Back to December 2024 Industry Update

December 2024 Industry Update: Truckload Capacity Outlook

Changes in the carrier population have started to stabilize as the market gets closer to balance.

Key Points

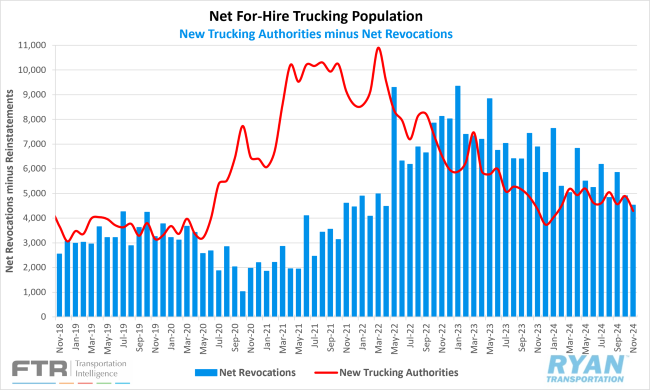

- Total net revocations, a measure of total authority rejections minus reinstatements, declined in November by 381 carriers, dropping from 4,909 revocations in October to 4,528 in November, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- The number of newly authorized for-hire trucking companies fell by 600 carriers, dropping from 4,897 new authorities in October to 4,297 in November.

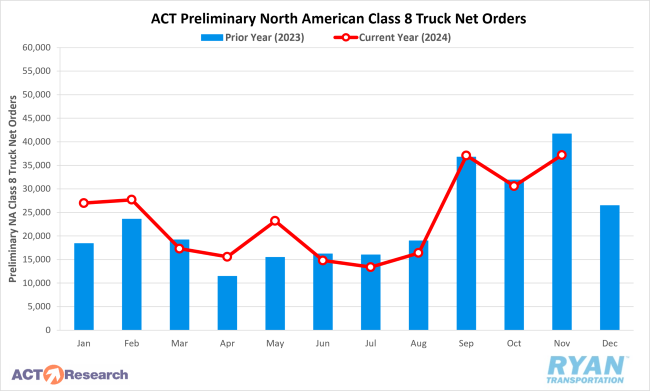

- Preliminary North American Class 8 Orders ranged from 33,500 units, as reported by FTR, to 37,200 units per ACT Research’s estimates, with annual comparisons both registering lower by 7% and 11%, respectively.

Summary

The carrier population exhibited continued signs of stabilization in November, with a net decline of only 231 carriers. While carrier population reductions have been recorded in nine of the 11 months this year, November’s decline was the second lowest, following a minimal decrease of 12 carriers in October, according to FMCSA data. Since July, the average monthly decline has been 576 carriers, significantly lower than the 2023 average of 1,755 monthly for-hire carrier reductions.

This stabilization can largely be attributed to a slowdown in monthly revocations of for-hire operating authority. Net revocations in November fell to 4,476 carriers, the lowest level since April 2022, and represented a decline of 381 carriers from October’s figure of 4,909. Year-to-date, the monthly average of authority revocations stands at just over 5,620 carriers—a notable decrease from the historical averages of 6,500 in 2022 and 7,240 in 2023. According to FTR, the number of active for-hire trucking operations remains approximately 36% higher than pre-pandemic levels as of November.

The stabilization of the for-hire market was also reflected in the latest Logistics Managers’ Index (LMI) report for November, which noted a 1.7% MoM increase in the Transportation Capacity sub-index, bringing it to 52.6%. This marks continued gradual expansion in capacity. Transportation Capacity has not contracted for a full month since March 2022. While October’s figure of 50.8% suggested a near standstill in capacity changes, November’s results indicate modest growth. However, this expansion was not evenly distributed—smaller firms reported capacity contraction, whereas larger firms experienced expansion. Survey responses revealed a tightening of capacity in the second half of the month, shifting from 57.3% in expansion territory (November 1–18) to 49.1% in contraction territory (November 19–30).

Preliminary data on North American Class 8 truck orders in November indicated a MoM increase of 12% to 21%, depending on the source. However, annual comparisons showed weaker performance, with FTR estimating a 7% YoY decline and ACT Research reporting an 11% decline compared to November 2023 levels. November marked the sixth consecutive month of YoY declines in Class 8 orders.

Despite these declines, ACT Research noted that the industry is still in the early stages of building 2025 order backlogs. Progress in closing the backlog gap compared to a year ago has been limited, even with seasonally strong orders. FTR offered a more optimistic perspective, highlighting that November’s orders exceeded seasonal expectations and brought net YTD orders 9% higher than the same period in 2023. Both reports identified strong demand in the vocational sector as a key driver of November volumes. Additionally, growing confidence in a potential freight market recovery in 2025 has supported increased replacement demand among fleets.

Why It Matters:

The volatility observed in the for-hire carrier population over the past four years appears to be subsiding, as indicated by the November release of FMCSA data. Signs of stabilization in capacity levels, though encouraging, present a paradox given the minimal improvement in truckload conditions over the past year. While the market remains oversupplied amidst subdued demand, the flattening in declines in for-hire operating authority revocations aligns with the theory that the current freight recession is nearing its end. This development supports growing expectations for a full market recovery by 2025.

Although monthly data on new operating authorities and net revocations from the FMCSA provides some perspective on shifting capacity levels, it offers a limited view of overall supply. According to the latest BLS report, non-seasonally adjusted payroll employment in the for-hire trucking sector increased by 2,100 jobs in November, following two consecutive months of decline. When adjusted for seasonal factors, payroll employment rose by 2,900 jobs MoM in November, marking the most significant monthly gain since September 2023, when the industry partially recovered losses from the Yellow Corporation's shutdown in the previous month. This rise in employment suggests that, while the trucking industry continues to hire, there is no rush to add jobs prior to any projected increases in demand.

Although November's BLS payroll data indicates that for-hire trucking employment has risen approximately 1.9% compared to the pre-pandemic levels of February 2020, more granular data through October suggests a closer alignment with pre-pandemic benchmarks. General freight truckload employment experienced a notable decline in October, compounded by downward revisions to August and September estimates. Furthermore, preliminary Q2 2024 figures from the BLS Quarterly Census of Employment and Wages (QCEW)—a more comprehensive measure of payroll employment—indicate that general freight truckload employment was 22,000 jobs lower than current estimates at the end of June. This discrepancy implies that capacity could be tighter than reflected in the BLS monthly jobs reports and an overall positive for the market recovery timeline.

Back to December 2024 Industry Update