Back to October 2024 Industry Update

October 2024 Industry Update: Flatbed

The flatbed sector performed the best of the three major mode types, as volumes surged and average spot rates increased slightly in September.

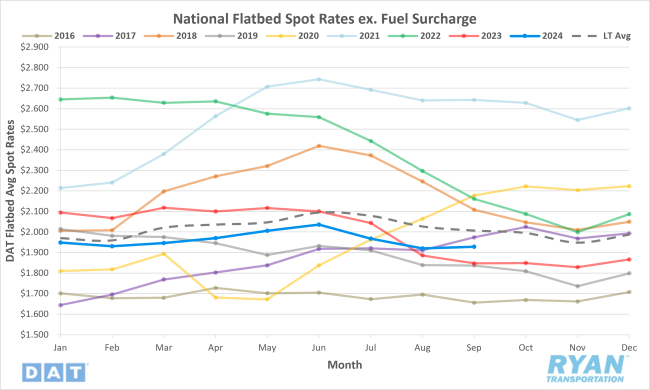

Spot Rates

Key Points

- The national average flatbed spot rate excluding fuel registered a slight increase in September, rising by 0.4% MoM, or just under $0.01, to $1.93.

- The average flatbed spot linehaul rate remained elevated on an annual basis in September, registering 4.4% higher YoY, but remains 3.9% below the LT average.

- The initially reported national average flatbed contract rate exclusive of fuel declined 1.3% MoM in September but was 1.6% higher compared to September 2023.

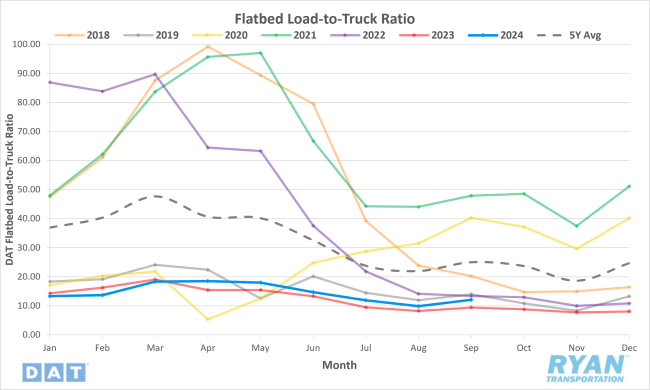

Load-to-Truck Ratio

Key Points

- The flatbed LTR rose by 22.9% MoM in September and was 28.2% higher compared to the previous year’s levels.

- The flatbed LTR remained well below the 5-year average in September at 51.6%.

Market Conditions

Flatbed Summary

U.S. residential housing construction for single-family homes fell to a four-year low, starting at a rate of 851,000 units, which was 14.1% lower than June's revised figures and 14.8% below July 2023 levels. The drop highlights a continued softening of the housing market, driven by higher mortgage rates and rising prices, which have dampened sales. Flatbed carriers looking for recovery signals in the truckload market should note that building permits, a key forward-looking indicator, were also down 4.0% from June, reflecting muted demand in the coming months. As the Federal Reserve considers interest rate cuts, expected market improvements could boost demand in this sector.

Flatbed spot rates remained strong and averaged around $2.00 per mile, slightly higher than in the previous months. In regions affected by Hurricane Helene, such as Florida and the Southeast, spot rates saw even steeper increases, particularly as outbound volumes plummeted and inbound freight surged. For example, inbound volumes into Alabama, Mississippi and Georgia rose 44%, pushing rates up by 7% week-over-week to $2.45 per mile. These trends suggest that while hurricanes negatively impacted outbound volumes, the recovery efforts boosted inbound freight demand, benefiting flatbed carriers.

On the broader economic front, construction spending, a major driver for flatbed demand, remained elevated. With that said inflation and higher costs for high-tech manufacturing projects such as electric vehicle production and semiconductor plants tempered growth. Housing starts, another critical flatbed demand indicator, rebounded, with single-family homebuilding jumping by 16% in August as interest rates slightly eased. This resurgence in construction, particularly in housing and infrastructure, is expected to support demand for flatbed carriers in the months ahead, even as other factors, like natural disasters, create short-term disruptions.

Meanwhile, agricultural equipment markets saw mixed results, with a 4.8% rise in U.S. 4-wheel-drive tractor sales in August. However, overall agricultural tractor and combine sales dropped nearly 20%, reflecting broader market difficulties and a need for policy support for rural economies.