Back to November 2024 Industry Update

November 2024 Industry Update: Truckload Demand

Contract volumes were down slightly in October but in-line with seasonal expectations, while spot market activity surged in the wake of Hurricanes Helene and Milton.

Key Points

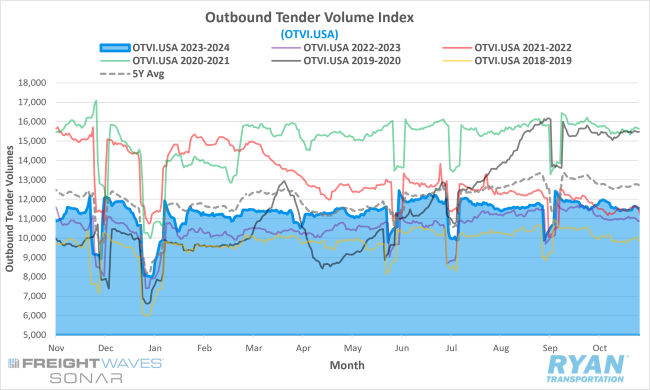

- The FreightWaves SONAR Outbound Tender Volume Index (OTVI.USA), a measure of contracted tender volumes across all modes, registered a 1.5% increase MoM at the end of October compared to 30 days prior, increasing from 11,444.06 to 11,611.75.

- The monthly average of daily tender volumes in October increased by 1% MoM compared to September, rising from 11,512.57 to 11,622.99.

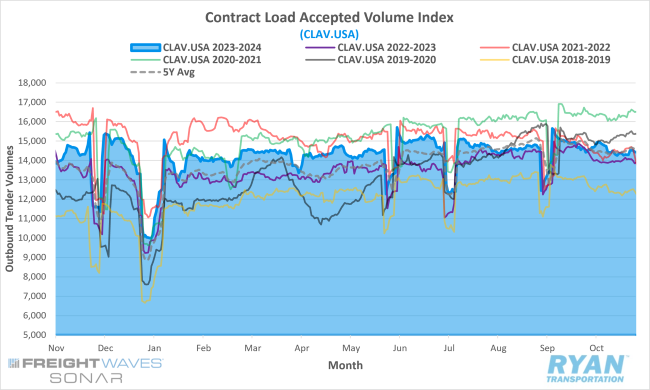

- Compared to October 2023, average daily tender volumes were up 4.9% YoY but registered 8.6% below the 5-year average.

- Spot market volumes registered significant gains in October, rising 26.6% MoM and 19.9% higher on an annual basis.

- The Cass Freight Index Report, which analyzes the number of freight shipments across North America and the total dollar value spent on those shipments, registered a 1.7% decline MoM for shipments while expenditures were up 2.4% in October with both coming in lower compared to 2023 by 5.2% and 6.6%, respectively.

Summary

Freight volumes remained relatively steady in October, although slightly lower than September, consistent with typical seasonal patterns. End-of-month data showed a modest increase of 1.5%, but these figures were influenced by the residual effects of Hurricane Helene and the impending East Coast port strike. Adjusting for these events, mid-month comparisons of FreightWaves SONAR OTVI data revealed a 2.9% MoM decline in October. Additionally, the customary post-Labor Day lull in freight activity inflated the observed 1% MoM increase in the monthly average of daily tender volumes. Excluding data from the first week of September and comparing the 21-day trailing average, October’s OTVI monthly average actually decreased by 2.5%.On an annual basis,

tender volumes recorded by the OTVI were up 4.9% compared to 2023, indicating a gradual demand recovery. The caveat to the annual gains registered by the OTVI is the index’s inclusion of rejection rates, which are higher than they were this time last year. For a clearer view, the FreightWaves SONAR Contract Load Accepted Volume Index (CLAV.USA), which excludes rejections, showed a more modest 3.5% increase YoY. However, the monthly average of tenders accepted under contract registered a steeper MoM decline of 3.2% (21-day trailing average) from September to October.

While contracted volumes weakened in October, the spot market captured increased activity, primarily due to hurricane impacts. According to DAT, spot volumes surged in the first week of October as supply chains adjusted in response to Hurricane Helene, with load postings up 14.9% WoW. However, as Hurricane Milton made landfall, spot market activity dipped by 14%, nearly erasing the gains from the prior week. Relief and recovery efforts for both hurricanes subsequently drove a 16% WoW increase in spot market volumes, though volumes declined by a cumulative 14% over the final two weeks of the month.

Why It Matters:

While the weakening demand observed in October aligns with seasonal expectations, the stability in volumes seen through much of the year appears to be softening. Following a Labor Day peak, volumes have trended downward over the past two months. Freight demand remains elevated compared to last year, suggesting that the market has likely reached its floor. However, the momentum that previously sustained volume resilience is showing signs of stalling. This sentiment has been echoed across earnings calls from major publicly traded trucking companies, with CEOs noting fewer shipments from customers and expressing limited optimism for a sharp recovery given the softer demand environment.

As noted in prior updates, any significant rebound in truckload demand depends on a substantial increase in U.S. manufacturing output. Although some analysts anticipate modest growth in domestic manufacturing as early as Q1 2025, YoY expectations are incremental, falling short of a strong inflection point. Meanwhile, analysts have continued to point to the strength of imports throughout 2024 as a potential catalyst for freight volume recovery. Containerized imports have increased approximately 14% YoY on average through the first nine months of the year, with July and September surpassing volumes from the same months in 2021 – a record year for imports. However, this growth has yet to translate into a notable rise in overall freight demand. Additionally, Michigan State Supply Chain Professor Jason Miller notes that paper manufacturing, the fourth-largest contributor to U.S. truckload volumes, has declined by 10% since Q2 2022. Paper manufacturing alone generates around seven million truckload shipments annually, roughly equal to or exceeding all containerized imports.

According to the October Logistics Managers’ Index (LMI) Report, both inventory levels and costs were both significantly robust in early October before dropping to slower expansion in the back half of the month. This suggests that seasonal inventories likely peaked in mid-October and will most likely continue to come down due to the holiday shipping season. According to the LMI report, this is consistent with what has been observed over the past two years. The report also noted that the only time in recent history this hasn’t occurred was in December 2021, which, in hindsight, was the precursor to the inventory bullwhip that staggered retailers in 2022 and was essentially the genesis of the current freight recession.

Despite the near-term outlook for freight volumes remaining muted, there is still potential for seasonal fluctuations around the upcoming holiday period. However, overall truckload demand is still trending in-line with levels observed in 2019, while truck capacity remains higher than in 2019. Consequently, any seasonal upticks in spot market demand are likely to be modest, consistent with trends from the past two years.