Back to September 2024 Industry Update

September 2024 Industry Update: Truckload Capacity Outlook

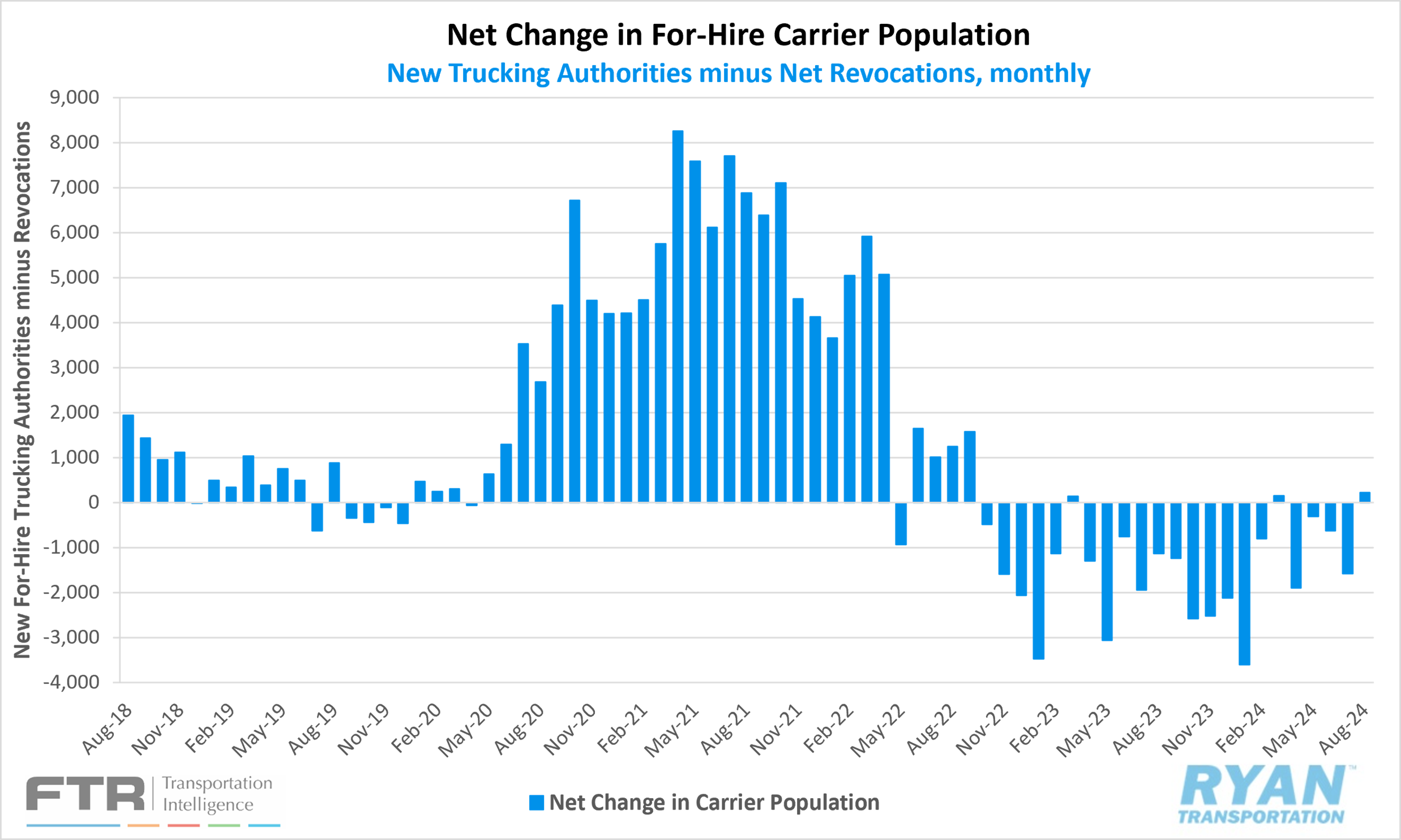

The net change in the carrier population turned positive in August, driven by an increase in new entrants, while revocations fell significantly.

Key Points

- Total net revocations, a measure of total authority rejections minus reinstatements, fell in August by 1,346 carriers, decreasing from 6,182 revocations in July to 4,836 in August, according to FTR’s preliminary analysis of the Federal Motor Carrier Safety Administration’s (FMCSA) data.

- While rejections declined substantially, the number of newly authorized for-hire trucking companies increased by 443 carriers, rising from 4,612 new authorities in July to 5,055 in August, per FTR’s reporting.

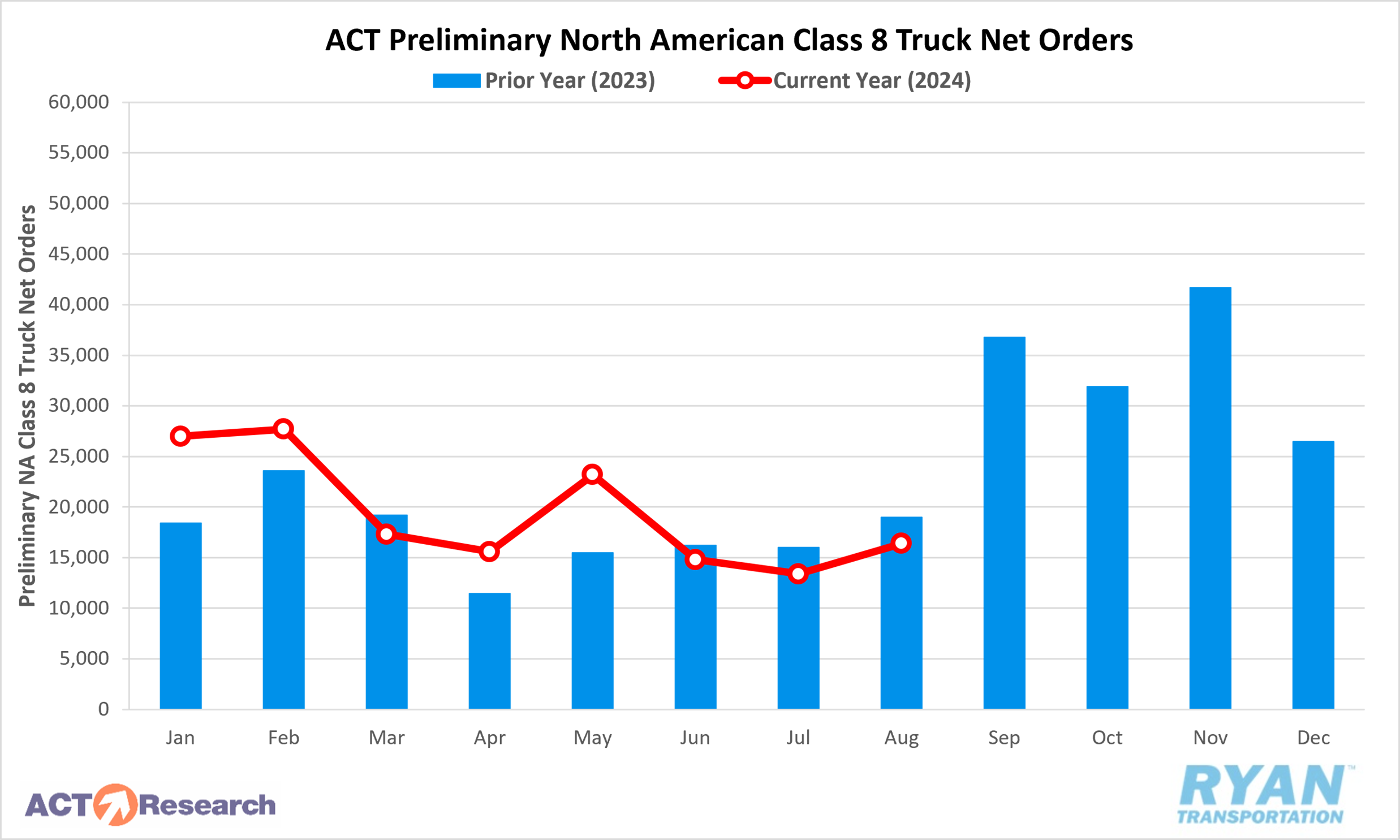

- Preliminary North American Class 8 Orders in August ranged from 13,400 units as reported by FTR to 16,400 units per ACT Research, with both estimates registering 16% lower on an annual basis.

Summary

Following accelerated declines in July, which nearly doubled the figures recorded in June, the net change in the for-hire carrier population turned positive in August with an increase of 219 carriers. This growth was driven by a substantial reduction in net revocations and an increase in new authorizations. August marks only the third instance since September 2022 of a MoM increase in the carrier population and represents the largest increase among these occurrences. New authorities remain historically high, with 5,055 new entrants recorded in August—the third-highest figure since September of last year. In 2024 to date, new authorizations have averaged slightly over 4,700 per month. For context, the FMCSA authorized fewer than 3,700 carriers in 2018, the strongest year before 2020. However, new carrier authorities are still at approximately half of the 2021 peak, when the monthly average was 9,150 new carriers.

Simultaneously, net revocations have been declining over the past few months but remain near historic highs. In August, total net revocations less reinstatements decreased from 6,182 in July to 4,835, the lowest level since April 2022. According to FTR's analysis, since that time, net revocations have averaged nearly 6,900 per month. It is worth noting that, prior to May 2022, carrier failures had never surpassed 5,000 in a single month.

Preliminary estimates indicate that North American Class 8 orders were slightly higher MoM in August compared to July, although they remain below YoY levels. August was the third consecutive month in which orders fell below the levels recorded in the same period the previous year. According to ACT Research, Class 8 orders were within seasonally expected levels, as August typically represents the last month of lower orders before OEMs open the books for the next year's orders. Given the historically weak average for orders during this month, a significant seasonal adjustment raised Class 8 orders nearly 12% above nominal levels. FTR reports that the annualized figure for Class 8 orders reached 271,000 units in August, suggesting that orders are running slightly below replacement levels. Nonetheless, stronger order figures earlier in the year have resulted in a 14% YoY increase in net orders, despite the three consecutive months of decline.

Why It Matters

The increase in the carrier population in August, despite the absence of significant improvement in overall market conditions, has created uncertainty in the capacity outlook. While net revocations have been trending lower throughout the year, aligning with the theory that weaker carriers were forced out early, the rise in new entrants is less straightforward to explain. One theory suggests that smaller carriers and owner-operators are returning to the market after initially exiting during the early phase of the downturn. The August Logistics Managers’ Index (LMI) report indicates that “signs of renewed activity in the freight market, along with expectations of the traditional surge in demand following the Labor Day holiday, are likely prompting some of the previously sidelined capacity over the past two years to re-enter the market, contributing to the slight increase in available capacity.”

While the decline in the for-hire carrier population may have temporarily stabilized, the ongoing expansion of private fleets presents an additional challenge to the capacity outlook. As previously discussed, companies increasingly relying on their own fleets have removed a considerable share of volume from the for-hire market. According to a NPTC report, which cited FMCSA data, there are over 940,000 private fleets registered with the FMCSA, compared to approximately 1.08 million for-hire carriers, indicating that private fleets comprise 47% of total truckload carriers. Furthermore, 72% of respondents in the survey indicated plans to increase private fleet drivers, equipment and shipments over the next five years.

After a period of significant overbuying over the past two years, Class 8 truck orders are beginning to normalize. Pre-buying is slowing as uncertainties around the upcoming election and rising interest rates are delaying decision-making, which is evident in the thinning OEM backlogs. According to FTR’s analysis, the conventional truck market outperformed the vocational sector as fleets continue to invest in new equipment, albeit at a reduced pace. The NPTC survey found that 62% of private fleets are planning or expecting to add new equipment to their operations in 2024. While most of these additions are intended to replace older units, an average of 14% of the respondents indicated the new equipment would be dedicated to expansion.

Back to September 2024 Industry Update