Back to December 2024 Industry Update

December Industry Update: Intermodal

Intermodal volumes remained robust in October despite weakening carload traffic, while rates trended negatively.

Spot Rates

Key Points

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door intermodal spot rate for 53’ dry vans across a majority of origin-destination pairings, registered slightly higher MoM, increasing from $1.48 in October to $1.49 in November.

- Compared to November 2023, intermodal spot rates are down 11.8% and registered 26.5% below the 5-year average.

Volumes

Key Points

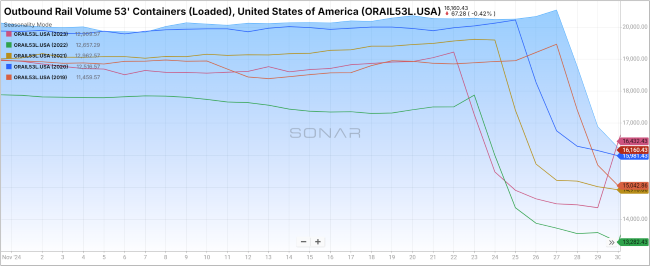

- Total loaded volumes for 53’ containers for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), registered a 2.6% increase MoM at the halfway point of the month in November compared to the midway point in October.

- On an annual basis, total loaded volumes for 53’ containers in November were 7.9% higher at the halfway point of the month compared to the year before and were 7.5% above the 5-year average.

Intermodal Summary

Despite historical standards traditionally reflecting declines in the later months of the year, intermodal volumes continued to register impressive gains in November. According to the Association of American Railroads’ (AAR) December report, U.S. railroads originated an average of 282,000 intermodal containers and trailers per week in November, up 10.7% compared to November 2023 levels and the highest weekly average for the month of November since the association began keeping records in 1989. Per the report, container volumes continued driving the growth as container originations averaged 272,243 per week during the month, the third highest weekly average on record despite Thanksgiving week typically being the one of the lowest-volume weeks of the year.

Driven primarily by the strength in imports, YTD container volume through November is the highest it has ever been, registering 10.6% higher compared to November 2023. While the gains in container volumes continued to trend higher, the close positive correlation between manufacturing output and carload volumes led to further declines across the carload sector. According to the AAR’s report, total U.S. carloads were down 3.8% YoY, making November the 10th out of 11 months that carloads have registered lower than the previous year’s levels.

With November’s decline, YTD carload volumes are down 3.1% from the same time period last year and the second lowest YTD level on record, falling just behind the levels recorded in 2020. Per the report, coal continues to be the primary driver for the carload declines, as U.S. rail carloads of coal are down 14% YTD following the 15.2% YoY decline registered in November. However, the report notes that the AAR Freight Rail Index (FRI), which is defined as intermodal plus carloads excluding coal and grain, given what little relation their gains and declines have to do with the broader economy, was up 2.8% MoM in November to its highest level since May 2021.

Despite the strength in volumes, they have yet to translate into any notable gains for either contract or spot rates. Following a $0.06 MoM decline in October to end the month at $1.59, initially reported intermodal contract rates, measured by the FreightWaves SONAR Intermodal Contract – Initial Reporting of Average Base Rate Per Mile (IMCRPM1.USA), erased the losses from October and then some, increasing $0.09 to end the month at $1.68. However, despite the monthly gains, intermodal contract rates were still $0.04 lower than they were compared to November 2023. While contract rates are working their way up from the bottom, intermodal marketing companies have not had much concern in protecting their contracted capacity, as evident by spot rates remaining depressed.

Although most intermodal volumes are moved under contracted rates, movements in spot rates signal whether intermodal companies are under any pressure to protect that capacity. The $0.01 MoM increase in November and registering 11.8% lower compared to last year is indicative rail carriers are still operating with ample capacity.