Back to April 2025 Industry Update

April 2025 Industry Update: Truckload Demand

The continued pre-tariff pull-forward in inventories failed to translate into any notable gains in truckload volumes.

Key Points

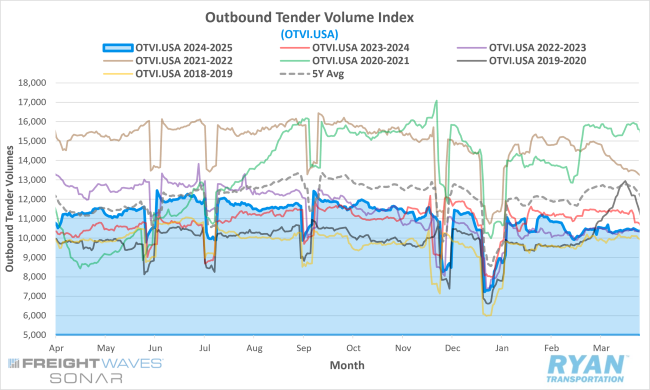

- The FreightWaves SONAR Outbound Tender Volume Index (OTVI.USA), a measure of contracted tender volumes across all modes, declined by 0.9% MoM at the end of March compared to 30 days prior, dropping from 10,465.49 at the start of the month to 10,371.96 by the end.

- The monthly average of daily tender volumes in March dropped 0.7% MoM compared to February, falling from 10,501.74 to 10,428.39.

- Compared to March 2024, average daily tender volumes were down 7.9% YoY and registered 17.4% below the 5-year average.

- Spot market activity regained momentum in March after stalling in February, rising 10.9% MoM and 22.2% higher YoY compared to March 2024.

- The Cass Freight Index Report, which analyzes the number of freight shipments across North America and the total dollar value spent on those shipments, registered higher MoM in February for both shipments and expenditures by 10.6% and 3.6%, respectively. Annual comparisons remained lower YoY by 5.5% and 4.6%, respectively.

Summary

Ongoing uncertainty surrounding tariff policy—both proposed and enacted—continued to exert downward pressure on freight demand in March. Following the typical seasonal slowdown observed in February, shipping activity remained subdued as tender volumes exhibited flat trends for much of the month, underperforming relative to historical seasonal expectations.

Data from FreightWaves SONAR’s OTVI indicated early signs of a potential recovery at the beginning of March, with outbound tender volumes rising 3.8% WoW to start the month. The index continued its upward trajectory into the second week, reaching a peak midweek with volumes 2.1% above early-March levels. However, this momentum proved short-lived, as volumes declined 3.1% by the end of the third week before stabilizing somewhat in the final days of the month. Ultimately, March closed with tender volumes 0.9% below where they began and 2.9% below the monthly peak.

Volatility in weekly freight activity can largely be attributed to disruptions caused by shifting trade policies, which have distorted normal seasonal patterns. As noted in previous reports, uncertainty over tariffs has prompted many shippers to accelerate freight movements in advance of potential duties, thereby complicating both MoM and YoY comparisons. March’s average OTVI declined 0.7% MoM, falling well short of the typical seasonal increase of 5.9% for the month. On an annual basis, average tender volumes, which were positive for most of 2024, have now trended downward through the first quarter of 2025, dropping from 3.8% lower YoY in January to 7.9% lower YoY in March.

A closer examination by equipment type reveals continued weakness in dry van and refrigerated modes, both of which have been negatively impacted by tariff-related uncertainty. According to SONAR’s modal-specific indices, average dry van and reefer volumes declined 1.4% and 1.7% MoM, respectively. On an annual basis, dry van activity has been particularly soft, with average volumes down 9.8% YoY, while refrigerated volumes declined by 2.1% YoY.

Conversely, flatbed activity experienced a significant rebound in March, likely buoyed by shifting industrial demand patterns and the domestic sourcing of materials. The FreightWaves SONAR Flatbed Outbound Tender Volume Index (FOTVI.USA) surged 55.4% MoM in March, representing a sharp reversal from prior softness. On a YoY basis, flatbed volumes increased 22.9%, following a 7.9% decline in February.

Why It Matters:

The continued weakness in freight demand throughout March has raised concerns among industry stakeholders who anticipated the early stages of a broader market recovery. The combined impact of implemented tariffs and persistent uncertainty surrounding the Trump administration’s evolving trade policy has complicated efforts to distinguish between fundamental market shifts and temporary disruptions. Historically, March marks a rebound in freight activity as post-holiday lulls give way to early-season produce shipments and summer merchandise flows. However, this year's seasonal uplift—much like in 2022 and 2023—appears subdued, as the industry continues to adjust to the latest policy changes.

In response to the heightened volatility, many companies have begun modifying their supply chain strategies to mitigate risk, with a particular focus on inventory management. According to the March 2025 LMI® report, the Inventory Levels Index continued to expand, albeit at a slower pace than in February. A closer analysis reveals a notable divergence in inventory behavior between downstream and upstream supply chain segments. In March, inventory levels grew more rapidly at the downstream (retail) level, reversing the trend observed in February, when upstream expansion outpaced downstream growth. This inversion suggests that much of the earlier pull-forward in freight volumes has likely progressed through the supply chain and is now being absorbed at the retail level.

Another strategic shift observed among shippers is the increased use of less time-sensitive rail transportation in place of over-the-road (OTR) trucking. This not only offers cost benefits but also serves as a buffer through extended inventory holding, providing additional flexibility in response to supply chain disruptions.

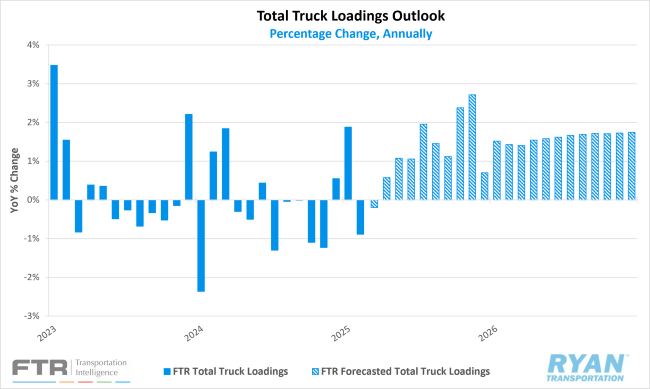

Despite the looming risk of broader trade tensions, FTR’s latest Trucking Update (April 2025) forecasts total truck loadings to increase by 1.1% YoY in 2025. This represents a downward revision from its previous forecast of 1.6% growth, driven primarily by weaker outlooks for food, construction materials and consumer goods.

Among the three major freight modes, flatbed loadings are projected to see the most growth in 2025, with volumes expected to rise 3.1% YoY—down from the previous 4.5% projection due to a softer construction sector outlook. Dry van volumes are now forecast to grow 0.6% YoY, a slight downgrade from the earlier 1.1% estimate. Refrigerated loadings are expected to see the most pronounced deceleration, with growth projections revised from 2.5% to just 0.9% YoY, reflecting a significantly weaker outlook for produce volumes.