Back to January 2025 Industry Update

January 2025 Industry Update: Truckload Supply

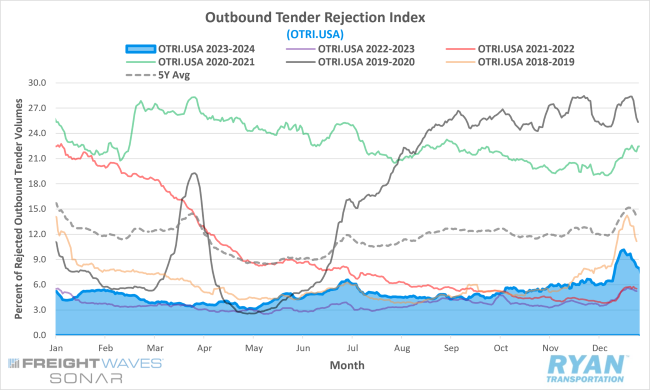

Tender rejections hit double digits for the first time in over two years as ongoing capacity exits and holiday disruptions led to increased volatility.

Key Points

- Mid-month comparisons of the FreightWaves SONAR Outbound Tender Rejection Index (OTRI.USA), a measure of relative capacity based on carriers’ willingness to accept freight volumes under contract reflected as a percentage, registered 43 basis points (bps) higher in December compared to November.

- The monthly average of daily tender rejections in December was 174 bps higher MoM, rising from 5.97% in November to 7.71% in December.

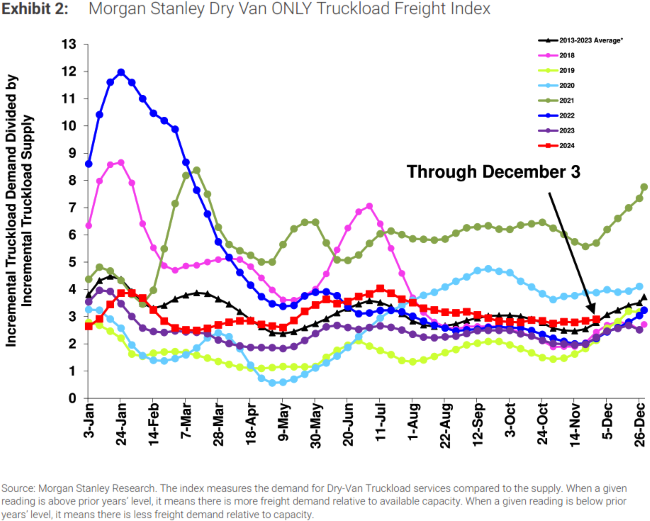

- On an annual basis, average daily tender rejections were up 3.3% compared to December 2023 and were 5.5% below the 5-year average.The Morgan Stanley Truckload Freight Index (MSTLFI) registered sequential increases throughout December and outperformed typical seasonality driven by strong outperformances in both the supply and demand components.

Summary

The combination of ongoing capacity contractions and multiple holiday disruptions resulted in the tender rejection index experiencing its strongest month in over two years this December, surpassing the 10% mark for the first time since April 2022. After rallying in late November to close the month at its highest level since July, rejection rates initially declined in early December, dropping 66 basis points (bps) during the first week to briefly fall below 6%. However, this decrease was short-lived, as tender rejections began a steady ascent in the second week, rising 46 bps by mid-December. Following this point, rejection rates surged by 373 bps to reach 10.16% in the days leading up to Christmas. The index remained above 10% for only two days before declining steadily through the remainder of the month, closing December slightly above 8%.

From a quarterly perspective, the sustained growth in rejection rates is particularly notable. Average tender rejections in Q4 reached their highest level since Q2 2022, with a quarterly average of 6.32%, reflecting a 155 bps increase QoQ compared to Q3 and a 232 bps increase YoY compared to Q4 2023. Since hitting a low in Q2 2023, average tender rejection rates have risen in five of the past six quarters. On an annual basis, December’s monthly average rejection rate was 3.3% higher YoY compared to December 2023, representing the largest YoY differential observed since July 2021.

Why It Matters:

The positive trend in rejection rates and the observed market volatility in December indicate that supply and demand levels are moving closer to equilibrium. Unlike previous cycles, where market recoveries were largely driven by demand growth, the current shift is reliant solely on the ongoing correction of excess capacity.

According to the latest Logistics Managers’ Index Report, the Transportation Capacity subindex remained in expansion territory in December, increasing by 0.6% MoM from 52.6% in November to 53.2%. This marks the third consecutive month of growth for the subindex, which continues to exceed the critical threshold. However, the subindex remains over 10 basis points (bps) below the average for 2023 and 16 bps lower than its December 2022 level.

Looking ahead to 2025, rejection rates are expected to decline during the first few months, driven by the return of drivers to the road post-holiday season and the typically lower seasonal freight volumes in Q1. However, March and April will be pivotal months to monitor as freight volumes begin to recover. Increased volatility during this period could signal that the market’s return to equilibrium is approaching sooner than anticipated.