Back to March 2025 Industry Update

March 2025 Industry Update: Intermodal

Growth in intermodal volumes continues to keep overall volumes elevated YoY despite further weakness in carload volumes, while rates remain near historic lows.

Spot Rates

Key Points

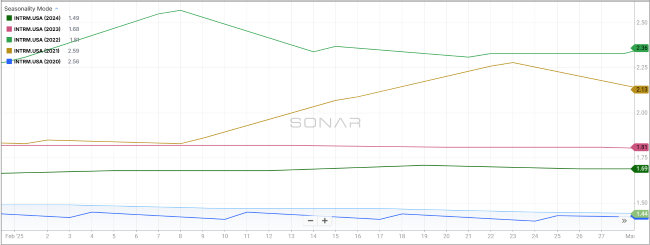

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door spot rate for 53’ dry vans across a majority of origin-destination pairings, ended February $0.05 lower MoM compared to January at $1.44.

- Compared to February 2024, intermodal spot rates were down 14.8% YoY and were 24.5% below the 5-year average.

Volumes

Key Points

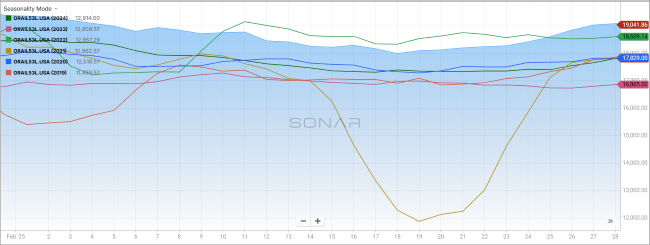

- Total loaded volumes for 53’ containers for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), declined by 1.5% MoM at the end of the month compared to 30 days prior, falling from 19,388.57 at the end of January to 19,091.14 in February.

- Loaded domestic volumes for 53’ containers in February were up 7.2% YoY compared to February of last year and 7.3% higher than the 5-year average.

Intermodal Summary

Rail activity sustained its positive momentum in February, despite weather-related disruptions and ongoing uncertainty surrounding trade policy. According to the latest report from the Association of American Railroads (AAR), rail traffic exhibited a mix of strengths and challenges, with certain sectors demonstrating resilience while others faced headwinds amid evolving market conditions. The continued strength of consumer-driven commodities, coupled with efforts by some importers to expedite shipments ahead of potential tariffs, contributed to a 6.4% YoY increase in intermodal volumes, equating to an additional 66,340 units, per the report. Furthermore, intermodal volumes for the first two months of the year rose 8.5% YoY, with container volumes increasing 9.5% to reach their highest YTD level on record for this period.

Meanwhile, after experiencing a slight uptick in January – the first in five months – carload volumes declined by 4.5% YoY in February, equating to a reduction of 39,547 units compared to the same period in 2024. The report notes that while six of the 20 carload commodities tracked by the AAR recorded growth, coal – the highest-volume carload commodity – declined by 8.2% YoY, marking its 14th consecutive monthly decline. Excluding coal, carload volumes were still down 3.1% YoY, or 19,855 units. Given the ongoing softness in key industrial sectors, combined with weather-related disruptions, U.S. rail carloads declined by 2.0% YTD through the first two months of the year.

Despite rail continuing to gain market share, the strong performance has not yet translated into significant pricing shifts, based on FreightWaves SONAR rail indices. The FreightWaves SONAR IMCRPM1.USA index, which tracks initially reported average contract rates excluding fuel, showed that contract rates ended February at $1.60, a decrease of $0.04 from January’s $1.64. Compared to 2024 levels, average intermodal contract linehaul rates declined by $0.02 YoY. Similarly, intermodal spot rates, which indicate whether intermodal carriers are prioritizing contract capacity for shippers, declined on both a monthly and annual basis in February, reaching their lowest level since early September 2024.