Back to September 2024 Industry Update

September 2024 Industry Update: Fuel

The benchmark price of fuel continued its downward trend in August as excess supply remains unencumbered by weak demand and economic uncertainty.

Key Points

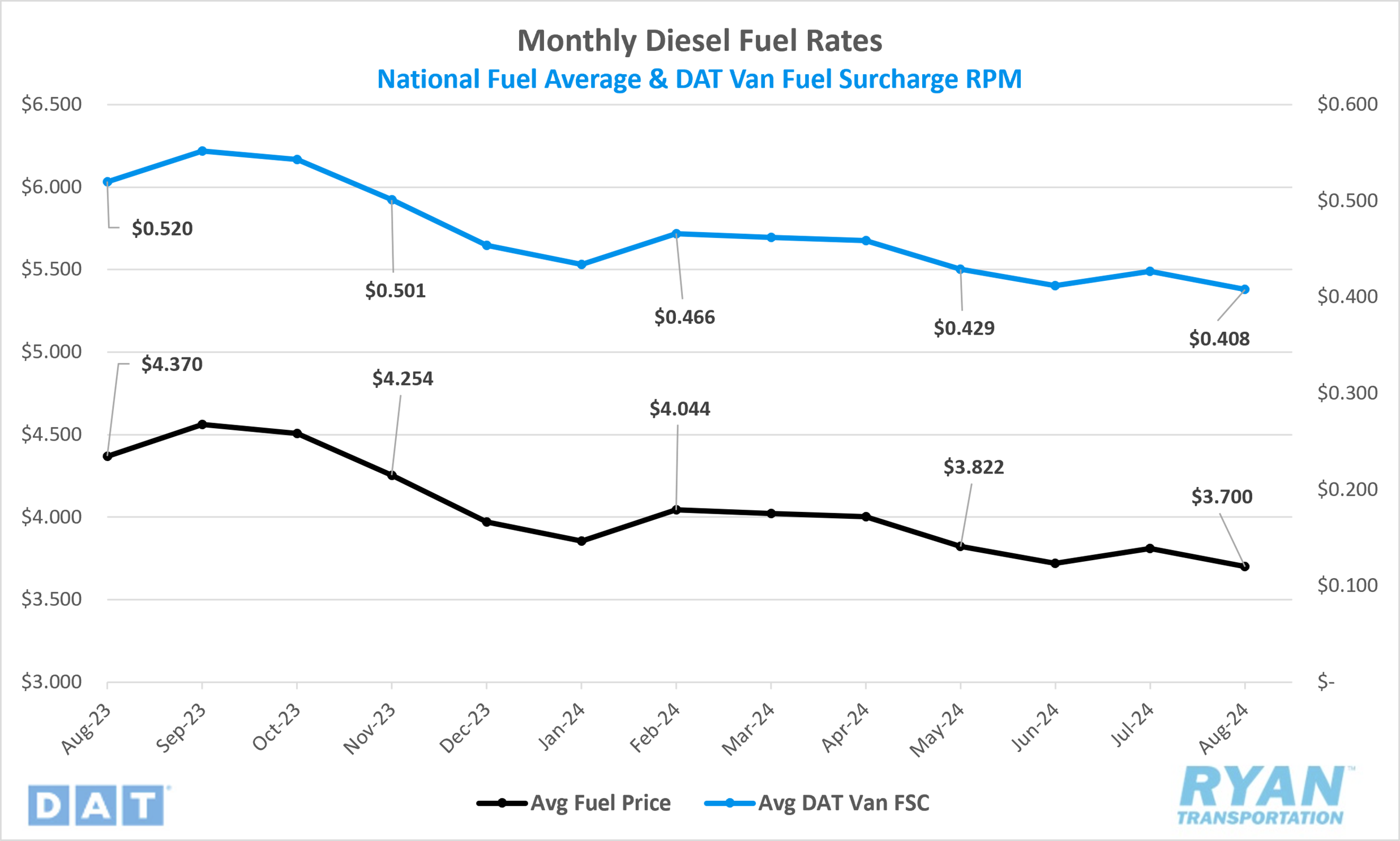

- The national average price of diesel declined in August, dropping 2.9% MoM, or $0.11, from $3.81 in July to $3.70.

- Compared to August 2023, diesel prices were 15.3%, or $0.67, lower in August 2024.

- Draws on U.S. Crude Reserves outpaced builds in August by 14.7M bbls and exceeded the consensus decline of 5.6M bbls for the weeks ending August 2 and August 30.

Summary

Following an increase in July that ended a four-month streak of declines, the average fuel price resumed its downward trend in August. The monthly average price of diesel in August fell to its lowest level since December 2021, a few months before Russia's invasion of Ukraine, which had caused a surge in prices. On a weekly basis, fuel prices steadily declined throughout August, dropping by a total of over $0.14 during the month. In the final week of August, the benchmark price of fuel reported by the Energy Information Administration (EIA) decreased by just over $0.03 per gallon WoW, reaching its lowest point since January 3, 2022.

Meanwhile, withdrawals from crude oil reserves continued to outpace additions for the fourth consecutive month in August. Crude output has risen despite weak global demand and declining prices, particularly in the United States and Guyana. According to the EIA, the U.S. refinery utilization rate remained elevated at approximately 92.2% in August. However, this figure is expected to decline to around 90% in Q4, according to recent earnings calls from major U.S. refiners, as the supply surplus has compressed margins in recent months.

Across the Atlantic, plans by OPEC+ to gradually increase production in October have been postponed until later in the year. However, according to a report from S&P Global Commodity Insights (SPGCI), member nations have been exceeding their agreed production targets, primarily driven by Iran. The report indicates that OPEC+ production rose significantly in July, increasing by 100,000 barrels per day (bpd) compared to June, and exceeding the implied targets by 240,000 bpd. Despite this additional output, the delay in the decision to raise production led the EIA to revise its forecast. New projections indicate that global demand will exceed production by 0.9 million bpd in 2024, up from a 0.5 million bpd deficit in the previous forecast.

Why It Matters

The continued decline in average diesel prices has provided welcome relief for carriers operating near breakeven, particularly those unable to pass fuel costs on to shippers. This downward trend in benchmark fuel prices is largely driven by weak global demand, especially in China, and an oversupply in the market. While retail diesel prices fell steadily throughout the month, futures markets experienced significant volatility in August. Despite the overall weak demand, potential supply disruptions stemming from escalating conflicts in the Middle East caused only temporary price increases.

Despite the current downward trend in oil markets and the absence of strong upward pressure factors, the EIA continues to project a rise in prices over the coming months. This forecast is based primarily on declining supply levels, as U.S. refiners reduce utilization rates and OPEC+ delay plans for gradual production increases. In its most recent Short-Term Energy Outlook (STEO), the EIA indicated that the price of Brent Crude, which closed out August at just over $76 per barrel, is expected to increase to $82 by December. The report also suggests that ongoing conflicts in the Middle East may lead to future supply disruptions, and some OPEC+ member nations may choose not to reverse production cuts voluntarily. However, whether global demand will ultimately outpace supply over the long term remains uncertain.