Back to April 2025 Industry Update

April 2025 Industry Update: Intermodal

Continued gains in market share have yet to translate to higher rates for rail carriers.

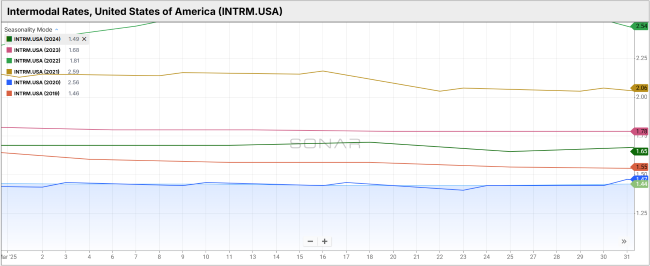

Spot Rates

Key Points

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door spot rate for 53’ dry vans across a majority of origin-destination pairings, ended March $0.03 higher MoM compared to February at $1.47

- Compared to March 2024, intermodal spot rates were down 10.9% YoY and were 22.4% below the 5-year average.

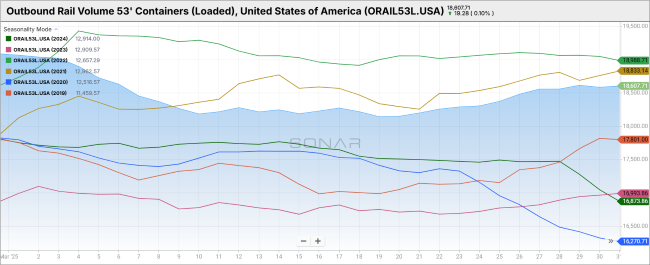

Volumes

Key Points

- Total loaded volumes for 53’ containers for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), declined 2.5% MoM, dropping from 19,091.14 in February to 18,607.71 in March.

- Loaded domestic volumes for 53’ containers in March were up 5.8% YoY compared to March of last year and 10.3% higher than the 5-year average.

Intermodal Summary

Rail activity sustained its trend of annual growth in March, despite heightened market volatility stemming from anticipated shifts in trade policy. According to the latest report released by the Association of American Railroads (AAR), rail traffic continued to demonstrate positive momentum across multiple segments, particularly in intermodal and select carload categories.

U.S. railroads originated 1.10 million intermodal containers and trailers in March, representing an 8.0% YoY increase—or 82,151 additional units—compared to March 2024. This marked the 19th consecutive month of YoY gains for intermodal traffic. On a quarterly basis, intermodal originations reached 3.54 million units in Q1 2025, up 8.3% YoY from Q1 2024. This figure represents the second highest first-quarter total on record, trailing only Q1 2021.

Total carload originations in March reached 906,253 units, a 4.5% YoY increase (39,342 units), representing only the third YoY gain in the past 15 months. Plus, the monthly average of 226,563 carloads was the highest in six months and the strongest March figure since 2022. According to the AAR, 12 of the 20 carload segments recorded growth in March, led by coal shipments, which rose 11.1% YoY (23,963 units). This marked the highest percentage increase for coal since February 2022 and the first YoY gain in 15 months.

Quarterly carload volumes totaled 2.76 million units in Q1 2025, nearly flat with the prior year, reflecting a marginal 0.1% YoY increase (1,758 units). Despite the strong March performance, coal volumes declined 0.3% YoY (2,305 units) over the quarter, marking the lowest first-quarter total for coal on record, per AAR data.

The sustained growth in rail volumes continues to be driven by rail carriers positioning themselves as cost-effective alternatives to OTR freight services. This strategic positioning has helped stabilize pricing dynamics, with limited movement observed in both spot and contract rates. According to FreightWaves’ SONAR IMCRPM1.USA index, which tracks initially reported average contract rates excluding fuel, intermodal contract rates rose slightly MoM in March, increasing by $0.02 to $1.62 from $1.60 in February. However, rates remain down $0.11 YoY compared to March 2024.

Similarly, intermodal spot rates experienced modest month-over-month growth in March, although the gains were not substantial, and rates continue to lag behind March 2024 levels. The limited fluctuation in both contract and spot pricing suggests continued prioritization of contract capacity by intermodal carriers amid steady demand conditions.