Back to April 2025 Industry Update

April 2025 Industry Update: Reefer

Limited signals of early produce led to a decline for both demand and rates.

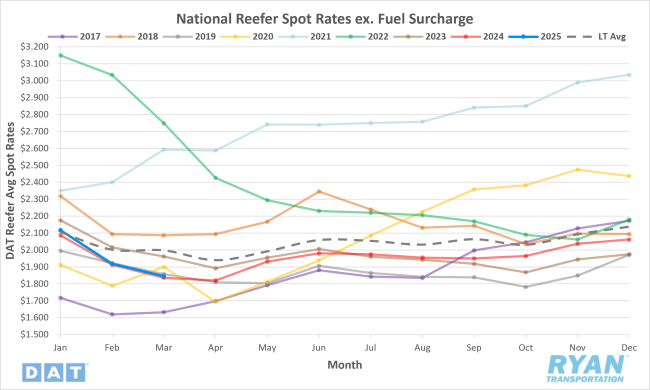

Spot Rates

Key Points

- The national average reefer spot rate excluding fuel declined 3.9% MoM (just over $0.07) in March to $1.85.

- On an annual basis, average reefer spot linehaul rates were up 0.5% YoY compared to March 2024 but were 8.2% below the LT average.

- Initially reported average reefer contract linehaul rates fell 0.6% MoM in March compared to February and were 1.8% below March 2024 levels.

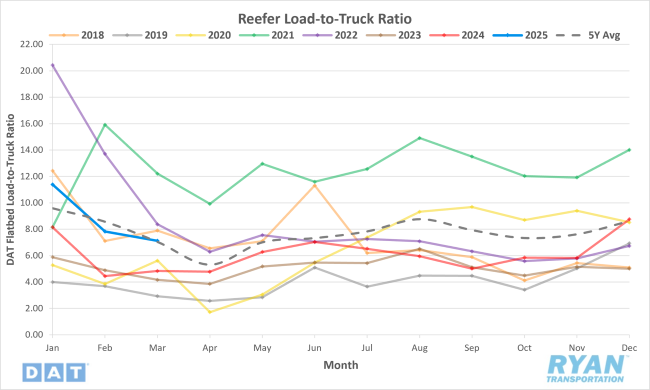

Load-to-Truck Ratio

Key Points

- The reefer LTR registered a 9.1% decline MoM in March to 7.12.

- Compared to March 2024, the reefer LTR was up 47.4% YoY but 8.2% below the 5-year average.

- Refrigerated load posts, recorded from the DAT Analytics load boards, were down 3.7% MoM in March while truck posts registered 6.0% higher MoM.

Market Conditions

Reefer Summary

During the winter months, a major logistical shift takes place in the leafy green produce supply chain, as production moves from California’s Salinas Valley to the Yuma, Arizona region and surrounding desert areas, including parts of Mexico. Yuma becomes the "Winter Salad Bowl," supplying nearly all the nation’s winter vegetables. This season, record-high volumes of lettuce have been reported in Arizona, almost doubling those of 2024, with strong shipments also coming through the Nogales border. The increased volume has led to tighter reefer truck capacity, with average outbound rates from Arizona reaching $2.19 per mile, 6% higher than the previous year.

Meanwhile, Nebraska, particularly Omaha, continues to dominate in red meat production, contributing over 8 billion pounds annually. Omaha’s meatpacking industry remains a key driver of refrigerated freight demand, averaging about 700 reefer truckloads per day. The market presents a strong backhaul opportunity for carriers, as outbound volumes far exceed inbound shipments, leading to outbound reefer rates that are almost 50% higher. In March, outbound volumes rose 29% year-over-year, with average rates reaching $2.55 per mile, up $0.15 from 2024.

As winter ends, lettuce production begins its return to California’s Salinas Valley, ensuring a year-round supply of leafy greens. This transition involves moving entire farming operations—equipment, workers and infrastructure—to match the seasonal growing conditions. Such shifts are essential for maintaining steady nationwide produce availability, though they present operational challenges for carriers who must adjust to changing freight lanes and volumes throughout the year.

Industry analysts, including ACT Research’s Tim Denoyer, note that while reefer rates have softened slightly from January peaks, capacity remains tighter than in the dry van segment. This constrained availability helps support reefer rate stability amid broader economic uncertainty.