Back to March 2025 Industry Update

March 2025 Industry Update: Economy

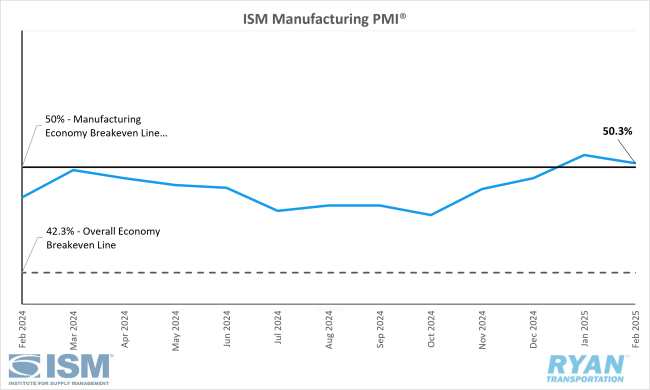

Manufacturing activity remained in moderate expansion territory in February despite a contraction in demand.

United States ISM Manufacturing PMI

Key Points

- The ISM® Manufacturing PMI® registered 50.3% in February, a 0.6% decrease from January’s reading of 50.9%.

- The New Orders Index contracted in February, dropping 6.5% from January’s reading of 55.1% to 48.6%.

- The Production Index registered 50.7% in February, 1.8% lower than January’s figure of 52.5%.

- The Employment Index returned to contraction territory, registering 47.6% in February, a 2.7% decrease from January’s reading of 50.3%.

- The Prices Index jumped 7.5% in February to 62.4%, up from January’s reading of 54.9%.

Summary

U.S. manufacturing activity experienced marginal expansion in February for the second consecutive month, following a prolonged 26-month period of contraction, according to the latest ISM® Manufacturing PMI® report. In the broader economic context, February’s reading marked the 58th consecutive month of expansion, apart from a brief contraction in April 2020. (A Manufacturing PMI® above 42.3% over time generally indicates overall economic growth.)

The report highlighted a weakening in demand, while output remained stable and input factors contributed positively to PMI® growth for the first time in several months. Notably, demand deterioration was most evident in the significant decline in new orders, pushing the subindex back into contraction after three months of expansion. The 6.5% decline from January represented the sharpest single-month drop since April 2020, when the index fell 15.1% from the prior month. Panelists cited a softening demand environment, with sentiment regarding near-term demand weakening to a 1.3-to-1 positive-to-negative ratio, down from 2-to-1 in January. Additional signs of demand weakness included continued contraction in the Backlog of Orders Index, albeit at a slower rate than in January, and a deceleration in new export order growth. However, one encouraging development was the Customers’ Inventories Index falling into “too low” territory, which typically signals potential future demand and production growth.

On the output side, the Production and Employment indices remained relatively stable in February, though their combined effect contributed a -4.5% impact on the Manufacturing PMI® calculation. Production remained in expansion for the second consecutive month, albeit at a slightly slower pace due to weak order books and sluggish new orders. Conversely, the Employment Index returned to contraction after a brief expansion in January, with continued workforce reductions driven by layoffs, attrition and hiring freezes. Survey respondents reported a second consecutive month of a 1-to-1 hiring-to-reducing ratio.

The report also indicated signs of supplier challenges, with the key input indices (supplier deliveries, inventories, prices and imports) reflecting disruptions.

The Supplier Deliveries Index rose to 54.5% in February, up 3.6 percentage points from January’s 50.9%, suggesting that supplier delivery performance is slowing. Accelerated delivery requests – driven by concerns over potential port strikes and tariff implementation – as well as ongoing negotiations regarding tariff-related costs, contributed to these delays. Anticipation of tariffs also fueled rising input costs, with the Prices Index recording its largest MoM increase since a 7.7% surge in January 2024. Despite tariffs not taking effect until mid-March, spot commodity prices have already risen approximately 20%, according to the report.

Among the six largest U.S. manufacturing industries – Chemical Products, Transportation Equipment, Computer & Electronic Products, Food, Beverage & Tobacco Products, Machinery and Petroleum & Coal Products – four reported growth in February: (Petroleum & Coal Products, Food, Beverage & Tobacco Products, Chemical Products and Transportation Equipment).

Why it Matters:

While February’s Manufacturing PMI® reading of 50.3% marks a noteworthy development – signifying consecutive months of expansion in manufacturing activity following more than two years of contraction – market attention has largely shifted toward the uncertainties surrounding potential import duties imposed by the new administration. The concerns over tariffs, which were initially subdued by a resurgence in demand in January, escalated into a dominant focal point in February, exerting broad impacts across the composite index. Unlike January’s largely optimistic report, which suggested the potential beginning of an expansion cycle for the U.S. manufacturing sector, February’s report presents a more cautious outlook.

The planned tariffs on imports from two of the United States’ three largest trading partners, which had been paused in January, are now scheduled to take effect on March 4. According to Timothy Fiore, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee, suppliers are limiting new orders, as many are unwilling to make deliveries until an agreement is reached regarding responsibility for the tariffs that have already been implemented. Fiore noted that while suppliers navigated similar challenges in 2018, they are taking a more proactive approach this time rather than waiting to assess the full extent of the impact. This reluctance among suppliers appears to have been a key factor in the decline of new orders, leading the subindex to return to contraction in February. Additionally, ongoing negotiations between buyers and suppliers regarding tariff costs contributed to an elevated Supplier Deliveries Index of 54.5%, which ultimately kept the overall Manufacturing PMI® in expansion territory. According to Fiore, had supplier delivery performance remained consistent with recent trends, the PMI® would have likely slipped back into contraction, registering closer to 48.5%.

The most significant impact of tariff concerns, however, was reflected in the sharp increase in the Prices Index – deemed the “story of the month” by Fiore. In February, the index measuring price movements reached its highest level since hitting 78.5% in June 2022. According to the ISM® Supply Chain Planning Forecast released in December, manufacturers have expressed reduced confidence in their ability to pass cost increases onto customers in the current economic climate. This inflationary pressure is particularly concerning given that the majority of tariffs have yet to take effect. The rising Prices Index is expected to be mirrored in upcoming Consumer Price Index (CPI) and Producer Price Index (PPI) readings, which remain closely monitored by the Federal Reserve. Any increase in these indices could heighten the likelihood of further interest rate hikes. As demonstrated throughout 2023 and early 2024, a higher cost of capital would likely hinder any manufacturing recovery and prolong the ongoing freight recession.

Macro Economy

- Core consumer prices and the Fed’s preferred inflation gauge rose in January by 2.6% YoY, matching expectations and slowing from the 2.9% rate in December which was revised upward from the initially reported 2.8%, according to the most recent Personal Income and Outlays Report from the Bureau of Economic Activity (BEA).

- Core Personal Consumptions Expenditures (PCE) Index, which excludes volatile food and energy prices, increased 0.3% MoM in January, up slightly from the 0.2% MoM increase registered in December.

- Meanwhile, headline PCE in January was up 0.3% MoM, matching the prior month’s increase and translated to a YoY increase of 2.5%, slightly lower than December’s 2.5% figure.

- Inflation cooled in February according to latest Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) Report, as headline CPI rose 2.8% on a seasonally adjusted annual basis, down from the 3.0% increase recorded in January.

- Excluding food and energy prices, core CPI rose 3.1% compared to last year and 0.2% lower than the 3.3% increase in January.

- On a monthly basis, both headline and core CPI rose +0.2% versus the consensus of +0.3% for both and were lower than increases registered in January of 0.5% and 0.4%, respectively.