Back to November 2024 Industry Update

November Industry Update: Intermodal

Intermodal volumes remained robust in October despite weakening carload traffic, while rates trended negatively.

Spot Rates

Key Points

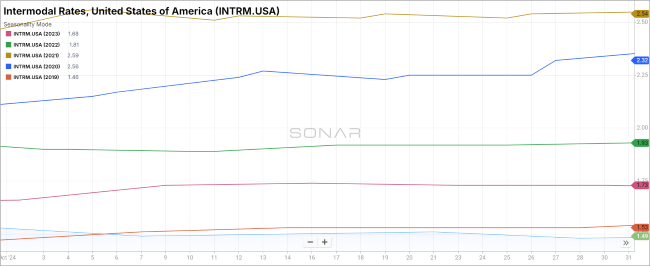

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door intermodal spot rate for 53’ dry vans across a majority of origin-destination pairings, registered a 3.3% decline MoM, or $0.05, in October, to $1.48.

- Compared to October 2023, intermodal spot rates were down 14.5% and registered 26.4% below the 5-year average.

Volumes

Key Points

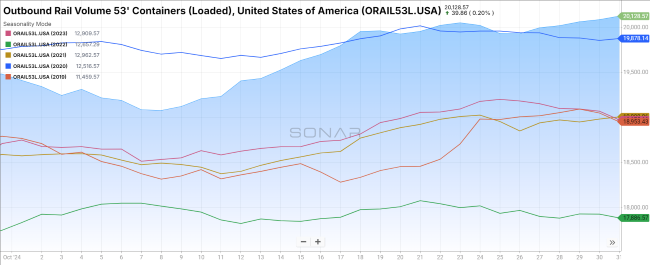

- Total loaded volumes for 53’ container for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), increased 3.3% MoM at the end of October compared to the end of September.

- Total loaded volumes for 53’ containers in October registered 6.1% higher compared to October 2023 and was 6.3% higher than the 5-year average.

Intermodal Summary

Rail activity remained strong in October, driven by sustained consumer spending and import demand, which has supported elevated intermodal volumes as the peak retail shipping season approaches. According to the latest report from the Association of American Railroads (AAR), U.S. railroads originated 1,410,083 intermodal containers and trailers in October, marking a 5.5% YoY increase compared to October 2023. This makes October one of the strongest months for intermodal traffic in 2024, with an average weekly movement of 280,000 units.

Conversely, a downturn in the manufacturing sector has led to a decline in carload volumes, with total carload traffic down 1.4% YoY in October, totaling 1,128,025 units. Much of this decrease stems from a drop in coal carloads, which fell 8.7% YoY, along with a 5.3% decline in crushed stone volumes. YTD, total carload volumes are down 3.0% compared to the same period in 2023. However, excluding coal, U.S. carload volumes showed a 1.4% YoY increase, indicating relative stability in certain freight commodities despite challenges in manufacturing.

In contrast to volume trends, intermodal rates showed weakness in October, with both contract and spot rates declining over the course of the month. After a $0.14 increase in September, growth in intermodal contract rates slowed, declining by $0.04 MoM to end October at $1.61. As the 2025 bidding season commences, substantial rate changes are not anticipated for the remainder of Q4 until new pricing takes effect. The continued drop in intermodal spot rates reflects ample capacity, as carriers remain competitive in expanding their market share.