Back to November 2024 Industry Update

November 2024 Industry Update: Truckload Capacity Outlook

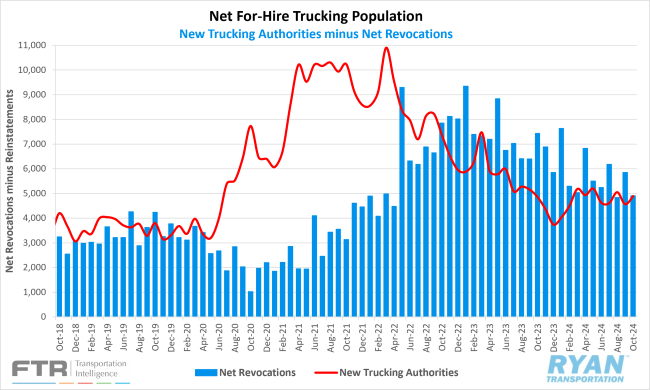

The for-hire carrier population remained virtually unchanged in October as an increase in new entrants nearly offset declines in net revocations.

Key Points

- Total net revocations, a measure of total authority rejections minus reinstatements, declined in October by 943 carriers, dropping from 5,852 revocations in September to 4,909 in October, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- The number of newly authorized for-hire trucking companies rose by 330 carriers, rising from 4,567 new authorities in September to 4,897 in October.

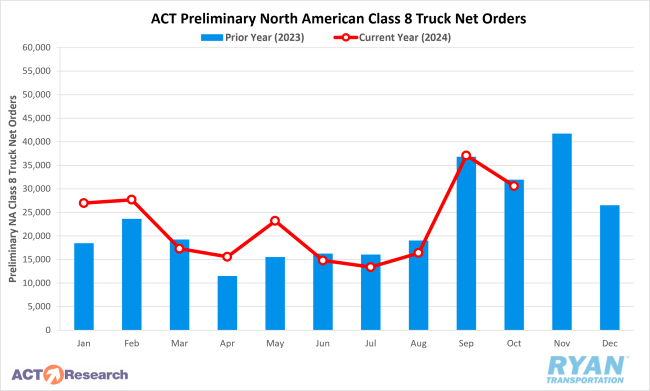

- Preliminary North American Class 8 Orders in October ranged from 28,300 units as reported by FTR to 30,600 units per ACT Research, with annual comparisons mixed as FTR reported a 2% increase YoY while ACT Research noted a 5.2% decline compared to 2023.

Summary

After an accelerated decline in September that followed a modest increase in August, October’s net change in the carrier population was nearly flat. According to FTR’s preliminary analysis of FMCSA data, net revocations surpassed new authorities by only 12 carriers. This minimal net decrease represents the lowest reduction in the carrier population in over two years, despite three instances of moderate increases during that period. October’s subdued capacity change primarily reflects a steep decline in net revocations, which fell by over 940 carriers to 4,908, the second-lowest level YTD after July’s 4,836. New authorities rose MoM for the sixth time in 2023, an unexpectedly brisk pace, given that new entrants only increased on a monthly basis eight times between 2022 and 2023.

On the equipment side, after strong gains in September as OEMs opened their 2025 order books, preliminary North American Class 8 truck orders slowed in October, with monthly declines reported by ACT Research and FTR. According to ACT, October orders were estimated at 30,600 units, a 17.5% MoM decrease from September and a seasonally adjusted decrease of 30%. On an annual basis, orders fell 5.2% compared to October 2023, marking the fifth month in 2024 in which orders were lower YoY. FTR, however, reported a slight YoY gain of 2% for October but noted that order levels missed seasonal expectations. According to FTR, the seven-year October average is 33,940 units, placing last month’s preliminary estimates about 17% below this seasonal benchmark.

Why It Matters:

The ongoing stabilization of the carrier population remains a concern, as indicators of a demand-driven recovery remain weak. The resurgence of new entrants supports the view that recent rate increases and anticipation of rising retail shipping demand have drawn smaller carriers and owner-operators—many idle over the past few years—back into the market. Despite minimal declines in October, there are still nearly 90,000 more active operating authorities than pre-pandemic levels, according to FMCSA data.

The October Logistics Managers’ Index reported a slight expansion in the Transportation Capacity Index, which increased by 0.8% MoM to 50.8%. The report noted that in past freight market cycles, transportation capacity typically contracts before the market rebalances; however, this contraction has not yet appeared in the current cycle. The sub-index has reached the neutral 50% level only twice in the last two years, in July and September, without dipping below into contraction.

While FMCSA data on active for-hire trucking authorities provides a partial view of current capacity, it does not fully capture the degree of market oversupply. BLS data on payroll employment in the for-hire trucking sector reported a minimal loss of 100 jobs MoM in October (seasonally adjusted). September’s initial loss of 700 jobs was revised down to just 100. While previous months showed more fluctuation, the net change in truck transportation employment over the past four months has been a decline of just 700 jobs.

More detailed data on truckload employment, which lags by a month, presents a somewhat contrasting picture. Despite the modest declines in the broader trucking sector, general freight truckload employment increased by 1,600 jobs MoM in September, marking the largest seasonally adjusted gain since May 2023. This increase places general truckload employment at its highest level since April. Although these gains are concerning given the lack of change in for-hire capacity, they are likely to be adjusted downward in February when the BLS releases its annual revisions.