Back to December 2024 Industry Update

December 2024 Industry Update: Truckload Supply

Ongoing supply contractions combined with the Thanksgiving holiday led to rejection rates reaching their highest level in over two years.

Key Points

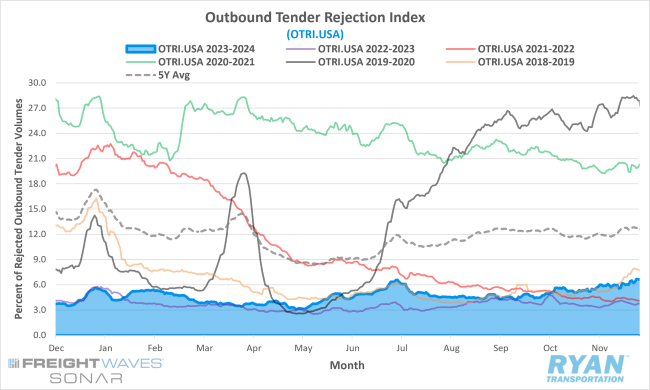

- The FreightWaves SONAR Outbound Tender Rejection Index (OTRI.USA), a measure of relative capacity based on a carriers’ willingness to accept freight volumes under contract reflected as a percentage, registered 61 basis points (bps) higher MoM at the halfway point in November compared to October, rising from 5.39% to 6%.

- The monthly average of daily tender rejections in November was 71 bps higher MoM, increasing from 5.26% in October to 5.97% in November.

- On an annual basis, average daily tender rejections were up 2.3% YoY but remain 6.27% below the 5-year average.

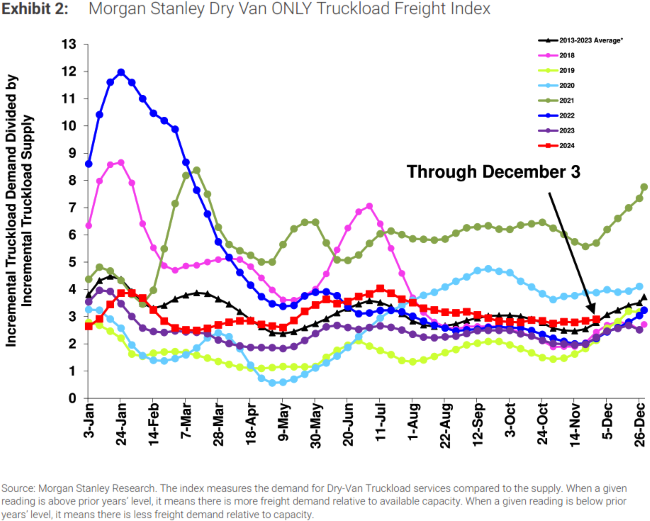

- The Morgan Stanley Truckload Freight Index (MSTLFI) continued to strongly outperform seasonality in November and registered sequential increases throughout the month, keeping the index above the LT average.

Summary

In November, tender rejection rates continued to build on the momentum established in October, driven by multiple capacity disruptions that pushed the index above 5% for the first time since July. Rejection rates began the month with strong gains, increasing nearly 80 bps during the first week to exceed 6%, compared to October’s close at 5.2%. However, the significant surge observed at the start of the month represented the peak rate of increase, as the index stabilized within a narrow range, oscillating just above or below 6% for the majority of November. Leading into the final week and the Thanksgiving holiday, tender rejections gained renewed traction, rising 50 bps WoW before reaching a monthly high of 6.67% on the day after Thanksgiving. This marked the index's highest level since July 2022.

From an annual perspective, tender rejections continued to outperform 2023 levels, with average daily rejections in November 2.3% higher YoY, an increase from the 1.4% YoY growth observed in October. November's YoY gap was the widest recorded YTD, narrowly surpassing the 2% spread reported in July. While annual comparisons remain volatile, November showed early signs of deviation from historical trends, particularly those observed in 2019. During the first half of November, rejection rates averaged 45 bps higher than in 2019. However, the second half saw a decline, with current rates averaging 68 bps below their 2019 counterparts.

Despite Thanksgiving occurring in the final week of November in both 2019 and 2024, the divergence in tender rejection behavior was considerable. In 2019, rejection rates surged 1.6% WoW in the final week compared to just 0.8% in 2024. On Thanksgiving Day itself, rejection rates reached 7.94% in 2019, significantly higher than the 6.31% recorded this year.

The ongoing contraction in capacity was also reflected in the November Morgan Stanley Truckload Freight Index. While demand underperformed typical seasonal trends, the supply component strongly outperformed, declining 230 bps sequentially—far exceeding the typical 80 bps decrease for the month. Survey respondents highlighted the potential for additional carrier attrition due to upcoming insurance renewals and ongoing challenges posed by an unsustainable rate environment. Forward-looking sentiment remained mixed; some respondents expressed optimism about market stabilization, while others maintained a more cautious outlook for a meaningful recovery in 2025.

Why It Matters:

The resilience of tender rejections in November serves as a positive indicator that the market is gradually approaching equilibrium. Following multiple capacity disruptions in October, there was lingering uncertainty whether the increase in rejection rates was solely a temporary byproduct of those disruptions or a genuine indication of tightening supply levels. However, the rejection index sustaining a level near 6% throughout November—despite a sluggish start to the retail peak season and subdued demand—suggests the latter is likely the case.

While signs of market stabilization are evident, there are clear indications that full equilibrium has yet to be achieved. This is particularly apparent from the limited reaction in rejection rates during the final week of November leading up to the Thanksgiving holiday. Although the OTRI reached its highest level in over two years, hovering around 6%, this remains reflective of a relatively loose market. The 49 bps WoW average increase during Thanksgiving week exceeded the two-year average of 29 bps for the same period. However, it fell significantly short of the 101 bps WoW average observed during the four years preceding the onset of the current deflationary market cycle.

The next critical test of truckload supply levels will occur in the weeks leading up to Christmas and extending through the New Year’s period. Historically, rejection rates have increased by over 200 bps on average in the days preceding Christmas, followed by an additional rise of approximately 50 bps in the week leading up to New Year’s Eve. However, over the past two years, the average increase leading up to Christmas has declined to approximately 133 bps, reflecting the absence of a traditional peak season. Notably, the subsequent increase in the week following Christmas has remained largely consistent.

The performance of rejection rates during these two weeks will provide key insights into market conditions as the industry enters 2025, offering a clearer picture of the trajectory toward equilibrium.