Back to September 2024 Industry Update

September 2024 Industry Update: Intermodal

Intermodal volumes continued to improve in August, approaching levels near their 2021 peak season despite rates remaining historically low.

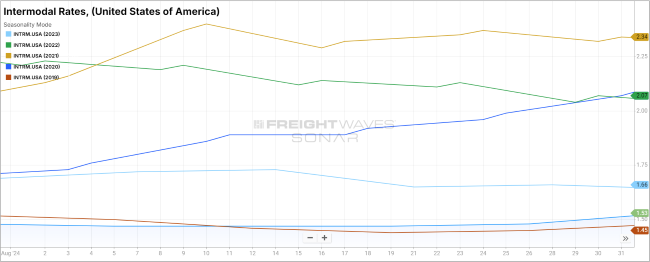

Spot Rates

Key Points

- The FreightWaves SONAR Intermodal Rates Index (INTRM.USA), which measures the average weekly all-in door-to-door intermodal spot rate for 53’ dry vans across a majority of origin-destination pairings, remained unchanged MoM in August at $1.48.

- Compared to August 2023, intermodal spot rates are down 10.8% YoY and are 22.9% below the 5-year average.

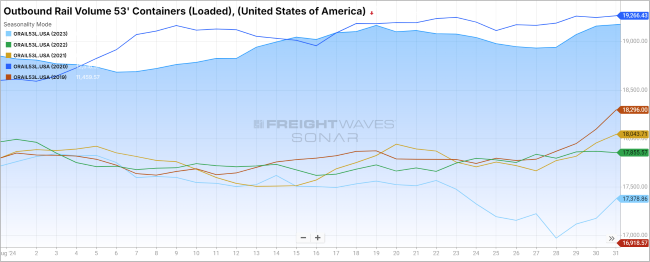

Volumes

Key Points

- Total loaded volumes for 53’ containers for all domestic markets, measured by the FreightWaves SONAR Loaded Outbound Rail Volume Index (ORAIL53L.USA), increased slightly in August to end the month up 1.7% compared to the end of July.

- On an annual basis, total loaded volumes for 53’ containers were 10.3% higher YoY compared to August 2023 and registered 5.5% above the 5-year average.

Intermodal Summary

Intermodal volumes continued to show improvement in August, nearing levels last seen during the peak season of 2021. According to the American Association of Railroads (AAR) monthly report, total intermodal volumes increased by 14.3% YoY in August 2023, driven by higher import activity and sustained consumer resilience. The report noted that intermodal volumes averaged 282,878 units per week, marking the highest weekly average since May 2021. Carload volumes also posted annual gains in August, though at a more modest rate, increasing by 0.6% YoY. This represents the first YoY gain for carload shipments recorded in 2024. The increase brought the average weekly carload volumes to 228,814 units in August, the highest level since October 2023. Overall, combined intermodal and carload volumes were up 7.8%, or 147,352 units, compared to the same period in 2023.

Despite the sustained strength in overall volumes, rail carriers continue to operate at historically low costs. Intermodal spot rates indicate that intermodal capacity remains ample. Although a relatively small proportion of intermodal volume moves on the spot market, rates can experience week-to-week volatility as carriers seek to safeguard capacity for contractual shippers. On the contractual side, intermodal rates turned positive YoY in August after bottoming out in early July. Compared to the same period in 2023, intermodal contract rates rose by $0.04 YoY, following a $0.21 MoM increase from their bottom in July. While intermodal rates remain lower than in previous years, the cost savings relative to the weaker truckload market are still minimal. The FreightWaves SONAR Intermodal Contract Savings Index (IMCSI1.USA), which measures the percentage difference between initial dry van contract rates excluding fuel and initial intermodal contract rates excluding fuel, remained essentially flat in August at around 7.8%, the same level recorded at the end of July.