Back to February 2025 Industry Update

February 2025 Industry Update: Truckload Demand

Multiple disruptions during the month led to gains in market share for spot freight while contract volumes returned to more normal seasonal patterns.

Key Points

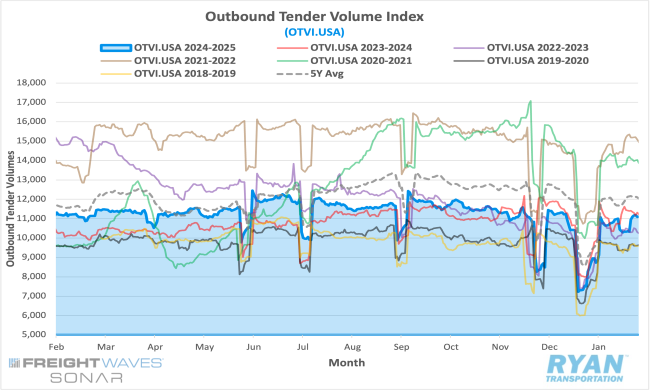

- Mid-month comparisons of the FreightWaves SONAR Outbound Tender Volume Index (OTVI.USA), a measure of contracted tender volumes across modes, reflect a decline of 4.8% MoM in January, dropping from 11,314.13 in December to 10,776.69 in January.

- The monthly average of daily tender volumes in January rose 4.7% MoM compared to December, rising from 9,843.82 to 10,310.64.

- Compared to January 2024, average daily tender volumes were down 3.8% YoY and registered 9.8% below the 5-year average.

- Spot market activity ticked up for the second consecutive month in January with spot load post volumes registering 27.4% higher MoM but slightly lower compared to January 2024 levels by 0.2%.

- The Cass Freight Index Report, which analyzes the number of freight shipments across North America and the total dollar value spent on those shipments, registered MoM declines in December for both shipments and expenditures of 7.3% and 2.6%, respectively, with both remaining below the previous year’s levels by 6.5% and 3.4%, respectively.

Summary

Despite various disruptions, freight volumes in January demonstrated a partial realignment with typical seasonal trends following an unseasonal decline in the fourth quarter. The slowdown in shipping activity over the Christmas and New Year’s holidays contributed to softer WoW comparisons early in the month, with tender volumes increasing by 18% and 21% WoW in the first two weeks. However, the return to normal operations was interrupted in the third week, as the FreightWaves SONAR OTVI recorded a 2% WoW decline, primarily due to disruptions associated with the Martin Luther King Jr. holiday. Outbound tenders rebounded in the final week of the month, increasing by nearly 5% WoW, bringing volumes back in line with levels observed during the second week.

Seasonal holiday effects and adverse weather conditions complicated both monthly and annual comparisons, limiting their ability to accurately reflect market trends. Excluding the volatility from early January, tender volumes during the second and third weeks averaged approximately 4% below December levels. By month-end, the tender volume index had increased 45% MoM, though largely due to weak prior-year comparisons. On an annual basis, tender volumes declined by 4.7% YoY during the first half of January compared to the same period in the previous year. However, trends in the latter half of the month fluctuated due to the timing of the Martin Luther King Jr. holiday, which occurred later this year. As a result, outbound tenders rose 3.6% YoY in the third week before declining to an average of 5.6% below YoY levels by month-end.

While contract volumes continued to dominate market share, spot load volumes gained momentum in January despite holiday- and weather-related disruptions. Sequential and annual comparisons were skewed in the first week due to New Year’s Day falling on a Wednesday. However, the onset of winter weather in the second week disrupted capacity, leading to spot load posts rising 12% YoY compared to the same week in 2024. These gains were short-lived, as capacity rebounded later in the month, resulting in a sequential decline of approximately 24% in the final two weeks. By month-end, spot load post volumes were 0.2% below prior-year levels.

Why It Matters:

January’s partial return to seasonal volume patterns does not provide a reliable indication of how the rest of the year will unfold. While the first quarter traditionally experiences softer demand, this year’s market faced additional challenges due to holiday timing and adverse winter weather, further hindering efforts to restore equilibrium.

The holiday calendar played a key role in early disruptions. With Christmas and New Years falling on Wednesdays, the shipping week was effectively shortened to just two days, resulting in a sharp decline in overall volumes and a sluggish start to the year. The final week of 2024 saw a 27% WoW drop in average outbound tenders – exceeding the three-year average decline of approximately 22% for the same period, when these holidays fell on a weekend or Monday. Additionally, Martin Luther King Jr. Day occurred later in January, just as demand was beginning to show signs of recovery. While not typically regarded as a major disruptor, this holiday has historically had a measurable, albeit smaller, impact on freight volumes compared to other Monday holidays, such as Memorial Day and Labor Day.

Macroeconomic factors also contributed to demand fluctuations. According to the latest Bank of America Consumer Checkpoint Report, consumer spending declined 0.2% YoY in January, following a modest 0.2% increase in December. Much of this downturn can be attributed to severe winter weather, which disrupted economic activity across large portions of the country. However, in unaffected regions such as the West, spending remained resilient. Additionally, as temperatures moderated in the latter half of the month, consumer spending rebounded across all regions.

While some January data suggests early signs of demand recovery—particularly with growth resuming in domestic manufacturing and new orders—significant challenges remain before the market will reach a true inflection point. Chief among these is the uncertainty surrounding potential trade policy shifts under the new administration. Proposed tariffs on key trading partners, along with anticipated retaliatory measures, present a considerable risk to economic stability. While viewpoints on these policies vary, the prevailing consensus among economists is that their implementation would likely lead to higher costs, accelerated inflation and slower economic growth – placing the greatest burden on consumers and domestic manufacturers. Should these policies take effect, they could further delay a meaningful recovery in demand and prolong current market challenges.