Back to November 2024 Industry Update

November 2024 Industry Update: Economy

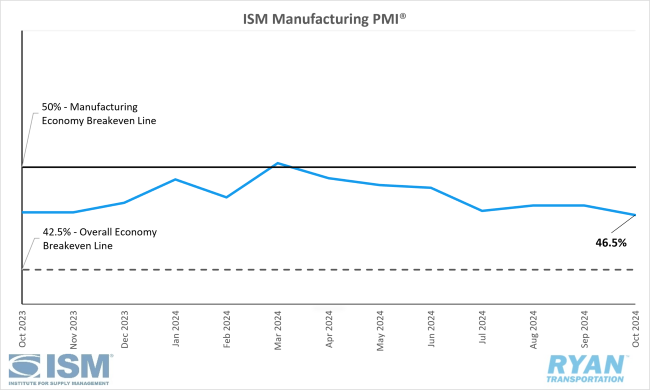

Manufacturing activity remained sluggish in October as the ISM® Manufacturing PMI® remained in contraction, driven by weaker new orders and reduced production.

United States ISM Manufacturing PMI

Key Points

- The ISM® Manufacturing PMI® registered 46.5% in October, a 0.7% decrease from September’s reading of 47.2%.

- The New Orders Index remained in contraction territory, registering 47.1% in October, 1.0% higher than September’s figure of 46.1%.

- The Production Index fell 3.6% from the 49.8% reading in September to 46.2% in October.

- The Employment Index contracted at a slower rate in October than September, registering a 0.5% increase from 43.9% in September to 44.4% in October.

- The Backlog of Orders Index moved deeper into contraction territory in October, registering 1.8% lower than September’s reading of 44.1% to 42.3%.

Summary

U.S. manufacturing activity declined for the seventh consecutive month in October, accelerating from September’s contraction, as reported in the latest ISM® Manufacturing PMI® release. With the index remaining below 50%, manufacturing has now contracted in 23 of the past 24 months. Nonetheless, the broader economy marked its 54th month of expansion in October. (A Manufacturing PMI® above 42.5% generally signals overall economic growth over time.)

Demand indicators weakened further in October, as both the New Orders and Backlog of Orders indices contracted at a greater rate than in September. ISM® report panelists noted ongoing uncertainty and concern about the scarcity of new orders, with a 1-to-1.2 ratio of positive to concerned comments regarding near-term demand. This lack of new orders caused the Backlog of Orders Index to enter deeper contraction territory. However, one positive sign for future demand and production was the Customers’ Inventories Index, which decreased to the upper end of the “too low” range.

The output components of the composite index, measured by the Production and Employment indices, contributed a -3.1% impact to the Manufacturing PMI® and remained in contraction in October. Employment declined, though at a slower pace than in September. According to the ISM® report, the Employment Index readings in July, September and October were the lowest since July 2020, when the index registered 43.7% during the early stages of the post-pandemic recovery. Layoffs, attrition and hiring freezes primarily drove headcount reductions, with a hiring-to-reduction comment ratio of approximately 1-to-3. Production activity continued to decrease as new orders and backlogs remained low, prompting manufacturers to adjust output and plan for reduced production through year-end.

Among the six largest manufacturing industries — Machinery; Transportation Equipment; Fabricated Metal Products; Food, Beverage & Tobacco Products; Chemical Products; and Computer & Electronic Products — only two (Food, Beverage & Tobacco Products and Computer & Electronic Products) recorded expansion in October, up from one in September.

Why it Matters:

The October Manufacturing PMI® reading continued to highlight challenges that have impacted the manufacturing sector over the past two years, with weak demand leading to reduced output, despite accommodative input levels. October’s PMI® came in below expectations, with economists previously forecasting a slight uptick to 47.6% from September’s level. While weak demand and lowered production remain key obstacles, October’s PMI® shortfall was also influenced by disruptions from recent hurricanes and port strikes. Although the full impact of Hurricanes Helene and Milton remains unclear, respondents reported that storm-related damage to energy and electrical infrastructures affected multiple industries with heavy dependence on those resources.

As noted in prior reports, the subdued demand environment is driven largely by companies’ reluctance to invest in capital and inventory ahead of the November elections. This hesitancy is attributed to uncertainties around federal monetary policy, given the contrasting fiscal approaches proposed by the two major parties and concerns about a potential resurgence in inflation. According to Timothy Fiore, Chair of the Institute for Supply Management® Manufacturing Business Survey Committee, respondents have voiced concerns regarding policy stances from both major candidates, including those related to tariffs and protectionism. However, regardless of the election outcome and subsequent policies, growth in the manufacturing sector is unlikely to resume until January or February, when the new administration is in place.

In a report released by FTR in October that analyzed the ongoing manufacturing slump, the company projected the return of annual growth in manufacturing production to come in 2025 at a marginal rate of 0.9% YoY, slightly stronger than the 0.3% uptick in their previous outlook. The firm’s longer-term projections put manufacturing output up by 1.0% YoY in 2026, which was revised down from 1.2% YoY in their earlier forecasts. While that roughly 1% increase pales in comparison to the gains of 5.0% and 2.7% observed in 2021 and 2022, respectively, it nonetheless marks an improvement over the recent period of stagnation. Per the report, the growth projections in manufacturing output over the next two years is likely not going to be equally distributed across industries. FTR anticipates growth in non-durable goods (+1.1% YoY) to outpace the annual rise in durable goods consumption (+0.7%) in 2025 with the latter outpacing the former by a slimmer margin in 2026. Durable goods were a driving force behind the surge in freight volumes in 2021 and are generally tied to higher overall demand within the transportation sector.

Macro Economy

- Non-farm payroll employment added 12,000 jobs MoM in October on a seasonally adjusted basis following downward revisions to both August and September estimates, according to the most recent jobs report released by the Bureau of Labor Statistics (BLS).

- The unemployment rate remained unchanged at 4.1% in October from September.

- Transportation and Warehousing employment declined by 3,700 jobs MoM in October on a seasonally adjusted basis.

- Truck Transportation shed just 100 jobs MoM in October.

- Warehousing and Storage declined by 7,000 jobs MoM.

- Both headline and Core Personal Consumption Expenditures (PCE) indices rose in September as the all-items index rose by 0.2% MoM and all-items less food and energy registered a 0.3% increase MoM on a seasonally adjusted basis, according to the most recent report released by the Bureau of Economic Analysis (BEA).

- On an annual basis, the headline PCE index increased by 2.1% YoY in September on a seasonally adjusted basis and was 0.2% lower than August’s increase of 2.3%.

- Excluding food and energy, the PCE Index rose by a seasonally adjusted 2.7% YoY in September and was unchanged from August.