Back to December 2024 Industry Update

December 2024 Industry Update: Fuel

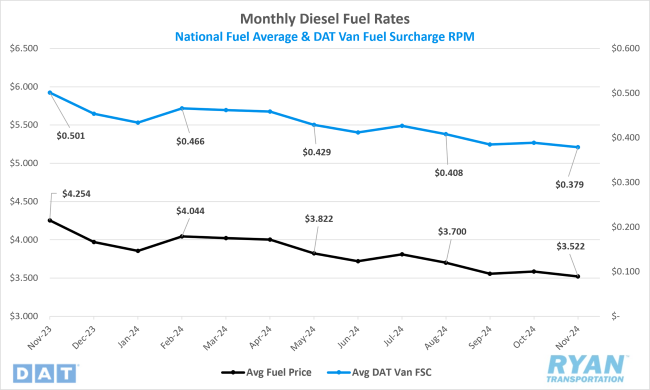

Average fuel prices declined further in November to their lowest level in over three years.

Key Points

- The national average price of diesel declined in November, falling 1.8% MoM, or roughly $0.06, to $3.52.

- Compared to November 2023, diesel prices were 17.2%, or just over $0.73, lower in November.

- Draws on U.S. Commercial Crude inventories outpaced builds in November by 2.1M barrels (bbls) and underperformed the consensus of 3.9M bbls for the weeks ending November 1 and November 29, according to data released by the Energy Information Administration (EIA).

Summary

Average fuel prices returned to a downward trajectory in November following a brief uptick in October, driven by heightened concerns over escalating tensions in the Middle East. With this decline, fuel prices have now decreased in 11 of the past 14 months, reaching their lowest level since September 2021, when the average price of diesel was $3.38. From their peak of $5.75 in June 2022—just months after Russia's initial invasion of Ukraine—average diesel prices have dropped by more than $2.23 as of November. On a weekly basis, fuel prices experienced consistent declines during the first three weeks of November, cumulatively falling just over $0.08. However, increased demand driven by holiday travel in the final week partially offset these losses, with prices rising by nearly $0.05 WoW to close the month.

As peak refinery season concluded, commercial crude inventories remained largely stable throughout November. Notably, a sharp draw on commercial stocks occurred during the final week of the month, with reserves declining by over 5 million barrels—exceeding the consensus forecast of just over 4 million barrels—amid an unexpected 2.8% WoW increase in refinery utilization, bringing utilization rates to 93.3%.

Similarly, inventories of ultra-low sulfur diesel (ULSD) showed minimal variation during November, with the Energy Information Administration (EIA) reporting levels that were deemed relatively robust for the season. However, this assessment was challenged by a shift in the futures market. The spread between front-month and second-month futures on the CME Commodity Exchange transitioned from contango—where second-month prices exceed front-month prices, a condition observed for several months—to backwardation, where front-month prices surpass those of the second month. Backwardation typically signals tighter inventory conditions, increasing the value of barrels available for immediate delivery while reducing the value of deferred deliveries.

Why It Matters:

Global supply levels remained elevated in November while weaker demand continued to exert downward pressure on fuel prices, extending a trend observed over the past two years. Although concerns regarding the potential escalation of conflict between Israel and Iran, which had driven prices higher in October, have temporarily abated, the persistent softness in global demand has led to fuel prices reaching their lowest levels in over three years. This development has further deepened bearish sentiment regarding the market outlook.

OPEC+ had initially planned to implement production cuts of 2.2 million barrels per day, starting in September. However, this decision was postponed to December 1 and has now been deferred once again to the group’s next meeting on January 1, 2025. Analysts suggest that the anticipated increase in production may not materialize, given that demand growth is expected to remain stable or potentially decline, particularly if tariffs proposed by the new administration come into effect.

Speculation surrounding the trajectory of fuel prices under the new administration has intensified. Proponents of a bullish outlook argue that a resurgence in U.S. manufacturing activity could drive higher demand, while the possibility of renewed sanctions on Iran under former President Trump could reduce supply, thereby supporting price increases. Conversely, bearish analysts highlight that a more producer-friendly policy agenda might encourage U.S. oil producers to increase output. With current production already at historic highs of approximately 13.5 million barrels per day, further increases could exacerbate the oversupply in global markets. Additionally, bearish arguments emphasize the potential for economic slowdowns resulting from tariffs, which could ultimately suppress demand.