Back to October 2024 Industry Update

October 2024 Industry Update: Truckload Demand

Demand levels were stable in September following the Labor Day holiday but provided little insight into when traditional pre-holiday peak shipping season would begin ramping up.

Key Points

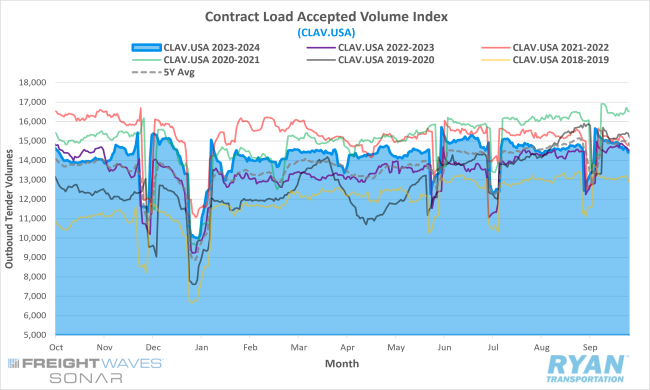

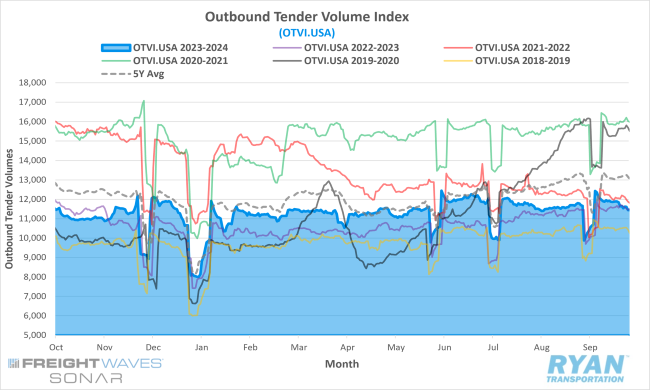

- The FreightWaves SONAR Outbound Tender Volume Index (OTVI.USA), a measure of contracted tender volumes across all modes, fell 2.1% MoM at the end of September compared to the end of August, dropping from 11,690.80 to 11,444.06.

- The monthly average of daily tender volumes in September fell slightly by 0.6% MoM compared to August, decreasing from 11,512.57 to 11,582.55.

- Compared to September 2023, average daily tender volumes were up 2.9% YoY but were 9.8% below the 5-year average.

- Spot market volumes declined further in September, dropping 1.8% MoM, and registered 13.1% lower compared to September 2023.

- The Cass Freight Index Report, which analyzes the number of freight shipments in North America and the total dollar value spent on those shipments, increased on a monthly basis by 1.0% for shipments while expenditures fell 2.0% in September. Both shipments and expenditures were lower by 1.9% and 9.0% YoY, respectively.

Summary

Freight volumes, as reported by the FreightWaves Outbound Tender Volume Index (OTVI), remained relatively stable throughout September, as they have throughout much of the year thus far. After freight demand failed to gain momentum leading into Labor Day weekend, volumes dropped by more than 10% during the first week—a typical decline following a holiday. However, the post-Labor Day dip was brief, as volumes rebounded by over 13% in the second week and remained elevated through the third. That momentum stalled during the final week, with tender volumes falling by approximately 4%, closing out both the month and the third quarter.

Among the key transportation modes tracked by the OTVI, the dry van segment posted the strongest performance in September, with volumes increasing by just over 4%. Refrigerated volumes, however, remained flat MoM. Although not reflected in the OTVI, flatbed volumes have shown signs of improvement in recent months, likely driven by a resurgence in industrial activity following recent Federal Reserve interest rate cuts. In August, housing starts rose by 16% MoM, while building permits—a leading indicator of demand—saw a more moderate 3% MoM increase. This industrial uptick was also evident in the 1.0% MoM increase in shipments recorded by the Cass Freight Index Report for August, which is heavily influenced by industrial sectors.

Despite this relative stability, freight volumes in September continued to flow primarily through the contract market, as spot market activity registered declines. According to DAT, spot market volumes jumped 11.5% WoW leading up to Labor Day, but then steadily decreased through the first two weeks of September. However, spot activity recovered in the last two weeks of the month ahead of Hurricane Helene and anticipated port strikes, with volumes rising by just over 10% and 13% WoW, respectively, by month-end.

Why It Matters:

While demand remained stable in September, there is still uncertainty surrounding the potential impact of the traditional peak season this year. The pre-holiday shipping surge has been virtually absent over the past two years, raising questions about whether it will return in 2024. The latest Logistics Managers’ Index report suggests that the expansion of inventory levels and increases in warehousing costs may signal that retail supply chains are preparing for peak season.

However, despite strong consumer spending driving freight volumes throughout much of 2024, concerns about its sustainability in the coming months persist. Some analysts highlight the absence of typical pre-Labor Day and end-of-quarter volume surges as an indication that consumer resilience may be weakening, potentially leading to another subdued peak season.

While the outlook for retail shipping remains uncertain, signs of recovery in industrial activity offer a positive outlook for the flatbed sector, which has underperformed over the past two years. A significant contributor to industrial freight volumes is the ongoing recovery from major weather events, such as Hurricane Helene.

In contrast to Hurricane Francine, which had minimal impact, Helene caused widespread devastation across several southeastern states. The Category 4 storm resulted in significant damage to homes and infrastructure, particularly in Florida, Tennessee and North Carolina, where a section of I-40 collapsed near the state border. The hurricane also tragically claimed 227 lives and caused billions of dollars in damage, with costs still being assessed. With additional hurricanes projected to make landfall in October, flatbed carriers are expected to benefit significantly as construction equipment and materials are transported to support rebuilding efforts.