Back to January 2025 Industry Update

January 2025 Industry Update: Economy

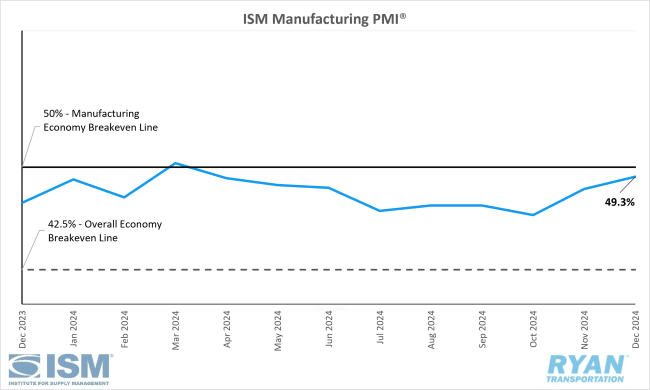

U.S. manufacturing activity contracted in December but at a slower rate than November as new orders and production grew.

United States ISM Manufacturing PMI

Key Points

- The ISM® Manufacturing PMI® registered 49.3% in December, a 0.9% increase from November’s reading of 48.4%.

- The New Orders Index remained in expansion territory in December, rising 2.1% from November’s reading of 50.4% to 52.5%.

- The Production Index registered 50.3% in December, 3.5% higher than November’s figure of 46.8% and moving the subindex back into expansion territory.

- The Employment Index dropped from November’s reading of 48.1% to 45.3% in December, moving deeper into contraction territory.

- The Prices Index registered 52.5% in December, a 2.2% increase from the 50.3% registered in November.

Summary

Manufacturing activity in the United States contracted for the ninth consecutive month in December, albeit at a slower pace than in November, according to the latest ISM® Manufacturing PMI® report. December’s figure represented the 25th occurrence in the past 26 months where the index remained below the 50% threshold. However, for the broader economy, December marked the 56th consecutive month of expansion, following a brief contraction in April 2020. (A Manufacturing PMI® reading above 42.5% over time generally indicates expansion in the overall economy.)

The deceleration in the contraction of manufacturing activity in December was primarily attributed to improved demand conditions, while output showed signs of stabilization and input factors remained favorable. The improvement in demand was most evident in the New Orders Index, which continued its upward trajectory, moving further into expansion territory. Additionally, the Backlog of Orders Index, though still in contraction, moderated its rate of decline, increasing by 4.1 percentage points to 45.9% in December. Another positive indicator for future demand was the Customers’ Inventories Index, which shifted further into “too low” territory, declining 1.7 percentage points from November’s 48.4% to 46.7%.

The output components of the composite index, represented by the Production and Employment indices, contributed positively to the Manufacturing PMI® calculation. The Production Index returned to expansion territory after six consecutive months of contraction, reflecting stabilized production levels compared to November, as companies prepared for alignment with 2025 operations. However, employment levels moved further into contraction in December as companies continued workforce reductions through layoffs, attrition and hiring freezes. According to the ISM® report, the hiring-to-staff reduction ratio increased to approximately 1-to-2 in December, compared to 1-to-1.5 in November, as organizations sought to streamline their workforces to conclude 2024.

Why it Matters:

December’s Manufacturing PMI® reading revealed several positive indicators for a sector that has been mired in contraction for much of the past two years. The increase in demand and stabilization of output suggests the possibility of a long-anticipated growth cycle on the horizon. However, despite these encouraging signs, the sector still faces significant challenges that must be addressed before consistent expansion can be achieved.

The report’s positive developments were largely reflected on the demand side, with new orders registering consecutive months of growth for the first time since the 24-month streak from June 2020 to June 2022 was interrupted. The continued strengthening of new orders bodes well for the sector’s potential return to growth, given the ripple effects these orders have across the supply chain. Another notable positive was the return of production levels to growth for the first time in six months. While the Employment Index's further contraction moderated the upward impact of production on the Manufacturing PMI® calculation, this decline was reportedly intentional. According to Timothy Fiore, Chair of the Institute for Supply Management® Manufacturing Business Survey Committee, the staffing reductions observed in December reflect manufacturers’ efforts to align workforce levels with revenue projections for the new year, and these adjustments are expected to conclude soon.

While the resurgence of manufacturing activity appears closer than it has been in some time, several headwinds could delay a sustained recovery. The Prices Index, for example, showed modest but consistent growth for the third consecutive month in December, increasing 2.2 percentage points from November’s reading of 50.3% to 52.5%. Fiore noted that pricing trends will be a critical focus in the months ahead, particularly in light of policy decisions by the incoming administration regarding tariffs and immigration, both of which could have inflationary effects. The ISM® report also highlighted that over one-third of survey respondents referenced tariffs, with many expressing concerns about their limited ability to pass price increases on to customers.

Another significant challenge for the manufacturing sector is the Federal Reserve’s approach to interest rates. While initial expectations included multiple rate cuts in 2025, current projections suggest the possibility of just one reduction during the year, which could further influence manufacturing activity and broader economic conditions.