Back to December 2024 Industry Update

December 2024 Industry Update: Economy

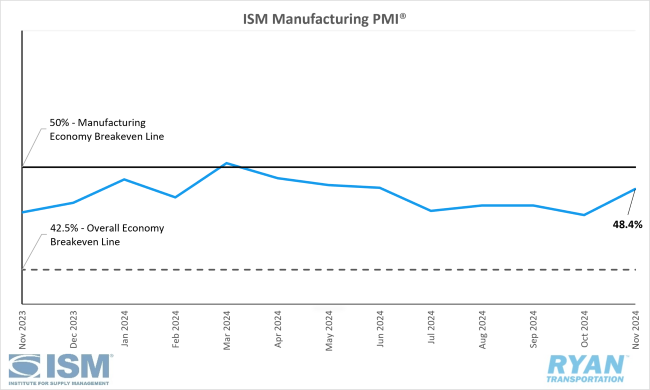

Manufacturing contracted at a slower pace in November compared to October as new orders activity returned to expansion.

United States ISM Manufacturing PMI

Key Points

- The ISM® Manufacturing PMI® registered 48.4% in November, a 1.9% increase from October’s reading of 46.5%.

- The New Orders Index moved into expansion territory in November, rising 3.3% to 50.4% from 47.1% in October.

- The Production Index registered 46.8% in November, 0.6% higher than October’s reading of 46.2%.

- The Employment Index rose 3.7% in November, increasing from 44.4% recorded in October to 48.1%.

- The Prices Index registered 50.3% in November, a 4.5% decline from October’s reading of 54.8%.

Summary

U.S. manufacturing activity remained in contraction territory for the eighth consecutive month in November, although the pace of contraction slowed compared to October, according to the latest ISM® Manufacturing PMI® report. With the index remaining below the 50% threshold, manufacturing activity has now contracted in 24 of the past 25 months. However, on a broader scale, November’s reading marked 55 consecutive months of overall economic expansion, following a brief contraction in April 2020. (A Manufacturing PMI® reading above 42.5% over time typically indicates expansion of the overall economy.)

The slower rate of contraction in November can be attributed largely to improved demand components within the composite index. Notably, new orders returned to expansion territory after seven consecutive months of contraction. While the New Orders Index for November indicated only weak expansion, this shift represents progress toward stabilizing demand. Additionally, the Customers’ Inventories Index, another key demand indicator, remained in contraction but increased slightly to 48.4% in November, up from October’s reading of 46.8%. Survey respondents noted that customers' inventory levels were only marginally above the “too low” threshold, signaling a potential boost to future demand. However, despite the improvement in new orders, the Backlog of Orders Index declined further into contraction, registering 41.8%, a 0.5% decrease from 42.3% in October.

On the supply side, the Production and Employment indices contributed a combined 4.3% positive impact to the Manufacturing PMI® calculation, though both remained in contraction. Employment declined at a slower rate, marking the sixth consecutive month of contraction. Survey respondents reported continued workforce reductions through layoffs, attrition and hiring freezes, with a hiring-to-reduction ratio of 1:1.5, an improvement from October's 1:3 ratio. Despite the marginal increase in new orders, the decline in backlog orders prompted manufacturers to scale back output, keeping production levels in contraction territory as the calendar year draws to a close.

Among the six largest manufacturing industries—Machinery; Transportation Equipment; Fabricated Metal Products; Food, Beverage & Tobacco Products; Chemical Products; and Computer & Electronic Products—only two reported growths in November: Food, Beverage & Tobacco Products and Computer & Electronic Products. This mirrors the performance seen in October.

Why it Matters:

While manufacturing activity remained subdued in November, the latest ISM® report indicated a cautiously optimistic outlook among survey respondents regarding the path to recovery. Consistent with trends observed during past election years, the November ISM® Manufacturing PMI® served not only as a gauge of the manufacturing sector's current health but also as a good barometer of sentiment toward the newly elected powers in Washington. Reflecting this dynamic, the composite index reading of 48.4% surpassed expectations, exceeding the consensus forecast of 47.5%.

Timothy Fiore, Chair of the Institute for Supply Management® Manufacturing Business Survey Committee, attributed some of the improved sentiment to business-friendly tax and regulatory policies anticipated under the incoming Republican administration and a Republican-controlled Congress. These factors contributed to a more favorable outlook despite the continued challenges facing the sector.

Although a rapid rebound in manufacturing activity is unlikely, the November ISM® report highlighted several promising signs of a shortened recovery timeline. Chief among these was the New Orders Index returning to expansion territory for the first time since March, alongside an increase in the New Export Orders Index. While overall demand remains weak, these improvements in both new orders and export orders generally have positive implications across other components of the Manufacturing PMI®.

Another encouraging development was the 5.5% rise in the Inventories Index, which reached 48.1% in November. Fiore noted that while companies are maintaining cautious control over working capital, the slower pace of inventory contraction suggests an increased willingness to invest in future growth—a marked departure from the prevailing trend of the past two years.

Despite these positive indicators, significant challenges remain before the manufacturing sector can achieve sustained growth. Persistent weakness in foundational industries such as Chemical Products and Fabricated Metal Products—key suppliers of materials and components across the manufacturing ecosystem—continues to act as a drag on recovery. Additionally, the Supplier Deliveries Index declined into contraction territory in November after four consecutive months of expansion. As an inverted index, a reading below 50% reflects faster delivery times, which may signal reduced demand rather than supply chain improvement.

Looking ahead, Fiore noted that a return of the Supplier Deliveries Index to above 50%, combined with stabilization in employment levels, could help lift the composite index back into expansion, potentially as early as the first quarter of 2025.

Macro Economy

- Non-farm payroll employment rose by 227,000 jobs on a seasonally adjusted basis in November following upward revisions to both September and October estimates totaling 56,000 jobs, seasonally adjusted, according to the most recent jobs report released by the Bureau of Labor Statistics (BLS).

- The unemployment rate rose 0.1% MoM from 4.1% in October to 4.2% in November.

- Transportation and Warehousing employment added 3,400 jobs in November on a seasonally adjusted basis.

- Truck Transportation added 2,900 jobs MoM in November.

- Warehousing and Storage shed 1,400 jobs MoM in November.

- Both the headline and core PCE indices rose in October, as the all-items index rose by 0.2% MoM and the all-items less food and energy registered a 0.3% increase MoM on a seasonally adjusted basis, according to the November release by the Bureau of Economic Analysis (BEA).

- On an annual basis, the headline PCE index increased by 2.3% YoY in October on a seasonally adjusted basis, 0.2% higher than September.

- Excluding food and energy, the core PCE index rose by 2.8% YoY in October and was 0.1% higher than September.