Back to April 2025 Industry Update

April 2025 Industry Update: Truckload Capacity Outlook

Population declines in the for-hire sector stabilized further in March as payroll employment edged higher.

Key Points

- Total net revocations, a measure of total authority rejections minus reinstatements, increased by 655 carriers in March. Total revocations went from 4,340 in February to 4,995 in March, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- The number of newly authorized for-hire trucking companies rose in March by 899 carriers, increasing from 4,085 new authorities in February to 4,984 in March.

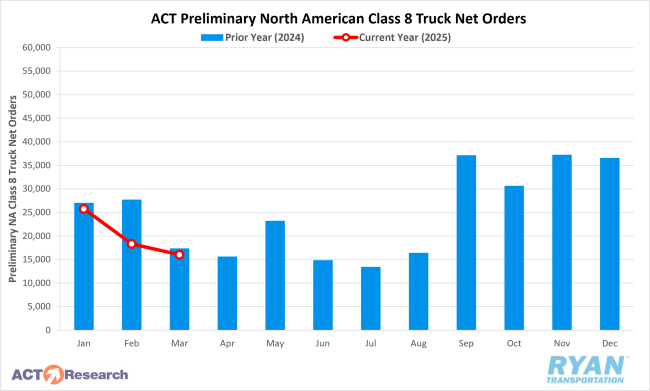

- Preliminary North American Class 8 Order estimates in March ranged from 15,700 units as reported by FTR to 16,000 units per ACT Research, with both estimates reporting lower YoY by 22% and 8.3%, respectively.

Summary

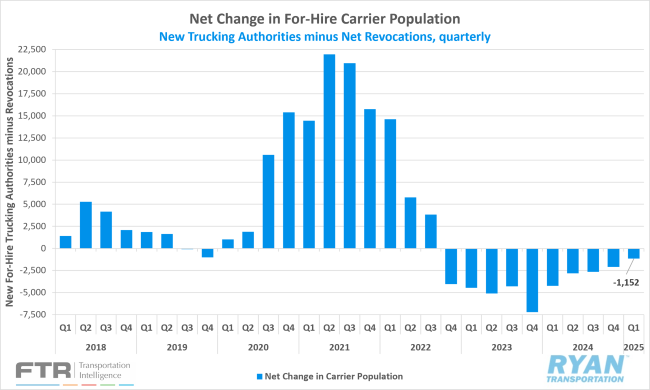

The for-hire truckload sector exhibited further signs of stabilization in March, as carrier authority revocations slightly exceeded new entrants, resulting in a modest net decline of just 11 carriers. This represents the smallest monthly change in the carrier population since December 2018, which saw a net reduction of only two carriers, narrowly surpassing the net decline of 12 carriers recorded in October 2024.

A quarterly analysis reinforces this trend of stabilization. The total for-hire carrier population declined by 1,152 carriers in Q1 2025, the smallest quarterly decrease since revocations began consistently outpacing new authorities in Q4 2022. Excluding that benchmark, Q1 2025 reflects the lowest quarterly net change in for-hire authorities since Q1 2020, when the carrier population increased by 1,026.

Since peaking in Q4 2023 with a net increase of 7,204 carriers, the for-hire carrier population has posted sequentially smaller declines over the past five quarters, indicating a gradual moderation in overall market contraction.

This deceleration in net population decline is primarily driven by a continued moderation in both authority revocations and the establishment of new for-hire trucking operations. According to FTR, the FMCSA issued a higher number of new operating authorities for the third consecutive month in March, marking an increase of nearly 900 carriers over February. This represents the largest MoM gain since March 2020, when new authorities rose by 1,211 carriers.

Despite the MoM growth, total new authorizations in Q1 2025 reached 12,828 carriers, the lowest quarterly total since Q2 2020, but only approximately 80 fewer than in Q4 2024. After declining by over 1,200 carriers in each of the two prior months, revocations rose by 655 carriers in March compared to February. Over the past 12 months, monthly revocation increases have occurred only five times, with March's increase representing the smallest among them—nearly 300 carriers fewer than the next lowest monthly gain.

Meanwhile, equipment orders continued to soften in March as carriers adjust capacity levels in response to ongoing economic uncertainty and a persistently weak freight environment. According to FTR, preliminary North American Class 8 net orders in March declined by 14% compared to February, falling well below the seven-year March average of 24,760 units.

FTR attributes the subdued 2025 order cycle—which spans from September 2024 through March 2025 and is down 8% YoY—to tariff-related uncertainty and broader market volatility, both of which have contributed to investment delays across the industry. Similarly, ACT Research reported that seasonally adjusted Class 8 orders in March increased slightly by 1.1% from February, totaling 16,500 units. However, this modest gain corresponds to a seasonally adjusted annual rate (SAAR) of just 198,000 units, the lowest one-month SAAR reading in nearly three years.

Why It Matters:

The ongoing stabilization in the for-hire carrier population continues to challenge conventional expectations, as there remains little empirical evidence to support a meaningful recovery in market conditions is imminent. While the rise in net revocations less reinstatements appears logical given the persistent softness in the truckload environment, the MoM increase—highlighted in FTR’s latest report—was notably influenced by calendar effects, specifically March having five Mondays. According to FTR, the FMCSA processes a significantly higher volume of revocations on Mondays than on any other day of the week.

At the same time, the continued increase in new operating authorities remains an outlier, with several theories being proposed to explain this trend. One theory suggests stronger-than-expected industrial production in February and a pull-forward in volumes may have encouraged sidelined carriers to reenter the market and drivers to exit unfavorable lease agreements for independent operations. Some have also attributed the trend to overly optimistic or uninformed new entrants. Regardless of the underlying motivation, it is evident that the market remains oversupplied. FMCSA data indicates that the number of active for-hire truckload authorities remains significantly above pre-pandemic levels, exceeding those figures by approximately 87,500 carriers.

Similarly, payroll employment in the for-hire truckload sector showed unexpected strength in March, with the addition of 9,600 jobs on a seasonally adjusted basis, according to preliminary estimates from the BLS. This growth followed upward revisions to January and February data, which collectively added another 1,200 jobs. The March increase represents the largest monthly gain since January 2022. On a YoY basis, for-hire payroll employment declined by 0.3%, marking the strongest comparison since May 2023 and placing total employment 0.6% above February 2020 levels.