Back to February 2025 Industry Update

February 2025 Industry Update: Intermodal

Rail activity remained mixed with strong intermodal volumes outperforming volatility in sector-specific carload volumes

Spot Rates

Key Points

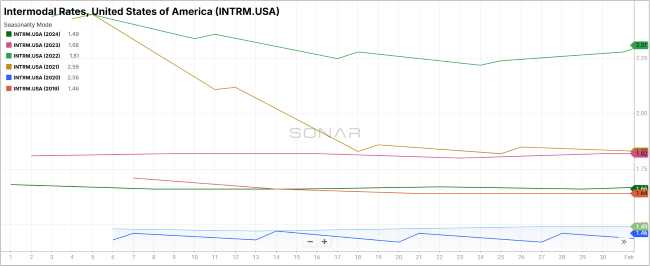

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door intermodal spot rate for 53’ dry vans across a majority of origin-destination pairings, ended January at $1.49, unchanged from the end of December.

- Mid-month comparisons reflected a more significant shift, with January intermodal spot rates registering 2.6% lower MoM, or $0.04, dropping from $1.51 in December to $1.47 in January.

- Compared to January 2024, intermodal spot rates were down 10.2% YoY and were 17.6% lower than the 5-year average.

Volumes

Key Points

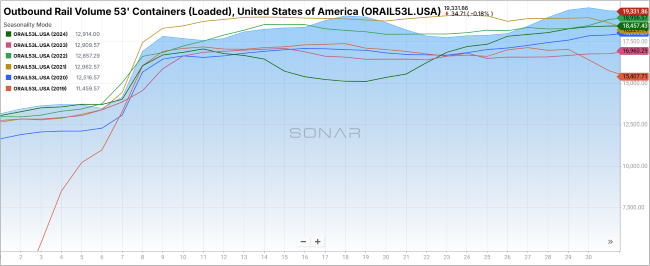

- Total loaded volumes for 53’ containers for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), declined by 11.5% MoM when comparing mid-month levels, dropping from 20,734.71 in December to 18,353.71 in January.

- Loaded volumes for 53’ containers in January were 6.9% higher YoY compared to January 2024 and roughly 5% higher than the 5-year average.

Intermodal Summary

Overall rail activity remained robust in January, despite disruptions related to holidays and adverse weather conditions. According to the latest report from the Association of American Railroads (AAR), rail movements exhibited a mix of stability and sector-specific volatility. Strength in consumer-driven commodities contributed to U.S. railroads originating 1,329,715 intermodal containers and trailers in January, representing a 10.3% YoY increase compared to January 2024 and marking the 17th consecutive month of intermodal traffic growth. The report also noted that average weekly originations reached 265,943, the second-highest level on record, trailing only January 2021.

Meanwhile, total U.S. rail carload volumes reached 1,025,664 units in January, reflecting a modest 0.2% YoY increase and the first overall growth in five months. Coal shipments continued to weigh on carload volumes, declining 2.3% YoY, though this represented the smallest percentage decline in over a year. When excluding coal and grain, combined intermodal and carload traffic increased by 6.4% YoY.

Despite sustained volume growth, intermodal rates have yet to reflect these gains, with neither spot nor contract rates registering significant increases in January. Initially reported intermodal contract rates opened the year at $1.65, marking a $0.05 increase from the close of 2024. Rates briefly peaked at $1.72 ahead of the Martin Luther King Jr. Day holiday before steadily declining throughout the remainder of the month, closing at $1.64. On a YoY basis, contract rates were up 2.5% ($0.04) but remained 3% below the five-year average. Similarly, intermodal spot rates, which serve as an indicator of whether intermodal carriers are prioritizing contract capacity for shippers, gained positive momentum ahead of the holiday before stabilizing and ending the month flat MoM.