Back to November 2024 Industry Update

November 2024 Industry Update: Truckload Supply

Impacts from the hurricanes and the East Coast port strike pushed rejection rates to their highest levels this year outside of the Fourth of July holiday.

Key Points

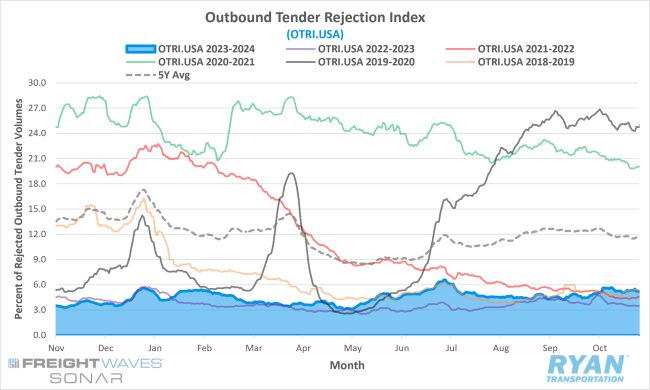

- The FreightWaves SONAR Outbound Tender Rejection Index (OTRI.USA), a measure of relative capacity based on a carriers’ willingness to accept freight volumes under contract reflected as a percentage, registered 65 basis points (bps) higher MoM at the end of October compared to the end of September.

- The monthly average of daily tender rejections in October was 71 bps higher MoM, rising from 4.55 in September to 5.26 in October.

- On an annual basis, average daily tender rejections were up 1.4% YoY compared to October 2023 and were 6.74% below the 5-year average.

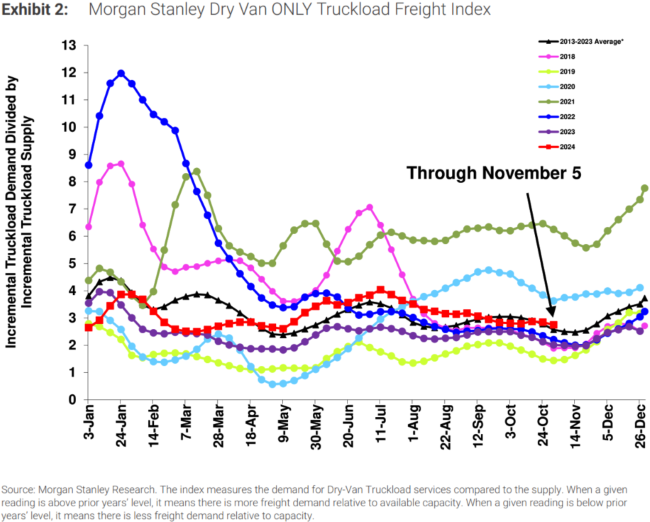

- The Morgan Stanley Truckload Freight Index (MSTLFI) registered sequential increases in the first half of October before turning negative in the second half, and outperformed seasonality during the month driven primarily by strong demand, pushing the index back above the LT average after dropping below in September.

Summary

Tender rejections gained momentum in October, driven by the impact of back-to-back hurricanes and the onset of the East Coast port strike. Following the disruption caused by Hurricane Helene and the three-day strike by ILA union workers, rejection rates increased by 53 basis points WoW in the first week of October, surpassing 5% for the first time since mid-July. Rejection rates continued to rise in the second week, adding another 61 basis points as Hurricane Milton made landfall. As Hurricane Milton’s effects proved less severe than anticipated, supply chains were able to quickly recover by the start of the third week, leading to a reversal of the previous week’s increase in the OTRI. Rejection rates moderated in the final week and a half of October, ultimately declining by 13 basis points WoW to close the month at 5.22%, still 67 basis points higher than at the beginning of the month.

YoY comparisons widened significantly in October, moving from 0.5% higher in September – tied for the third-lowest YTD – to 1.4% higher, the third-highest YTD. Although annual comparisons remain volatile, current rejection rates closely mirror the OTRI trend recorded in 2019, with October’s average daily tender rejection rate registering only 18 basis points above October 2019 levels. The alignment of current rejection rates with 2019 is noteworthy, as that year saw the tender rejection index surge in the final six weeks, rising over 2% MoM after Thanksgiving to just above 7%, ultimately peaking at over 14% on Christmas Day.

The Morgan Stanley Truckload Freight Index outperformed expectations in October, largely due to robust demand overshadowing a slight underperformance in supply. According to October’s report, the demand component of the index increased by a total of 11.5% during the month, contrasting with the typical seasonal decline of 0.5%. Meanwhile, the supply component rose by 13.5%, exceeding its seasonal average increase of 8.2%. The report suggests that hurricane impacts may have contributed to the index’s strong performance in October, but it notes that the continued rise and underperformance in supply complicate that assessment. Forward-looking sentiment appeared more neutral compared to the bearish outlook in September, with respondents noting early signs of market stabilization, though continued carrier attrition remains necessary.

Why It Matters:

The uptick in tender rejections in October created a sense of “normalcy" within the market. However, their sustainability at current levels is uncertain due to recent disruptions. The impact of the hurricanes and port strike drove rejections to their highest levels this year outside of the Fourth of July holiday.

Although these disruptions raised national rejection rates above average, the sharp decline after they subsided suggests the market remains oversupplied.

Despite supply continuing to outpace demand, October’s increase in rejection rates could influence the market in several ways in the months ahead. The rise in the OTRI throughout October effectively set a new baseline heading into the peak holiday shipping season. While the port strike and hurricanes caused regional capacity shortages, holiday disruptions tend to create shortages on a national scale. With tender rejections currently above 5%, any expected tightening in capacity during the holidays could exert greater upward pressure on rates than anticipated. As noted in prior updates, tender rejections in the 5-7% range can disrupt major carrier networks, while rejection rates that trend above 7% or experience a rapid increase in a short amount of time typically lead to higher spot rates.

While tender rejections have aligned with 2019 levels in the latter half of this year, a significant surge like that of November and December 2019 is unlikely to be repeated this year. The sharp rise in 2019 was driven by remarkably strong, unseasonable production by food manufacturers – the largest source of annual freight for truckload carriers. Given current weak conditions in both manufacturing overall and food production specifically, it is improbable that we will see a repeat of those conditions this year.