projects and select industrial shipments are helping stabilize rates. Ongoing economic uncertainties and trade policies continue to influence market direction, underscoring the need for shippers and carriers to remain adaptable. As spring approaches, the expected ramp-up in construction could offer new opportunities, especially for flatbed carriers well-positioned in active regions.