Back to October 2024 Industry Update

October 2024 Industry Update: Truckload Capacity Outlook

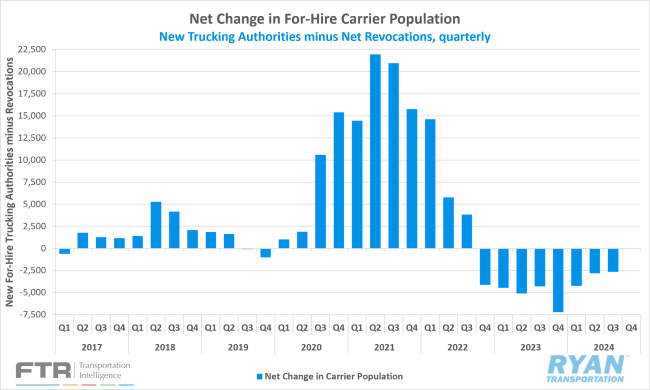

Declines in the carrier population slowed in Q3, suggesting for-hire capacity levels may be stabilizing.

Key Points

- Total net revocations, a measure of total authority rejections minus reinstatements, rose in September by 1,016 carriers, increasing from 4,836 revocations in August to 5,852 in September, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- The number of newly authorized for-hire trucking companies declined by 488 carriers, dropping from 5,055 new authorities in August to 4,567 in September.

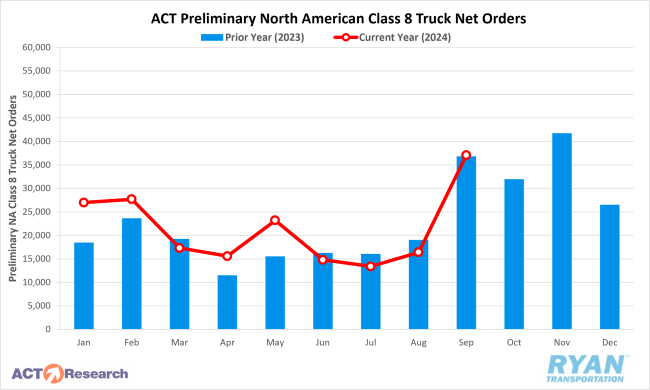

- Preliminary North American Class 8 Orders in September ranged from 30,000 units as reported by FTR to 37,100 units per ACT Research, with both estimates registering higher YoY by 4% and 0.3%, respectively.

Summary

Following a modest increase in August, the decline in the carrier population accelerated in September with a net reduction of 1,285 carriers—the fourth largest MoM decrease recorded this year. However, on a quarterly basis, the decline in Q3 was less pronounced, totaling 2,636 carriers and marking the smallest quarterly decrease since the onset of the current market downturn. This slowing of declines from a quarterly perspective suggests capacity levels are stabilizing.

The September decline in carrier numbers was primarily driven by a sharp rise in net revocations and a significant decrease in new carrier authorizations. According to FTR’s preliminary analysis, the 4,567 new carrier authorizations recorded in September represent the lowest figure since February. Concurrently, net revocations registered the fourth highest total this year, trailing the peaks observed in July, April and January. FTR notes that these three months each had five Mondays, the day when the FMCSA processes the majority of revocations. Excluding these anomalies, September saw the highest level of net revocations since December 2023, which coincidentally recorded the same total.

On the equipment side, preliminary North American Class 8 truck orders surged in September, coinciding with OEMs opening their 2025 order books. Preliminary estimates from both ACT Research and FTR show orders more than doubling compared to August at 0.3% and 3.2% respectively, though growth varied slightly by source.

According to ACT Research, while September typically marks the beginning of stronger order volumes due to OEMs opening their books for the following year, last month's orders exceeded both trend and seasonal expectations. ACT reported that, after adjusting for seasonality, order levels were up 92% compared to August 2023. FTR shared a similar outlook but noted that orders aligned with seasonal norms, with the 7-year average for September standing at approximately 32,170 units. FTR also highlighted the potential for downward pressure on build rates through the remainder of 2024, given the near-record inventory levels.

Why It Matters:

The return of net revocations outpacing new authorities, following the slight increase in August, is a positive indicator for the market as it continues to navigate the supply-led industry recession. However, a less favorable sign is the slowdown in the decline of the carrier population on a quarterly basis, as capacity stabilizes. According to FMCSA data, there are still approximately 90,000 more operating authorities than before the pandemic following September’s decline.

The September Logistics Managers’ Index Report highlighted a significant decrease in transportation capacity in September compared to August, bringing the subindex back to neutral territory. This suggests the market is beginning to tighten in a seasonally appropriate manner. The report also indicates that future projections for the next 12 months continue to predict further capacity contractions.

While FMCSA-reported changes in active for-hire trucking authorities provide some insight into current capacity levels, they do not fully reflect the extent of the oversupply in the market. According to BLS data, payroll employment in the for-hire trucking sector registered a modest decline of 700 jobs in September on a seasonally adjusted basis. This follows revised BLS estimates for July and August, which added a net of 800 jobs. Despite the slight reduction, payroll employment in truck transportation remained 2% higher in September compared to February 2020.

More detailed data, which lags by a month, shows that general freight truckload payroll employment eased by 400 jobs in August, marking the lowest level since September 2022. Nevertheless, employment in the general freight truckload sector was still 4.1% higher in August 2024 compared to February 2020. Given the current weak demand backdrop and bleak near-term outlook, the market conditions have little chance of improving in the coming months at the current pace of capacity contraction.