Back to November 2024 Industry Update

November 2024 Industry Update: Reefer

Average reefer rates increased modestly in October despite a significant uptick in volumes.

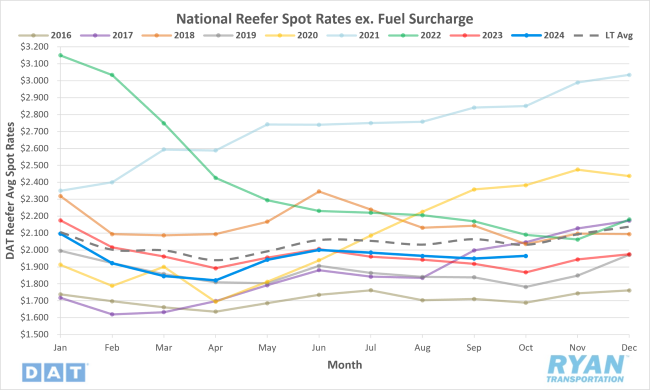

Spot Rates

Key Points

- The national average reefer spot rate, excluding fuel, registered an increase of 0.8% MoM, or roughly $0.02, to $1.97.

- On an annual basis, average reefer spot linehaul rates were up 5.2% YoY but were 3.2% below the LT average.

- The initially reported national average reefer contract linehaul rate rose slightly by 0.2% MoM but was down 2.6% compared to October 2023.

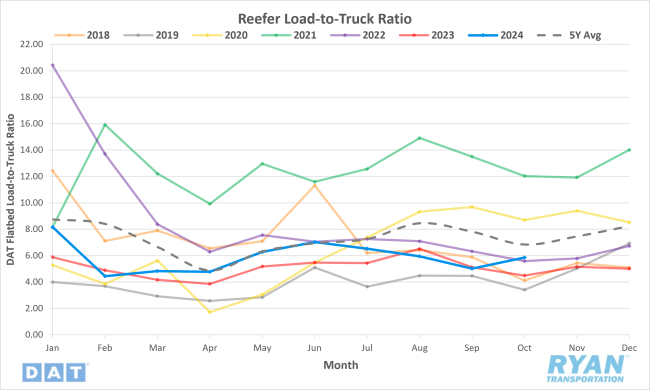

Load-to-Truck Ratio

Key Points

- The reefer LTR in October registered 16.8% higher MoM and was up 30.3% compared to the same month last year.

- Compared to the 5-year average, the reefer LTR was down 3.7%.

Market Conditions

Reefer Summary

As domestic growing seasons wind down, imports of produce from South and Central America will fill the gap. Chile and Peru are significant exporters, with Peru expected to flood the market with blueberries. Los Angeles and Philadelphia are major entry points for these imports, with high volumes of reefer volume heading to destinations in Illinois, North Carolina and Boston. The Philadelphia market has seen an 8% YoY increase in reefer loads, although outbound reefer rates have dropped by 6%.

Potato shipments are expected to start dominating the weekly truckload volumes in the produce sector. Idaho, Washington and Wisconsin lead production, with Colorado’s San Luis Valley rounding out the USDA Top 10 list. This region benefits from high altitude and mild summer temperatures, creating ideal growing conditions. Although the acreage has decreased, favorable weather has boosted volume as Colorado’s shipments of potatoes have already doubled compared to the same time last year.

California’s citrus industry is facing a difficult season, with crop size decreasing between 10-to-20% due to thrips (small insects that damage crops). Orange supply gaps are expected until late October or early November, and overall citrus truckload volumes from California are down 18% compared to last year. Oranges account for 52% of California reefer volume and were down 6% YoY, while lemon production was down 35%. California is the leading producer of lemons, supplying more than 90% of the nation’s volume. On the other hand, California also supplies nearly 90% of the nation’s grape volume and has seen a 12% increase in grape shipments at the beginning of October, the highest level in five years.