Back to March 2025 Industry Update

March 2025 Industry Update: Flatbed

Average rates remained flat MoM despite warmer weather leading to an increase in flatbed activity.

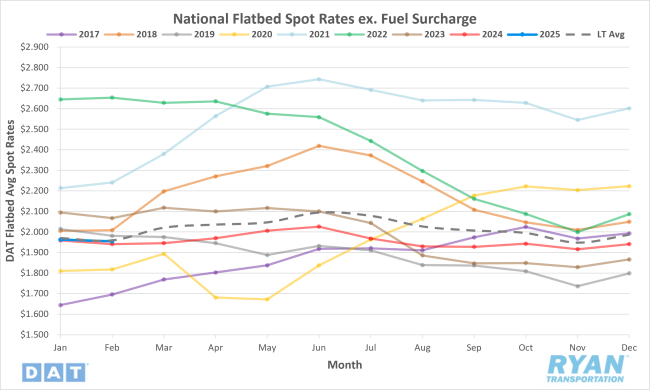

Spot Rates

Key Points

- The national average flatbed spot rate excluding a fuel surcharge was essentially flat MoM in February, registering 0.4% lower, or just under a penny per mile, to $1.96.

- Average flatbed spot linehaul rates in February were up 0.7% YoY compared to February 2024, but were 1.7% below the LT average.

- The initially reported flatbed contract rate excluding any surcharges declined 1.5% MoM but were up slightly by 0.2% compared to average contract rates during the same month last year.

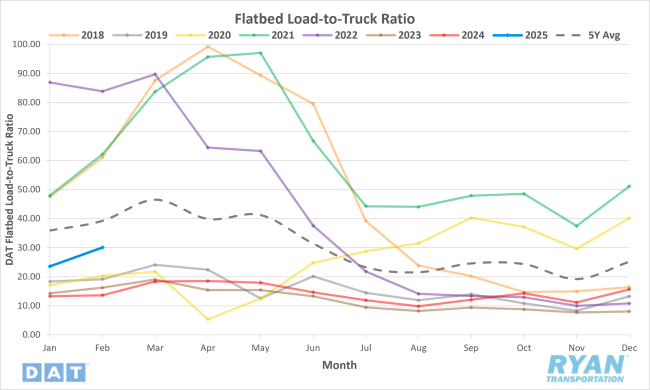

Load-to-Truck Ratio

Key Points

- The flatbed LTR registered a 27.8% MoM increase in February to 30.1.

- Compared to February 2024, the flatbed LTR was 120.7% higher YoY but registered 23.3% below the 5-year average.

- Flatbed load post volumes on the DAT load boards were up 15.7% MoM in February, while equipment posts fell 9.4% MoM compared to January.

Market Conditions

Flatbed Summary

Demand is going to be on the rise from March – June with infrastructure projects, residential construction and industrial shipments driving volume with key areas including TX, the Southeast and the Midwest. With impending tariffs on the horizon, many builders may be looking to freight-forward as many construction inputs as possible before the tariffs go into effect. According to the latest report from the American Trucking Association’s For-Hire Truck Tonnage Index, trucking activity contracted in December, the second decrease in as many months. ATA Chief Economist Bob Costello noted, “For the first time since March and April, truck tonnage contracted for two consecutive months.” The two-month total decrease was 2.9% pushing tonnage to its lowest level since January 2024 and down 3.2% from the same month last year. Costello also noted that, “Sluggishness in factory output continues to weigh on freight volumes, but another drag on the index has been fleet growth at private carriers, which is holding back how much freight is flowing to for-hire carriers.”

Caterpillar Inc., a bellwether for global economic growth for flatbed and specialized truckload carriers, announced Q4 and full-year results for 2024. Sales and revenue in Q4 were $16.2 billion, a 5% decrease from Q4 2023, and full-year sales and revenue were $64.8 billion, down 3% from 2023. Lower sales volume was primarily driven by lower sales of equipment for end-users. According to Bloomberg, “Investors have been concerned by elevated inventories, as high inventories suggest customers aren’t buying machines off dealer lots and indicates weak consumption.” Additionally, Volvo Construction Equipment reported North American sales were $8.0 billion in fiscal year 2024, down 15% from the previous year. Sales were down 20% as the North American total machine market contracted due to a normalization of replenished dealer and rental fleets.