Back to October 2024 Industry Update

October 2024 Industry Update: Truckload Supply

Excess truckload supply continues to put negative pressure on market conditions, as tender rejections remained below the 5% threshold.

Key Points

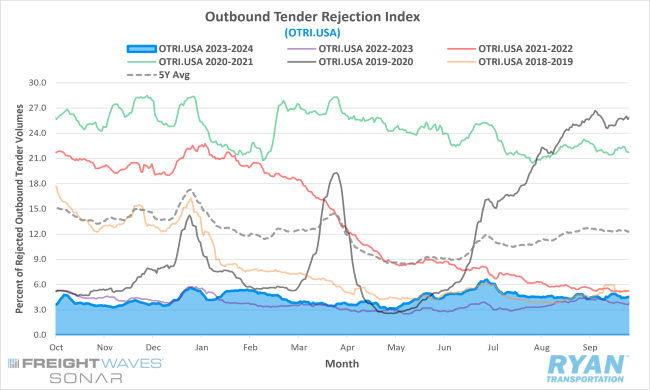

- The FreightWaves SONAR Outbound Tender Rejection Index (OTRI.USA), a measure of relative capacity based on a carriers’ willingness to accept freight volumes under contract reflected as a percentage, registered a 0.3% decrease MoM at the end of September compared to the end of August.

- The monthly average of daily tender rejections in September was virtually flat MoM compared to August, rising 0.01% from 4.54% to 4.55%.

- On an annual basis, average daily tender rejections were up 0.5% YoY compared to September 2023 and were 7.9% below the 5-year average.

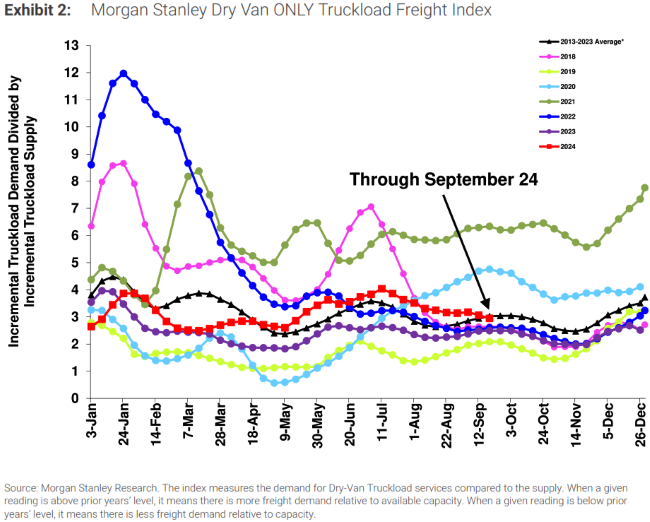

- The Morgan Stanley Truckload Freight Index (MSTLFI) registered sequential declines and continued to underperform seasonality in September, driven by a combination of weak demand and oversupply, pulling the index below the LT average for the first time since mid-April.

Summary

Tender rejections remained subdued throughout September, indicating that the market continues to have ample capacity to shed. After rising by 43 bps to reach a peak of 4.86% in the week leading up to Labor Day, rejection rates lost momentum post-holiday. They declined steadily during the first two weeks of September, falling by 61 bps to 4.25%. Towards the latter half of the month, tender rejections showed a slight recovery, increasing 0.65% week-over-week to 4.9%, before moderating back down to 4.5% at month-end, marking a decline of 31 bps from the beginning of the month. When adjusting for mid-month comparisons to account for holiday-related disruptions, tender rejections fell 0.15% MoM relative to August. From a quarterly perspective, average rejection rates in Q3 registered 4.76%, the highest they’ve been since Q3 2022.

On a YoY basis, tender rejection rates remained slightly above September 2023 levels but continued to align closely with trends observed in 2019, albeit marginally lower. Although YoY comparisons have remained positive, the differential narrowed for the second consecutive month, dropping from 2% above in July to just 0.5% above in September. In comparison to 2019 levels, tender rejections, which had been trending higher for the past two months, turned negative again, decreasing from 45 bps above in August to 61 bps below in September.

The latest Morgan Stanley report attributed this underperformance relative to typical seasonality to a sequential decline in demand and a corresponding increase in supply. According to the report, demand decreased by 170 bps compared to a 500 bps increase in the prior month. Meanwhile, supply increased by 640 bps, significantly above the typical monthly increase of 130 bps. Forward-looking sentiment has turned more bearish, with respondents noting slower capacity exits and weakening demand levels. While the index fell below the long-term average for the first time since mid-April, current levels remain higher than those recorded in the previous year, suggesting that ongoing supply contractions are gradually moving the market toward equilibrium.

Why It Matters:

Tender rejections' inability to surpass the 5% threshold in September, despite several capacity-disrupting events, underscores the ongoing imbalance between supply and demand in the truckload market. While recent capacity exits suggested the market might be shifting toward equilibrium, September's data indicates that the extent of supply contraction may have been overestimated. Outside of a few regional pockets experiencing capacity shortages, the majority of the country continues to see an oversupply of truckload capacity.

This imbalance is further highlighted by the decline in the Outbound Tender Rejection Index (OTRI) at the end of the month, coinciding with both the close of the quarter and a major hurricane—two events that would typically exert upward pressure on rejection rates.

Some analysts attribute the stagnant tender rejection rates to the lack of seasonal freight volume increases, which are usually observed at this time of year. Regardless, the situation emphasizes the extent of oversupply within the market amid a soft demand environment. With no immediate, sustainable demand drivers on the horizon, the path to restoring market equilibrium continues to come down to a further significant reduction in the for-hire capacity space.