Back to February 2025 Industry Update

February 2025 Industry Update: Economy

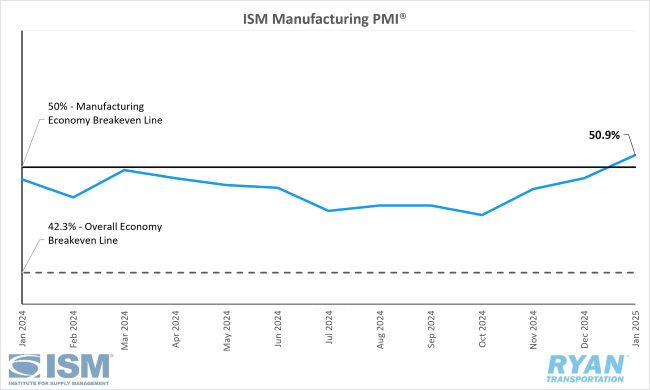

Domestic manufacturing returned to growth in January following 26 months of contraction, driven by strong new orders and production.

United States ISM Manufacturing PMI

Key Points

- The ISM Manufacturing PMI® registered 50.9% in January, a 1.7% increase from December’s reading of 49.2%.

- The New Orders Index remained in expansion territory, registering 3.0% higher in January to 55.1% from the 52.1% recorded in December.

- The Production Index registered 52.5% in January, 2.6% higher than the 49.9% recorded in December.

- The Employment Index jumped 4.9% in January and moved into expansion territory, up from 45.4% in December to 50.3% in January.

- The Prices Index registered 54.9% in January, 2.4% higher than the 52.5% recorded in December.

Summary

Following 26 consecutive months of contraction, U.S. manufacturing activity expanded in January, according to the latest ISM® Manufacturing PMI® report. With relation to the overall economy, January’s reading marked the 57th month of expansion after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3%, over a period of time, typically indicates an expansion of the overall economy.) According to the report, demand has clearly improved, while output expanded and inputs remained accommodative.

Improvements in the demand components of the composite index was most notably reflected in the New Orders Index moving further into expansion territory. According to the Manufacturing PMI® report, survey panelists noted improved levels of demand performance with a 2-to-1 ratio of positive comments compared to those expressing concerns regarding near-term demand, an improvement from the 1.5-to-1 ratio recorded in December. Other notable positives in terms of demand stemmed from the New Export Orders Index moving back into expansion territory while the Customers’ Inventories Index remained in “too low” territory. Per the ISM® report, survey respondents reported the amounts of their companies’ products in their customers’ inventories suggest a demand level that is positive for future production levels.

Meanwhile, the indices primarily used to measure output in the composite index (Production and Employment) combined for a +7.5% upward impact on the Manufacturing PMI® calculation in January, an indication that panelists’ companies are proceeding with growth plans in the new year. Much of the positive impact on output came from a sharp rise in the Employment Index, which returned to expansion territory after contracting in 14 of the last 16 months. Companies are continuing to reduce headcounts through layoffs, attrition and hiring freezes with January’s ratio of hiring versus staff reduction comments registering 1-to-1, compared to the 1-to-2 ratio recorded in December.

Of the six largest manufacturing industries – Chemical Products; Transportation Equipment; Computer & Electronic Products; Food, Beverage & Tobacco Products; Machinery; and Petroleum & Coal Products – four registered growth in January (Petroleum & Coal Products; Chemical Products; Machinery; and Transportation Equipment).

Why it Matters:

Although January’s Manufacturing PMI® is a positive sign for the domestic manufacturing sector that’s been stuck in contraction for over two years, the timing of the growth has left the door open to speculation. January’s report came amidst considerable uncertainty and an unpredictability of the new administration’s policies to enforce tariffs on the nation’s three biggest trading partners – Canada, Mexico and China. While, at present, the threat to raise levies on imported goods from our North American neighbors appears to be a negotiation tactic, some analysts have noted the upturn in manufacturing could’ve been a byproduct of pre-emptive purchasing to get ahead of the tariffs. However, according to Timothy Fiore, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee, the impacts from seasonal adjustment factors were minimal in January, and the fundamentals in the readings suggest that this could be the start of an expansion cycle rather than a one-off reading.

Per Fiore, there are a lot of positives that came from January’s report that provide support for the gradual return in growth across the sector. For starters, Fiore noted that the seasonal factors for January this year were half of what they were in January of last year, and the overall performance was better. Despite the lack of seasonal adjustments compared to the same time last year, the raw numbers were much stronger, as indicated by four of the five subindexes that directly factor into the Manufacturing PMI® calculation registering growth during the month (New Orders, Production, Employment and Supplier Deliveries). Most notably, Fiore pointed to the strength in performance in the Production Index, which flipped back to expansion territory following nine consecutive months in contraction, as well as the Employment Index ending its seven-month streak in contraction. According to Fiore, January’s Employment Index reading suggests that companies’ lengthy efforts to reduce headcounts and right-size staffs could be over.

Positives aside, there were still a few areas of concern stemming from January’s report, with the biggest red flag coming from the continued expansion of the Prices Index despite the relatively weak demand growth. Fiore pointed out that having strong price growth without strong demand will only lead to prices trending higher over time. As demand increases, prices will continue to increase, making the Fed’s battle with inflation more difficult. The other area of concern came from the Inventories Index moving deeper into contraction territory even amidst the extra buying to get ahead of potential tariffs, an indication that companies are struggling to balance supply and demand.

While the duties on imported goods from Mexico and Canada have been temporarily paused, the tariffs on those from China are still expected to go into effect this month. The president has also set his sights on taking action on goods imports from the European Union and United Kingdom. That kind of protracted tariff turbulence could potentially lead to a “false start on demand,” according to Fiore. Should the intention of levies be a backing for border policy with Mexico and Canada, then it is likely that the tariffs will be short-lived; however, if it is to bring manufacturing back to the states, that will take more time making the outlook for manufacturing recovery less clear.

Macro Economy

- Headline consumer prices rose in December by 2.6% compared to the same month in 2023, up from 2.4% in November, according to the most recent Personal Income and Outlays Report from the Bureau of Economic Analysis (BEA).

- The core Personal Consumptions Expenditures (PCE) Index, which excludes volatile food and energy prices and is the Federal Reserve’s preferred inflation gauge, rose by 2.8% on an annual basis, unchanged from October and November.

- On a monthly basis, headline PCE rose 0.3% MoM compared to November while core PCE was up 0.2% MoM, nearly consistent with the Fed’s targets.

- Inflation accelerated in January more than expected according to the latest BLS Consumer Price Index (CPI) Report, as headline CPI rose 3.0% on a seasonally adjusted annual basis while core CPI was up 3.3% during the same time.

- On a monthly basis, the all-items index jumped 0.5% MoM in January compared to the 0.4% rise recorded in December.

- Excluding food and energy, core CPI was up 0.4% MoM compared to December’s 0.2% increase.

- The Federal Reserve kept the target funds rate unchanged at 4.25%-4.5% at their latest meeting at the end of January, snapping the streak of three straight meetings with interest rate cuts.

- According to the CME FedWatch tool, the market consensus expects rates to remain unchanged at the central bank’s next meeting in March, with the no change probability at 97.5%.