Back to February 2025 Industry Update

February 2025 Industry Update: Truckload Supply

Tender rejections retreated from holiday highs but remained elevated as winter storms delayed drivers returning to the road.

Key Points

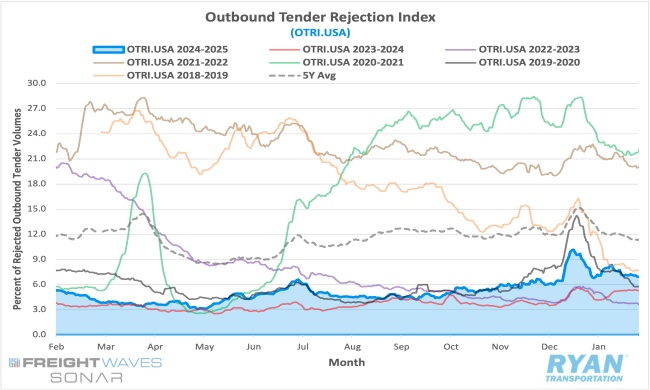

- The FreightWaves SONAR Outbound Tender Rejection Index (OTRI.USA), a measure of relative capacity based on carriers’ willingness to accept freight volumes under contract reflected as a percentage, was up 1.91% at the midway point in January compared to the midway point in December, up from 6.43% to 8.34%.

- The monthly average of daily tender rejections in January was down 30 bps MoM compared to December, falling from 7.71% to 7.41%.

- On an annual basis, average daily tender rejections were 2.53% higher YoY compared to January 2024 but 4.74% lower than the 5-year average.

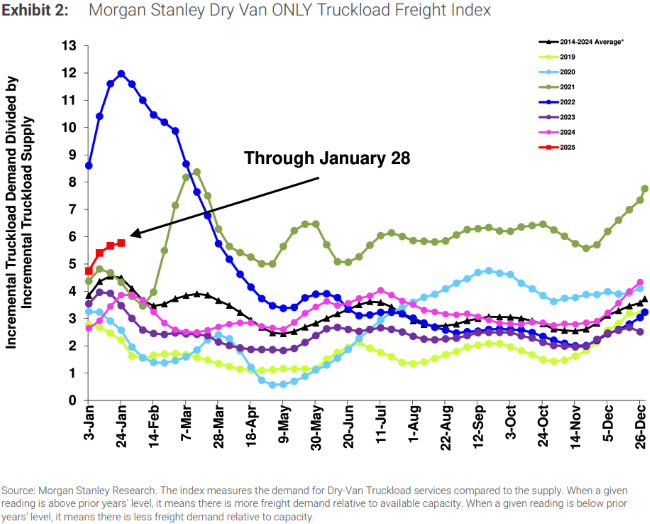

- The Morgan Stanley Truckload Freight Index (MSTLFI) registered sequential increases and outperformed typical seasonality in January, driven primarily by a strong performance in supply, keeping the index above the LT average.

Summary

Tender rejection rates stabilized in January after surging to their highest levels in over two years in the days leading up to Christmas. Following a 2.14% decline in the final week of 2024 from their pre-holiday peak, rejection rates continued to trend downward in early January, decreasing by an additional 96 bps to just over 7%. However, as Winter Storms Blair and Cora disrupted transportation networks nationwide, rejection rates spiked by 1.3% in the second week of January, reaching a monthly high of 8.34%. This increase was short-lived, as rejection rates resumed a downward trajectory for the remainder of the month, declining by 136 bps from their January peak to close at 6.95% – nearly a full percentage point below where they began.

While weekly volatility was evident, monthly comparisons in tender rejections reflected two distinct market phases. In the first half of January, rejection rates averaged 130 bps higher than during the same period in December, largely driven by weather-related disruptions. However, this trend reversed in the latter half of the month, with the average MoM comparison declining sharply to 195 bps below the second half of December. Despite these mid-month fluctuations, rejection rates remained elevated YoY, with the FreightWaves SONAR tender rejection index closing January 155 bps higher than the same period in 2024.

According to the latest Morgan Stanley report, the Truckload Freight Index outperformed typical seasonal patterns due to a sequential increase in demand alongside a corresponding decline in supply. The report noted that demand rose by 1,440 bps in January – well above the seasonal average increase of 500 bps – while supply levels fell by 1,210 bps, outperforming the typical monthly decline of 880 bps. Forward-looking sentiment appeared more optimistic than in previous updates, with respondents citing indications of tightening capacity amid rising demand. However, further capacity reductions are still necessary to drive a sustained market inflection.

Why It Matters:

Ongoing capacity reductions and supply contractions continued to increase market vulnerability to external disruptions in January. The combined effects of winter weather and holiday-related slowdowns contributed to persistently elevated tender rejection rates throughout the month, fueling speculation that truckload market conditions may be approaching a turning point. Although rejection rates retreated from their holiday peaks, they remained above typical seasonal trends, with January’s monthly average declining by only 30 basis points MoM –significantly less than the historical seasonal decline of 160 basis points for this period.

However, despite the resilience in tender rejections observed in January, truckload supply continues to outpace demand. According to the January Logistics Managers’ Index (LMI) report, the Transportation Capacity Index remained in expansion territory, registering 52.6% following a modest 0.5% decline from December’s reading. The report highlighted that available transportation capacity has not contracted since March 2022, as idle capacity continues to be reintroduced into the market, effectively absorbing incremental demand.

While market capacity is visibly tightening, the coming months are expected to pose challenges, as seasonal trends – absent further weather-related disruptions or demand shocks – will likely drive rejection rates lower. This, in turn, is expected to accelerate capacity exits ahead of produce season. Unlike previous cycles where demand-driven catalysts triggered a market shift, this cycle will continue to require the prolonged and gradual reduction in supply before any fundamental change can take place.