Back to November 2024 Industry Update

November 2024 Industry Update: Fuel

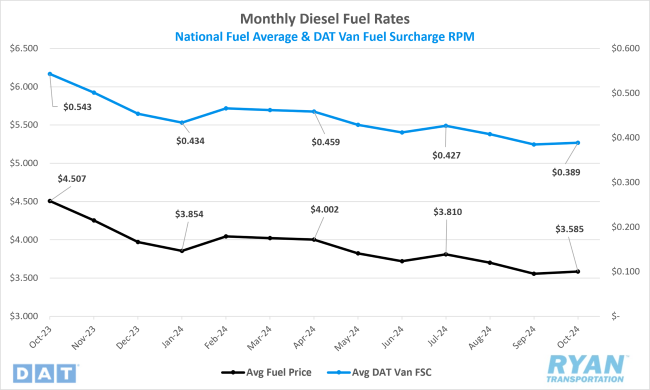

The average benchmark price of diesel rose slightly in October amidst rising tensions in the Middle East.

Key Points

- The national average price of diesel rose in October, increasing 0.8% MoM, or just under $0.03, to $3.59.

- Compared to October 2023, diesel prices were 20.4%, or just over $0.92, lower in October.

- Builds on U.S. Commercial Crude inventories outpaced draws by 8.6M barrels (bbls) and outperformed the consensus of 7.3M bbls for the weeks ending October 4 and October 25, according to data released by the Energy Information Administration (EIA).

Summary

Average fuel prices saw a modest increase in October following notable declines in August and September. Despite this rise, diesel prices remain below levels last seen in September 2021, when the average price was $3.38. October’s increase in the monthly benchmark price for diesel represents only the third MoM gain in the past year, with no consecutive increases. On a weekly basis, fuel prices rose in three of the four weeks during October, with the only weekly decline occurring in the third week, where average prices dropped nearly $0.08 – the largest weekly drop since December 18.

In parallel, U.S. commercial crude reserves experienced builds outpacing draws in October for the first time since April. Much of this increase in stockpiles resulted from the peak refinery maintenance season, which began in late September and extended through much of October. Data from the Energy Information Administration (EIA) indicated that refinery utilization rates dropped to 86.7% at the start of October after five consecutive weeks of decline, remaining below 90% for the remainder of the month. Concurrently, U.S. crude production reached a record high of 13.5 million bbls/day in October, up from 13.3 million bbls/day at the end of 2023 and surpassing the 13.4 million bbls/day recorded in August.

Why It Matters:

Despite the ongoing global challenge of supply exceeding demand, the rise in average fuel prices in October was primarily driven by heightened geopolitical concerns, particularly related to escalating tensions in the Middle East and, specifically, the conflict between Israel and Iran. Early in the month, Iranian missile strikes on Israel spurred fears that Israel might retaliate by targeting Iran’s oil industry, prompting a sharp increase in futures prices for ultra-low sulfur diesel (ULSD). However, these concerns eased after Israel assured U.S. officials that it would not target Iranian oil infrastructure in any potential retaliation. Although futures prices stabilized, retail prices continued to rise in the subsequent week due to the lag in retail response to future market changes.

While ongoing fears of supply disruptions from Middle East tensions periodically spike fuel prices, actual output losses remain minimal following the October 7 attack on Israel. In fact, the most significant disruption to oil supplies has come from Houthi-led attacks on shipping in the Red Sea, which caused minor diversions from the Suez Canal to the Cape of Good Hope. These events, however, have had minimal impact on prices. According to the latest International Energy Agency (IEA) report, global demand growth projections for 2024 have been revised down by roughly 40,000 to 50,000 bbls/day from the previous forecast. Per the report, as supply continues to flow and in the absence of any major disruptions, the market will be faced with a sizeable surplus in the new year.