Back to March 2025 Industry Update

March 2025 Industry Update: Truckload Capacity Outlook

Declines in the carrier population have continued to stabilize but remain well above pre-pandemic levels while payroll figures have essentially normalized.

Key Points

- Total net revocations, a measure of total authority rejections minus reinstatements, fell by 305 carriers in February, dropping from 4,645 total revocations in January to 4,340 in February, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- The number of newly authorized for-hire trucking companies rose in February by 326 carriers, increasing from 3,759 in January to 4,085 in February.

- Preliminary North American Class 8 Order estimates in February ranged from 17,000 units as reported by FTR to 18,300 units per ACT Research, with both estimates reporting significantly lower YoY by 32.7% and 34.0%, respectively.

Summary

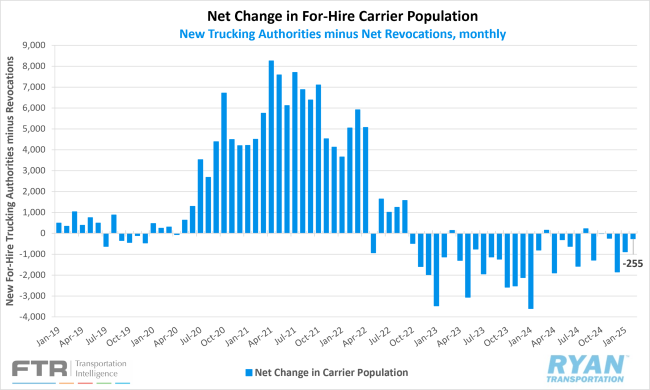

Capacity exits continued to show signs of stabilization, with the net change in the active for-hire carrier population declining by 255 carriers in February, a notable improvement from the 886-carrier decline recorded in January. February represented the third-lowest contraction in the active for-hire carrier population since the onset of widespread carrier exits in late 2022, trailing only the modest declines observed in October (-12) and November (-236) of last year. Further evidence of stabilizing capacity conditions is reflected in the downward trend of annual average declines. The average net decrease in the carrier population has moderated from just over 1,750 carriers in 2023 to approximately 1,000 in 2024, with the YTD average through February registering just over 570 carriers.

The deceleration in carrier exits continues to be driven by a moderation in both net revocations and new authority issuances. According to FTR, new carrier authorizations granted by the FMCSA increased by 326 in February compared to January, while net revocations less reinstatements declined by over 300 carriers MoM. Since 2023, the average monthly revocation count has fallen by nearly 2,750 carriers, dropping from approximately 7,250 in 2023 to 4,500 in January and February 2024. Meanwhile, new carrier authorizations have declined from approximately 5,500 per month to around 4,000 over the same period. FTR’s analysis indicates that the number of authorized carriers remains approximately 35% – or nearly 89,000 carriers – above February 2020 levels, prior to the pandemic.

On the equipment side, preliminary North American Class 8 orders continued to soften in February as concerns over tariffs and broader market uncertainty further dampened equipment investment. According to FTR, February’s net orders totaled 17,000 units, significantly below seasonal expectations and well short of the seven-year average of 26,912 units for the month. Notably, for the first time since the start of the 2025 ordering cycle, cumulative net orders from September 2024 to February 2025 declined on an annual basis, down 3% YoY. ACT Research echoed similar findings, noting that order activity over the past two months has been largely influenced by uncertainty surrounding economic and trade policies. ACT’s analysis, adjusted for seasonality, placed February’s order total at approximately 16,700 units – a 28% MoM decline from January and the lowest seasonally adjusted figure in nearly two years.

Why It Matters:

The ongoing stabilization of the active for-hire carrier population remains a point of concern, as truckload market conditions have yet to show significant improvement. While initial speculation suggested that early signs of an inflection point contributed to a slowdown in capacity exits, alternative theories indicate that multiple factors may be influencing this trend.

One frequently cited factor contributing to the resilience of for-hire carriers is the financial cushion afforded by historically high spot rates from mid-2020 through early 2022. According to Census Bureau data, non-employer firms experienced revenue growth of 8.7% in 2020 and 20.7% in 2021, outperforming employer firms in both years. Coupled with government support measures, such as stimulus payments and loan forgiveness, smaller carriers have been able to withstand financial pressures longer than initially anticipated. Additional contributing factors include advancements in technology that have enabled carriers to source business opportunities more efficiently, lender forbearance driven by an unwillingness to repossess equipment in the current market, and the reluctance of financially stressed carriers to exit the industry before benefiting from a potential market recovery.

While the carrier population has yet to return to pre-pandemic levels, payroll employment in the sector has largely normalized. According to the latest Bureau of Labor Statistics (BLS) jobs report, for-hire trucking employment declined by 1,900 jobs in February, following downward revisions to December and January estimates. Initially, the sector was believed to have added 4,100 jobs over those two months, but the latest data reflects a net loss of 800 jobs. Preliminary BLS figures indicated that truckload employment had increased by 7,400 jobs between November 2024 and January 2025. However, revised data now shows a gain of just 600 jobs between November 2024 and February 2025. Additionally, following annual benchmark revisions in January – adjusting employment levels from 1.7% above to just 0.3% above February 2020 – the most recent data suggests that payroll employment is now only 0.1% higher than its pre-pandemic level.