Back to April 2025 Industry Update

April 2025 Industry Update: Fuel Prices

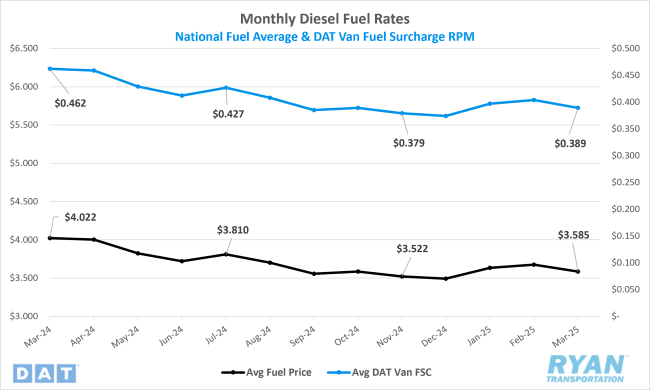

Average fuel prices declined in March as global supply levels increased amidst rising concerns for demand.

Key Points

- The national average price of diesel decreased in March, dropping 2.4% MoM ($0.09) to $3.585.

- Compared to March 2024, diesel prices were down 10.9% YoY (roughly $0.44) in March 2025.

- Builds on U.S. Commercial Crude Inventories outpaced draws in March by +6.0M barrels (bbls) and outperformed the consensus of +4.2M bbls for the weeks ending March 7 and March 28.

Summary

After a relatively strong start to the year registering back-to-back monthly increases for the first time in 17 months, the average price of fuel retreated in March, erasing nearly half of the combined gains recorded in January and February. Following March’s $0.09 MoM decline, the average benchmark retail price of diesel has dropped back equal to the average price recorded in October of last year. Despite the decrease, average prices are still just over $0.09 higher than the 12-month low recorded in December 2024 but have weakened further compared to the same month last year.

On a weekly basis, after registering increases in seven of the first eight weeks, average fuel prices turned negative at the beginning of March and continued that trend throughout much of the month. According to data from the Energy Information Administration (EIA), benchmark diesel prices declined by a total of roughly $0.12 through the first two weeks of the month, marking the largest two-week decline since December 11-18, 2023, when prices fell by roughly $0.20. Average prices continued their descent in the third week, falling another $0.03 WoW, dropping the retail price of diesel to $3.549 and its lowest level since the final Monday of 2024 when prices registered $3.503. Following the three-week decline, however, average fuel prices resumed their upward trend in the final two weeks of the month, climbing just over $0.04 to close out the month.

Builds on U.S. commercial crude inventories continued to outpace draws for the third consecutive month in March as tariff uncertainty led to a surge in imports. U.S. stockpiles of crude rose steadily through the first two weeks before an increase in refinery utilization in the third week led to a bigger drawdown than expected. However, in the week prior to President Trump’s April 2 “Liberation Day” tariff announcement, U.S. crude inventories surged by 6.2M bbls WoW for the second largest WoW build so far this year. According to weekly import data provided by the EIA, net U.S. crude imports rose 63% WoW, or by 999,000 barrels per day (bpd) to 2.585M bpd, the largest WoW rise in imports since the final week of November 2024.

Why It Matters:

The strong correlation between oil prices and overall economic activity contributed to the decline in average fuel prices in March, as crude oil was not immune to the widespread market volatility driven by tariff uncertainties. This downturn was further amplified by the persistent global supply-demand imbalance, which worsened following bearish developments, including expectations of a near-term increase in supply amid growing recession concerns.

In a press release issued on March 3, the Organization of the Petroleum Exporting Countries (OPEC) and its allies, collectively known as OPEC+, reaffirmed their intention to begin phasing out production cuts starting in April, originally implemented nearly two years ago. While similar previous announcements have been delayed due to unfavorable market conditions, the confirmed April 1 implementation date triggered a sharp selloff in the futures market. Analysts speculate that the decision to move forward with increased output, despite a still-weak market, may be aimed at disciplining member countries such as Kazakhstan, Iraq and the United Arab Emirates, which have consistently exceeded their production quotas. Others have suggested that the move may be an attempt to align with calls from U.S. President Donald Trump to boost crude output and ease prices, though OPEC+ has officially denied this influenced their decision-making process.

The EIA, in its latest Short-Term Energy Outlook (STEO), revised downward its global oil demand growth projections for the next two years. Demand is now expected to rise by 0.9 million bpd in 2025 and by 1.0 million bpd in 2026—both figures reduced from previous estimates by 0.4 million bpd and 0.1 million bpd, respectively. The report attributes the downward revisions to a combination of increasing OPEC+ supply and slowing global demand, which is expected to exert significant downward pressure on oil prices. The EIA now forecasts U.S. crude oil prices to average $63.88 per barrel in 2025, down from a previous estimate of $70.68. This projected price decline presents challenges for domestic producers, as profitability typically requires prices to remain above $65 per barrel, according to a recent Dallas Federal Reserve survey.

Analysts at Goldman Sachs have warned that if oil prices fall below $60 and remain at that level, U.S. oil and gas producers are likely to scale back operations, including rig shutdowns and workforce reductions. A decline in crude prices would translate to lower fuel costs, as the EIA projects on-highway retail diesel to average $3.44 per gallon in 2025, the lowest since 2021. However, the resultant contraction in domestic oil production would have adverse effects on freight volumes, particularly in the flatbed and specialized transportation sectors, amid broader economic headwinds.