Back to January 2025 Industry Update

January 2025 Industry Update: Truckload Rates

Capacity disruptions from the holidays led to both spot and contract rates trending higher in December.

Spot Rates

Key Points

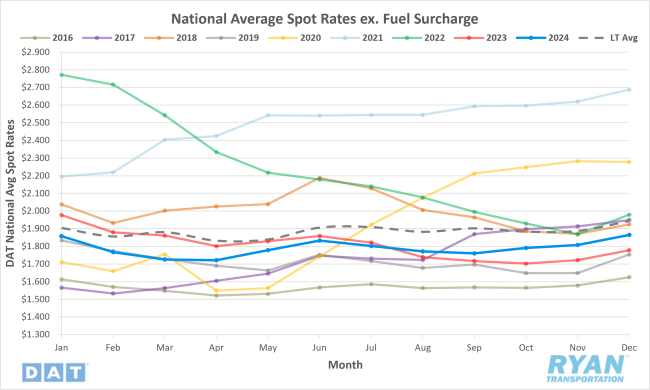

- The national average spot rate, excluding fuel, jumped in December, rising by just under $0.06 MoM, or 3.2%, to $1.87.

- Compared to December 2023, average spot linehaul rates were 4.9% higher YoY and were 4% below the long-term (LT) average.

Contract Rates

Key Points

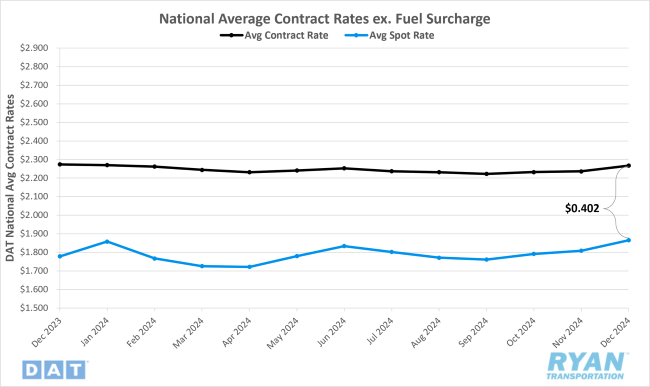

- Initially reported average contract rates excluding a fuel surcharge increased by just over $0.03 MoM, or 1.4%, to $2.27.

- On an annual basis, average contract linehaul rates were roughly flat compared to December 2023, registering just 0.3% lower YoY.

- The contract-to-spot spread narrowed further in December, dropping from $0.428 in November to $0.402 in December.

Summary

The national average spot rate, excluding fuel, increased for the third consecutive month in December, aligning with typical seasonal trends for the period. Driven by holiday-related capacity disruptions, the 3.2% MoM increase in December slightly exceeded the historical seasonal average MoM increase of 3.1%. December also marked the fifth consecutive month in which average linehaul spot rates remained elevated compared to 2023 levels. The rise in average spot rates further narrowed the gap between current and LT averages, with the spread steadily improving from its lowest point in September, when current rates were 7.4% lower, to just 4% below as of December.

According to weekly data from the DAT 7-day Linehaul Spot Rate Index, average spot rates exhibited consistent increases throughout the month, as anticipated. After modest gains in the first two weeks, totaling just over one cent per mile, the 7-day rolling average experienced a sharp uptick in the weeks leading up to Christmas, rising approximately $0.07 during this period. Following this surge, rates remained stable in the final week of December, with minor increases of fractions of a cent, culminating in a monthly gain of slightly more than $0.08 per mile.

The upward trend in rates observed in December extended beyond the spot market. Initial reports indicate that average contract rates also experienced notable gains during the month. According to DAT, average contract rates excluding fuel posted their largest MoM increase since November 2023, rising by approximately $0.04. On an annual basis, December’s YoY comparison for average contract linehaul rates fell to its lowest level since October 2022, registering a slight decline of 0.3%. With spot rate increases outpacing those in the contract market, the contract-to-spot spread narrowed further in December, reaching its lowest point since March 2022, when the current down-cycle began.

Why It Matters:

The rate increases observed in December were anticipated, given the month’s multiple capacity-disrupting holidays, which traditionally support stronger pricing in both the spot and contract markets. These disruptions, coupled with a persistently soft demand environment, suggest that December’s rate gains were largely driven by a contraction in available capacity. While supply levels continue to exceed demand, the alignment of spot rates with historical seasonal trends indicates that ongoing capacity exits are helping to maintain seasonality as the market seeks equilibrium.

Although the steady upward trajectory of spot rates in December exerted upward pressure on contract rates, evidence suggests that this momentum may not be sustainable in the near-term. With the current bid cycle underway, shippers are reportedly expecting contract rate increases in the low single-digit percentage range, according to a recent Journal of Commerce report. The 2025 State of the North American Supply Chain survey revealed that over 57% of shippers anticipate contract rate increases—up from approximately 52% last year—while 43% expect rates to remain flat or continue to decline.

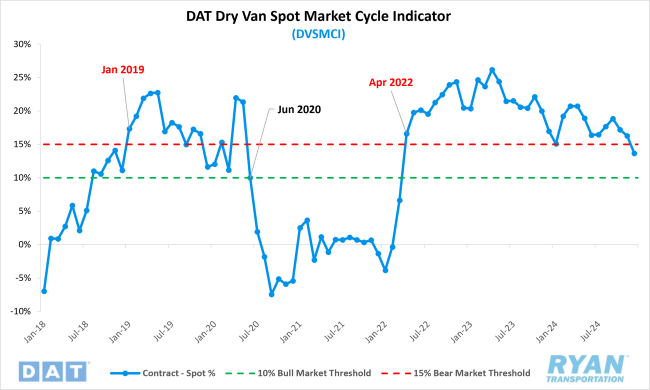

While December’s spike in spot rates was not unexpected, its significance should not be overlooked. According to the DAT Dry Van Spot Market Cycle Indicator (DVSMCI), which measures the spread between spot and contract rates relative to their average, December’s reading of 13.7% marked a significant improvement from November and represented the index’s lowest level since March 2022. Jason Miller, Interim Chair of Supply Chain Management at Michigan State University and creator of the DVSMCI, notes that a ratio above 15% reflects a bearish market, while a ratio below 10% signals a more bullish market. Although the index remains in bearish territory, it is trending toward an even more bullish position.

However, the typical January challenges, including inclement weather that disrupts capacity and travel, are likely to push rates higher in the short-term. As such, it will not be until February or March that a clearer determination can be made about whether the market has truly entered the inflationary phase of the truckload cycle.