Back to October 2024 Industry Update

October 2024 Industry Update: Fuel

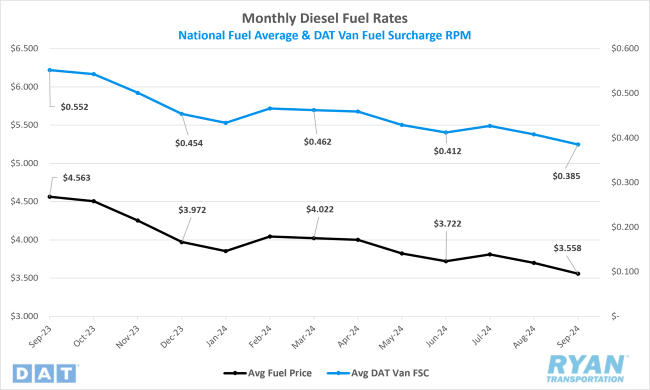

Weak global demand and limited impact from macroeconomic events dropped average diesel prices to their lowest level in two years.

Key Points

- The national average price of diesel declined further in September, dropping 3.8% MoM, or just over $0.14, to $3.56.

- Compared to September 2023, diesel prices were 22%, or just over $1.00, lower in September.

- Draws on U.S. Commercial Crude inventories outpaced builds by 1.4M bbls and slightly underperformed the consensus of 1.5M bbls for the weeks ending September 6 and September 27.

Summary

Average fuel prices continued to decline in September for the second consecutive month, following a brief uptick in July that interrupted the previous four-month downward trend. The national average fuel price for September reached its lowest level since September 2021, when it stood at $3.38, and is now over $1.00 lower than in the same month last year. On a weekly basis, diesel prices saw consecutive declines during the first three weeks of September, part of a 10-week period of WoW price reductions totaling $0.34. However, this trend concluded in the final full week of the month, with the Department of Energy (DOE) and Energy Information Administration (EIA) reporting a marginal WoW increase of just over $0.01.

At the same time, withdrawals from U.S. commercial crude oil inventories have slowed in recent months, as refining margins have sharply decreased over the past two months. Refining margins, which compare the per-barrel futures price of Brent crude to the per-gallon price of ultra-low sulfur diesel (ULSD), fell by over $0.20 since July, dropping from $0.57 to $0.36 in September. This narrowing spread reflects the fact that diesel prices have declined more rapidly than crude, indicating specific market weakness in diesel rather than a general decline in crude prices. Despite this, overall crude inventories remain near record lows. Following a larger-than-expected drawdown in the week ending September 20, crude oil inventories dropped to their lowest levels since April 2022.

Why It Matters:

Global demand growth remained sluggish in September, particularly in China, exerting further downward pressure on oil prices. OPEC+ initially planned to ease production cuts in October, but these plans have been postponed and are now set to take effect in December. Despite this delay, many analysts remain bearish, forecasting continued price declines. This outlook was reinforced by an RBC Capital report, which noted that crude inventory drawdowns in Q3 2024 were 70% lower compared to Q3 2023, signaling weak demand and reflecting the impact of a slowing global economy.

Recent news events that would typically drive oil prices higher have failed to produce sustained bullish momentum. Rising tensions in the Middle East, particularly between Israel and Iranian-backed groups such as Hezbollah in Lebanon, have not yet posed a significant threat to oil output in the region. This is likely to remain the case unless Israel directly targets Iranian oil facilities. Additionally, Hurricane Helene temporarily disrupted production along the Gulf Coast and Southeast U.S., but data from the Bureau of Ocean Energy Management indicates that only 59,000 barrels per day remained offline as of the Sunday following the storm. This suggests minimal damage to offshore platforms and no long-term supply disruptions. While diesel demand may rise in the short term due to relief efforts in the affected areas, this increase is expected to be offset by a temporary slowdown in broader consumption as normal activities are impacted.

Back to October 2024 Industry Update