Back to March 2025 Industry Update

March 2025 Industry Update: Truckload Demand

A surge in inventory levels failed to translate to freight volumes as declines in demand underperformed typical seasonality.

Key Points

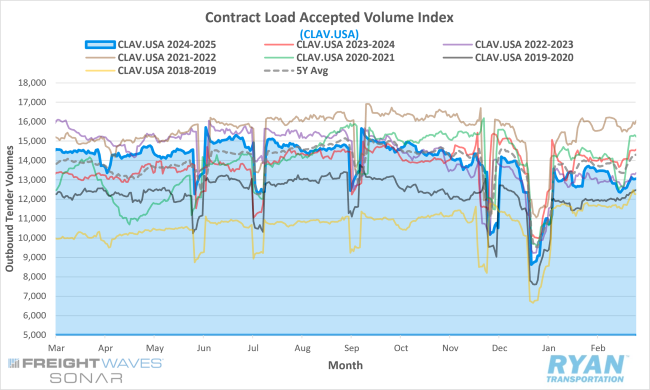

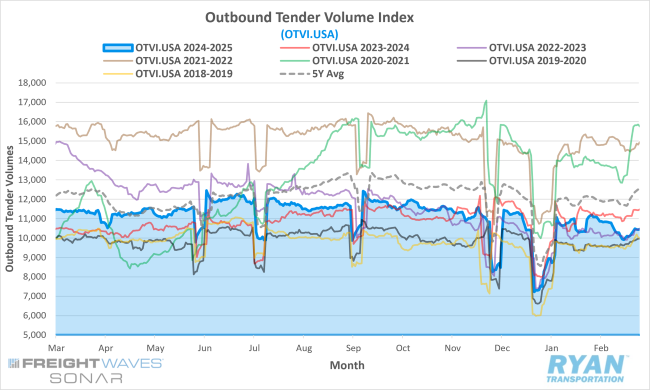

- The FreightWaves SONAR Outbound Tender Volumes Index (OTVI.USA), a measure of contracted tender volumes across modes, declined by 5.9% MoM at the end of the month compared to the levels recorded 30 days prior, dropping from 11,097.14 in January to 10,438.37 in February.

- The 21-day trailing monthly average of daily tender volumes in February fell 3.4% MoM compared to January, dropping from 10,725.20 to 10,356.01.

- Compared to February 2024, average daily tender volumes were down 6.1% YoY and registered 12.3% below the 5-year average.

- Spot market activity stalled in February after two consecutive months of gains with load post volumes dropping 11.7% MoM but registered 14.8% higher compared to February 2024 levels.

- The Cass Freight index Report, which analyzes the number of freight shipments across North America and the total dollar value spent on those shipments, registered MoM declines in January for both shipments and expenditures of 5.3% and 4.8%, respectively, with both remaining below the previous year’s levels by 8.2% and 4.2%, respectively.

Summary

Following a somewhat relatively stable January despite the various holiday and weather disruptions, freight volumes slowed significantly in February, making the month a particularly difficult one in the truckload industry. While a seasonal depression in demand is typical during the second month of the year, continual shifts in trade policies led to a surge in orders pulled forward in late January, further exacerbating the declines observed in the latter part of February.

After rebounding from the freight activity slowdown caused by the Martin Luther King Jr. holiday in late January, tender volumes, as measured by FreightWaves SONAR OTVI, showed a modest WoW increase of approximately 0.2% at the beginning of February. However, as seasonal pressures intensified, this momentum was short-lived. By the second week, the OTVI had declined 1.7% WoW before experiencing one of the most significant weekly drops in the past two years – down 6.6% – midway through the month. Despite these challenges, the final week of February saw some stabilization in tender volumes with the OTVI rising 1.6% WoW, but still ended the month nearly 6% below the levels at the start of the month.

Although the weekly fluctuations in demand mirrored the seasonal patterns observed in February over the last two years, the increasing weakness in YoY comparisons does present a cause for concern. Through the first half of the month, outbound tender volumes averaged roughly 2.9% lower YoY compared to the same time in 2024. However, that gap widened substantially in the second half of the month, dropping to an average of 8.4% lower YoY before ultimately ending the month down 8.8% YoY compared to 2024.

Breaking down February’s volume declines by mode, the refrigerated sector performed the worst of the three major mode types on a monthly basis while dry van activity has suffered the most compared to 2024 levels. According to FreightWaves SONAR tender volume indices for each specific mode, after rallying toward the end of last year that carried over through the beginning of the 2025, reefer volumes dropped considerably in February, registering 18.6% lower MoM compared to January and marked one of the largest MoM declines since COVID. On an annual basis, after registering higher YoY for much of the previous two months, refrigerated volumes declined 3.9% YoY. On the other side, dry van volumes fell 5.9% MoM but are down 10.1% YoY.

Why It Matters:

The declines in freight volumes across all modes is not unprecedented for February by any means, however, the rate of those declines does appear to be more of an anomaly. While seasonality played its part, impacts from tariff uncertainty, slowing consumer spending and retail sales as well as rising inventory levels, both upstream and downstream, suggest that no singular cause was responsible for a majority of the declines but rather it was the combination of these smaller issues that led to the considerable drop in volumes.

Of all the potential factors that contributed to the accelerated deterioration of freight volumes last month, none have dominated the 24-hour news cycle more than the uncertainties surrounding the potential changes in trade regulations. Although initial speculation was that the threat of tariffs under the current Trump administration was likely a negotiation tactic, many shippers and companies were unwilling to wait and find out, as evident in the February 2025 LMI® report. According to the report, inventory levels in February expanded at their fastest rate since June 2022, with the peak of that expansion occurring in the first half of the month as shippers worked to stay ahead of potential tariffs before tapering off in the second half. However, despite the slowing of expansion in inventory levels, the associated costs continued to expand at their fastest rate in several years, an indication that firms are holding the high levels of inventories static in hopes to slowly sell them off over time. The report notes that the buildup of inventory levels is a sharp deviation from the just-in-time (JIT) inventory strategies that were prevalent in 2024 and more in line with the just-in-case (JIC) policies from 2021, which was a major contributor to the inflation of 2021 and 2022.

Looking ahead, the extent in which demand can rebound in March and the coming months will be under close examination to provide any sort of signal for where the market is on the recovery timeline. Although seasonal factors are expected to gain strength over the next several months as summer merchandise starts to move and early produce volumes ramp up, there are still quite a few hurdles to overcome, not just within the transportation industry but in the macroeconomic and political climates as well. Current forecasts for when the cycle will reach an inflection point have been widespread and are likely to remain that way while uncertainties regarding policies and trade regulations persist. Putting those aside, however, the truckload industry is still in need of a demand catalyst that can only ultimately come from the manufacturing sector. While the wholesale and retail sectors have helped keep the industry relatively propped up over the past two years, cracks in consumer strength are beginning to show. Without a rebound in domestic manufacturing to spur demand, the market will continue to rely on further supply contractions, which will undoubtedly extend the current industry recession.