Back to October 2024 Industry Update

October 2024 Industry Update: Economy

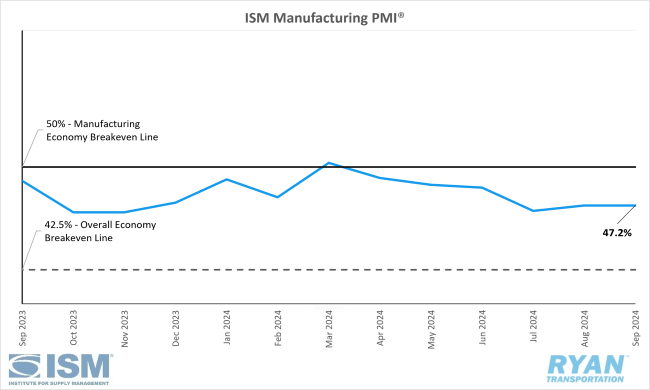

Domestic manufacturing remained in contraction in September as ongoing uncertainty surrounding the elections and federal monetary policy continues to deter further investments in capital and inventories.

Key Points

- The ISM Manufacturing PMI® registered 47.2% in September and was unchanged from the August reading.

- The New Orders Index remained in contraction in September, registering 46.1% and 1.5% above August’s reading of 44.5%.

- The Production Index registered 49.8% in September, 5.0% higher than the 44.8% recorded in August.

- The Employment Index contracted further in September, dropping 2.1% from August’s reading of 46.0% to 43.9%.

- The Prices Index moved into contraction territory in September, registering 48.3% and 5.7% below August’s reading of 54.0%.

Summary

U.S. manufacturing activity contracted for the sixth consecutive month in September, maintaining the same rate of decline as August, according to the latest ISM Manufacturing PMI® report. With September's reading remaining below 50%, the composite index has now been in contraction for 22 of the last 23 months. Demand continued to be weak, output declined and inputs remained accommodative.

While the demand component remained subdued, it showed slight improvement compared to August, with new orders contracting at a slower pace. The Backlog of Orders Index increased marginally to 44.1%, up from 43.6% in August, though it remained firmly in contraction. Meanwhile, customers' inventories rose by 1.6%, moving from 48.4% in August to 50.0% in September, indicating inventory levels were considered "about right." Survey respondents indicated that the amount of their product in customers’ inventories pointed to a neutral to negative outlook for future new orders and production.

The output components of the composite index, primarily the Production and Employment indices, remained in contraction but presented mixed results. The Production Index, after reaching its lowest level since May 2020, increased by 5% in September reaching 49.8%, which is near expansion territory. Despite weak new orders and declining backlogs, companies managed to maintain output levels. However, employment contracted at a faster pace, with companies continuing to reduce headcounts in line with projected demand. This sentiment was reflected in the PMI® report, where panelists noted a 1-to-1.5 ratio of hiring to staff reductions.

Among the six largest manufacturing industries—Machinery; Transportation Equipment; Fabricated Metal Products; Food, Beverage & Tobacco Products; Chemical Products; and Computer & Electronic Products—only the Food, Beverage & Tobacco Products industry reported growth in September, down from two industries reporting growth in August.

Why it Matters:

The continued contraction of domestic manufacturing activity in September came as no surprise, with stability reflected in the unchanged Manufacturing PMI® from August. Uncertainty surrounding the upcoming November elections and federal monetary policy continues to discourage companies from making capital investments and increasing inventories. While the Federal Reserve has addressed elevated borrowing costs with a 50-basis-point rate cut in September, this is unlikely to have a significant impact on the manufacturing sector until early 2025, according to Timothy Fiore, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Despite the overall weak report, there were some positive indicators suggesting that the underlying dynamics may be shifting in the right direction. Notably, production increased and prices decreased. Production, which had shown resilience throughout the contraction period, rebounded in September following a significant drop in August. Additionally, the Prices Index moved back into contraction territory, recording a 48.3% reading as key commodities, including aluminum and steel, experienced reduced volatility. Fiore noted that the stability in September’s report reflects companies aligning headcounts and inventory levels with expected revenue, as evidenced by contractions in both employment and inventory.

However, the September report comes with caveats, as it was compiled before two significant events: port strikes on the East and Gulf Coasts and the impact of Hurricane Helene on the Southeast. These developments, along with the ongoing Boeing union strike, which will heavily affect the Transportation Equipment sector, pose serious threats to the modest progress indicated in September. Rising geopolitical tensions in the Middle East further add to the uncertainty. These factors are expected to negatively affect the already weak outlook for October, and the ongoing challenges in domestic manufacturing will likely delay any recovery in truckload demand.

Macro Economy

- Non-farm payroll employment rose by 254,000 jobs MoM in September on a seasonally adjusted basis following upward revisions to both July and August estimates, according to the most recent jobs report released by the Bureau of Labor Statistics (BLS).

- The unemployment rate fell by 0.1% MoM to 4.1% in September, marking the second consecutive decline following five months of increases.

- Transportation and Warehousing declined by 8,600 jobs in September on a seasonally adjusted basis.

- Truck Transportation declined slightly, shedding 700 jobs in September on a seasonally adjusted basis.

- Warehousing and Storage employment declined by 11,000 jobs in September on a seasonally adjusted basis.

- Both the headline and core Personal Consumption Expenditures (PCE) indices rose by 0.1% MoM in August on a seasonally adjusted basis, according to the most recent report released by the Bureau of Economic Analysis (BEA).

- On an annual basis, the all-items PCE index rose by 2.2% in August on a seasonally adjusted basis and was 0.3% lower than July’s reading of 2.5%.

- Excluding food and energy, the PCE Index rose by a seasonally adjusted 2.7% YoY in August, 0.1% higher than the 2.6% increase registered in July.