Back to September 2024 Industry Update

September 2024 Industry Update: Economy

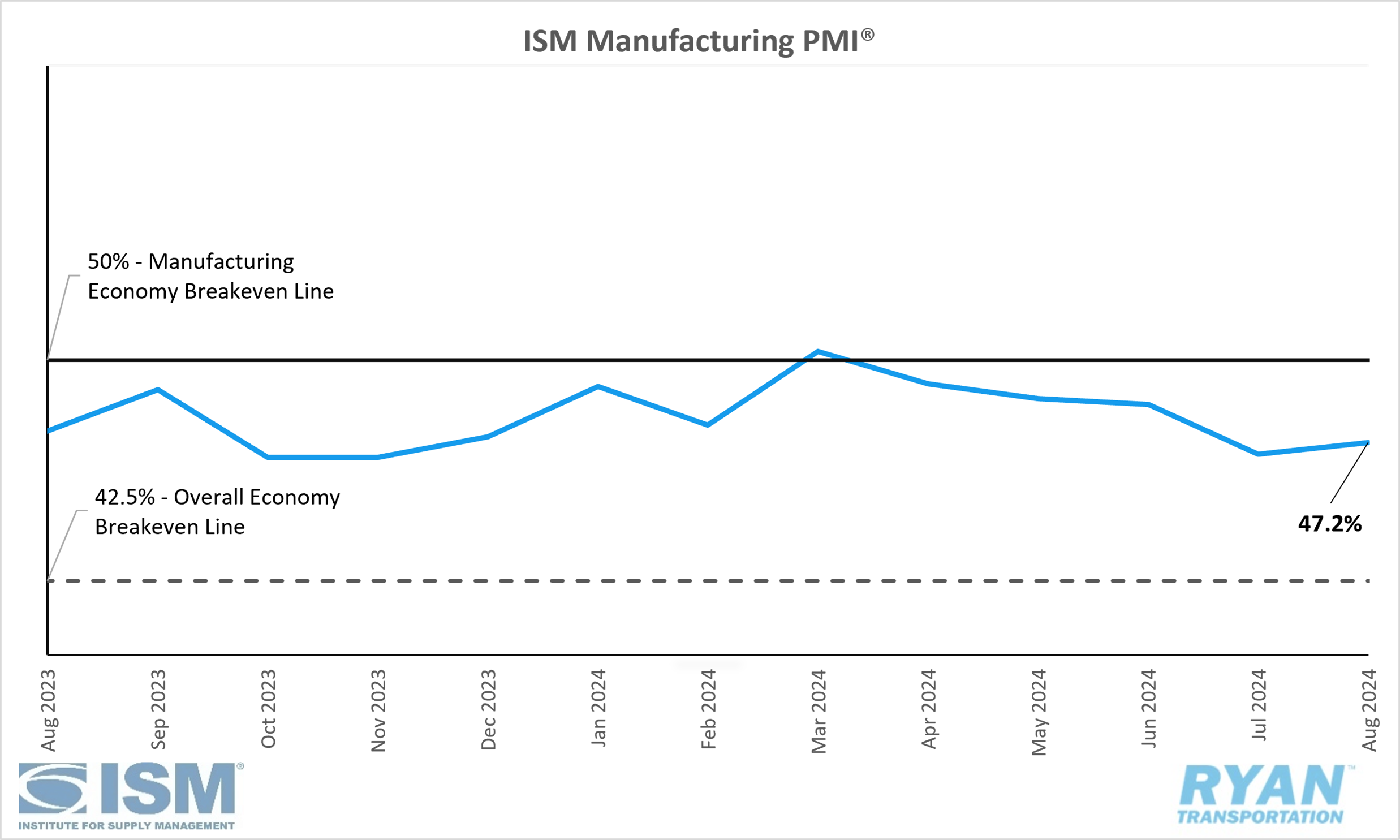

Manufacturing activity in the U.S. contracted in August but at a slower pace compared to July, as weakening demand and increasing inventories stifled production.

United States ISM Manufacturing PMI

Key Points

- The ISM Manufacturing PMI® registered 47.2% in August, a 0.4% increase from the 46.8% recorded in July.

- The New Orders Index contracted further, dropping 2.8% from July’s reading of 47.4% to 44.6% in August.

- The Production Index remained in contraction in August, registering 44.8% and 1.1% lower than the 45.9% recorded in July.

- The Employment Index registered 46.0% in August, 2.6% higher than July’s reading of 43.4%.

- The Customers’ Inventories Index moved to the low end of “just right” territory in August, increasing 2.6% to 48.4%compared to 45.8% in July.

Summary

U.S. manufacturing activity contracted for the fifth consecutive month in August, although at a slower pace than in July, according to the latest ISM Manufacturing PMI® report. With the August reading remaining below 50%, the composite index has now been in contraction for 21 of the last 22 months. The continued weakening in demand exerted downward pressure on outputs while input conditions remained accommodative.

The further slowdown in the demand components of the Manufacturing PMI® was primarily reflected in the decline of the New Orders Index. The ISM® report highlighted the ongoing uncertainty surrounding new order activity, with panelists' responses indicating a 1-to-1.6 ratio of positive sentiment to concern. Other notable indicators of the soft demand environment included the Backlog of Orders remaining in contraction—albeit at a slower rate than in July—and the Customers’ Inventories Index shifting from "too low" back to a "just right" level.

Output components, as measured by the Production and Employment indices, continued to show a moderation in contraction in August, with production declining further while employment contracted at a slower rate compared to July. According to the ISM® report, output levels continued to fall as demand remained weak and backlog levels diminished, bringing the Production Index to its lowest point since May 2020. On the employment front, companies continued to reduce their workforce through layoffs, attrition and hiring freezes. Panelists' responses reflected continued staff reductions, with an approximate 1-to-1.2 ratio of hiring to headcount reductions in August.

Of the six largest manufacturing industries—Machinery; Transportation Equipment; Fabricated Metal Products; Food, Beverage & Tobacco Products; Chemical Products; and Computer & Electronic Products—only two (Food, Beverage & Tobacco Products and Computer & Electronic Products) recorded growth in August, compared to none in July.

Why it Matters

The ongoing contraction in the U.S. manufacturing sector is concerning, not only for the health and outlook of the overall economy, but also for the much-needed recovery in the transportation industry. While the latest report from the ISM® offered limited positive news, it did show a slight improvement over the more concerning figures from July. However, the August report continues to reflect many of the same challenges highlighted in previous updates, primarily involving federal monetary policy restricting capital and inventory investments as well as uncertainty surrounding the upcoming election.

The recent period of contraction, with the PMI® registering below 50% in 21 of the last 22 months, is historically significant. Similar periods have occurred in the past: once when the PMI® contracted for 18 consecutive months between August 2000 and January 2002 following the dot-com bubble burst, and again for 16 out of 18 months between February 2008 and July 2009 during the Great Recession. Compared to those two periods, however, the current cycle has been less severe. Although a manufacturing PMI® in the high 40% range is not ideal, it indicates that there has not been a significant deterioration in manufacturing activity.

According to Timothy Fiore, Chair of the Institute for Supply Management® Manufacturing Business Survey Committee, the August report focused primarily on output, as the Production Index fell to 44.8%, the lowest reading in the current contraction cycle. This decline has created a cascading effect on employment. Despite a slight increase in the Employment Index, workforce reductions have reached their highest level since the ISM® began tracking this data two years ago. The lack of production is placing additional downward pressure on profits, thereby increasing the urgency to reduce staffing levels. Fiore noted that respondents emphasized their companies' inability to retain workers without an increase in incoming work over the next three to six months. As previously indicated, given the current elevated interest rates and ongoing election uncertainty, manufacturing activity is likely to remain in a holding pattern for the remainder of the year.

Macro Economy

- Non-farm payroll employment rose by 142,000 jobs MoM in August on a seasonally adjust basis following downward revisions to both June and July figures, according to the most recent jobs report released by the Bureau of Labor Statistics (BLS).

- The unemployment rate fell by 0.1% MoM to 4.2% in August after consecutive increases over the last five months.

- Transportation and Warehousing added 7,900 jobs MoM in August on a seasonally adjusted basis, driven primarily by increases in pipeline transportation as well as warehousing and storage.

- Total Truck Transportation shed 1,400 jobs on a seasonally adjusted basis.

Warehousing and Storage employment increased by 3,900 jobs on a seasonally adjusted basis in August.

- Both the headline and core Personal Consumption Expenditures (PCE) indices rose by 0.2% MoM in July on a seasonally adjusted basis, according to the most recent report released by the Bureau of Economic Analysis (BEA).

- On an annual basis, the all-items PCE index rose by 2.5% in July on a seasonally adjust basis and was unchanged from June.

- Excluding food and energy, the PCE index increased by 2.6% YoY in July on a seasonally adjusted basis and was flat from June.